Gaming Chair Market Size

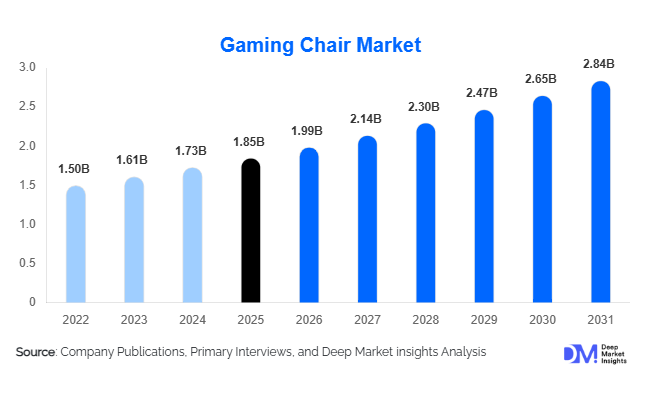

According to Deep Market Insights, the global gaming chair market size was valued at USD 1.85 billion in 2025 and is projected to grow from USD 1.99 billion in 2026 to reach USD 2.84 billion by 2031, expanding at a CAGR of 7.4% during the forecast period (2026–2031). The gaming chair market growth is primarily driven by the rapid expansion of esports ecosystems, increasing adoption of ergonomic seating solutions, rising consumer spending on gaming peripherals, and the growing convergence between gaming furniture and hybrid work environments.

Gaming chairs have evolved beyond niche gaming accessories into multifunctional ergonomic furniture products used across gaming, streaming, remote work, and content creation applications. The increasing awareness regarding posture correction, spinal health, and prolonged sitting comfort is significantly expanding the customer base globally. Consumers are increasingly investing in ergonomic seating products equipped with lumbar support, adjustable armrests, memory foam cushioning, and reclining mechanisms.

The rapid growth of professional esports tournaments, gaming cafés, streaming studios, and creator economies is further accelerating commercial demand for premium gaming chairs. Manufacturers are increasingly integrating advanced technologies such as RGB lighting, Bluetooth speakers, haptic feedback systems, cooling functions, and AI-powered posture monitoring into high-end product offerings. North America currently dominates the global gaming chair market due to strong premium product penetration and established gaming infrastructure. Meanwhile, the Asia-Pacific region is emerging as the fastest-growing region supported by expanding gaming populations, rising disposable incomes, and increasing esports investments across China, India, Japan, and Southeast Asia.

Key Market Insights

- Gaming chairs are increasingly positioned as ergonomic lifestyle furniture products, expanding demand beyond traditional gamers into hybrid workers and content creators.

- Esports and streaming ecosystems are significantly boosting commercial demand, particularly across gaming arenas, creator studios, and university esports programs.

- North America dominates the global gaming chair market, supported by premium gaming peripheral adoption and high consumer spending on ergonomic furniture.

- Asia-Pacific remains the fastest-growing regional market, driven by rapid gaming population growth and esports infrastructure investments.

- Mid-range gaming chairs priced between USD 100–250 account for the largest market share, balancing affordability with ergonomic functionality.

- Smart gaming chair technologies, including posture monitoring, RGB integration, haptic feedback, and cooling systems, are reshaping premium product innovation.

Gaming Chair Market Trends

Convergence Between Gaming and Ergonomic Office Furniture

The gaming chair market is increasingly witnessing convergence with ergonomic office furniture categories. Rising hybrid work culture and prolonged screen-time habits are encouraging consumers to invest in seating products capable of supporting both productivity and entertainment requirements. Manufacturers are launching hybrid gaming-office chairs featuring professional aesthetics, breathable materials, adjustable lumbar systems, and ergonomic support structures suitable for long working hours. This trend is expanding the total addressable market significantly beyond gamers alone. Consumers are prioritizing posture correction, spinal support, and sitting comfort, particularly among remote workers, freelancers, and digital creators. As a result, gaming chair brands are increasingly competing directly with premium office furniture manufacturers.

Technology-Integrated Smart Gaming Chairs

Technological innovation is becoming a major differentiating factor within the gaming chair market. Manufacturers are integrating advanced features such as RGB lighting systems, Bluetooth speakers, massage functions, cooling technologies, haptic feedback systems, and AI-powered posture monitoring. Premium gaming chairs are increasingly designed to enhance immersive gaming experiences while also improving user wellness and sitting ergonomics. Smart gaming chairs synchronized with virtual reality environments and gaming systems are emerging within premium segments. Mobile application integration for posture tracking and sitting analytics is also gaining traction among health-conscious consumers. These innovations are particularly appealing to younger demographics seeking immersive and technologically advanced gaming setups.

Gaming Chair Market Drivers

Expansion of Global Esports and Gaming Ecosystems

The rapid expansion of esports tournaments, online multiplayer gaming, and streaming platforms is significantly driving demand for gaming chairs globally. Professional gamers, esports teams, streamers, and gaming cafés increasingly require ergonomic seating solutions capable of supporting prolonged gaming sessions. The commercialization of esports and rising sponsorship investments are accelerating infrastructure spending on premium gaming accessories, including gaming chairs. Competitive gaming environments often involve extended sitting durations, making ergonomic seating essential for performance optimization and user comfort. Growing gaming participation among younger demographics globally continues to support long-term market demand.

Growing Awareness Regarding Ergonomic Wellness

Consumers are increasingly becoming aware of the health risks associated with prolonged sitting, including spinal strain, neck pain, and posture-related disorders. Gaming chairs are increasingly marketed as ergonomic wellness products designed to improve sitting posture and reduce physical fatigue. Features such as adjustable lumbar support, neck cushions, reclining mechanisms, memory foam padding, and multi-directional armrests are becoming standard expectations among consumers. This wellness-oriented positioning is expanding gaming chair adoption among non-gaming users, including remote workers and office professionals seeking enhanced seating comfort.

Gaming Chair Market Restraints

High Cost of Premium Gaming Chairs

Premium gaming chairs equipped with advanced ergonomic systems and smart technologies often carry high retail prices, limiting adoption among price-sensitive consumers. Advanced models featuring premium materials, posture-monitoring technologies, and immersive gaming integrations can exceed several hundred dollars, restricting accessibility in emerging markets. Consumers in developing economies frequently prioritize affordability over advanced ergonomic functionality, creating pricing pressure across mid-range product categories.

Raw Material Price Volatility and Supply Chain Challenges

The gaming chair industry remains highly dependent on steel frames, synthetic leather, plastics, foam materials, and electronic components. Fluctuations in raw material prices, transportation costs, and geopolitical disruptions can significantly impact manufacturing margins. Global supply chain instability has also increased production lead times and logistics expenses in recent years. Manufacturers are increasingly challenged to balance product quality, innovation, and affordability while maintaining profitability in a highly competitive environment.

Gaming Chair Market Opportunities

Hybrid Work and Gaming Furniture Expansion

The rapid expansion of hybrid work culture presents substantial growth opportunities for gaming chair manufacturers. Consumers are increasingly seeking ergonomic seating solutions capable of supporting both work and gaming activities. Hybrid gaming-office chairs with minimalist aesthetics, improved lumbar systems, breathable fabrics, and productivity-focused ergonomics are gaining strong traction globally. This convergence between gaming furniture and office seating is expected to significantly expand the addressable consumer base over the forecast period.

Commercial Esports Infrastructure Development

The growth of esports arenas, gaming cafés, creator studios, and university esports programs is generating substantial commercial demand for gaming chairs. Professional gaming environments require durable, ergonomic, and visually appealing seating products that support long-duration use. Countries such as China, the United States, South Korea, Saudi Arabia, and India are witnessing increasing investments in esports infrastructure, creating long-term opportunities for gaming chair manufacturers targeting institutional and commercial customers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.85 Billion |

| Market Size in 2026 | USD 1.99 Billion |

| Market Size in 2031 | USD 2.84 Billion |

| CAGR | 7.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

PC gaming chairs dominate the global gaming chair market, accounting for the largest share of industry revenue due to strong demand from esports players, streamers, and desktop gamers. Racing-style ergonomic chairs remain especially popular because of their aggressive aesthetics, reclining capabilities, adjustable support systems, and immersive gaming appeal. Hybrid gaming-office chairs are emerging as one of the fastest-growing product categories as consumers increasingly utilize gaming chairs for remote work applications. Console gaming chairs, including rocker chairs and pedestal seating models, continue to witness stable demand among console gamers and entertainment-focused consumers. Simulator and cockpit gaming chairs are also gaining traction within premium segments due to increasing popularity of racing simulators and virtual reality gaming setups.

Material Type Insights

PU leather gaming chairs account for the largest market share globally due to their affordability, premium appearance, durability, and ease of maintenance. Manufacturers widely prefer PU leather because it balances aesthetics with cost efficiency across mid-range and premium product categories. Mesh fabric gaming chairs are witnessing increasing adoption in tropical and warm-weather regions due to improved airflow and sitting comfort during prolonged usage. Genuine leather gaming chairs remain concentrated within luxury segments catering to premium consumers seeking high-end ergonomic furniture. Hybrid material chairs combining mesh, foam, and synthetic leather are also gaining popularity due to improved breathability and ergonomic performance.

Distribution Channel Insights

Online retail channels dominate gaming chair sales globally, supported by the rapid growth of e-commerce marketplaces and direct-to-consumer sales models. Consumers increasingly prefer online platforms because they provide broader product variety, customer reviews, influencer recommendations, and competitive pricing structures. Gaming chair manufacturers are investing heavily in direct brand websites to improve profitability and customer engagement. Offline retail channels, including gaming accessory stores, furniture chains, and electronics retailers, continue to maintain relevance among consumers seeking product trials before purchase. Influencer marketing, gaming livestream promotions, and esports sponsorships are also playing increasingly important roles in online customer acquisition strategies.

End-Use Insights

Residential users account for the largest share of the gaming chair market due to strong household demand among casual gamers, professional gamers, content creators, and hybrid workers. The rise of remote work culture has significantly expanded residential adoption beyond traditional gaming applications. Commercial demand from esports arenas, gaming cafés, streaming studios, and university esports labs is growing rapidly, particularly across Asia-Pacific and North America. Content creators and professional streamers are increasingly investing in premium gaming chairs as part of professional studio setups. Simulation-based applications, including racing simulators and VR gaming environments, are also emerging as important end-use categories supporting premium product demand.

Price Range Insights

Mid-range gaming chairs priced between USD 100 and USD 250 account for the largest share of global market revenue due to their balance between affordability and ergonomic functionality. Consumers increasingly seek products that provide adjustable lumbar support, reclining features, and premium aesthetics without entering luxury price categories. Budget gaming chairs remain highly popular in emerging economies due to strong price sensitivity among younger consumers. Premium and luxury gaming chairs are witnessing rising adoption in developed markets, particularly among professional gamers, streamers, and affluent consumers prioritizing advanced ergonomic systems and smart feature integration.

Explore more data points, trends and opportunities Download Free Sample Report

Gaming Chair Market Segmentations

By Product Type

- PC Gaming Chairs

- Console Gaming Chairs

- Hybrid Gaming & Office Chairs

- Professional Esports Chairs

- Simulator & Cockpit Gaming Chairs

- Floor Rocker Gaming Chairs

By Material Type

- PU Leather

- Mesh Fabric

- Genuine Leather

- Memory Foam Upholstery

- Hybrid Material Chairs

By Application

- Gaming

- Streaming & Content Creation

- Work-from-Home & Hybrid Office

- Virtual Reality Gaming

- Simulation Training

By End User

- Residential Users

- Professional Gamers

- Content Creators & Streamers

- Gaming Cafés

- Esports Arenas

- Educational Esports Labs

By Distribution Channel

- Online Retail

- Direct-to-Consumer Websites

- Specialty Gaming Stores

- Furniture Retail Chains

- Consumer Electronics Stores

Regional Insights

North America

North America remains the largest gaming chair market globally, accounting for nearly 35% of global market revenue in 2025. The United States dominates regional demand due to strong consumer spending on gaming peripherals, large esports audiences, and widespread remote work adoption. Premium gaming chair penetration is particularly high among professional gamers, streamers, and hybrid workers. Canada also represents a growing market supported by rising gaming participation and increasing awareness regarding ergonomic seating products. Strong influencer marketing ecosystems and esports sponsorship activity further support regional market expansion.

Europe

Europe accounts for a significant share of the gaming chair market, led by Germany, the United Kingdom, and France. European consumers increasingly prioritize ergonomic wellness, sustainability, and product durability when purchasing gaming furniture. The region is witnessing growing demand for premium gaming-office hybrid chairs as remote work adoption remains high. Sustainability-focused product innovations, including recyclable materials and eco-friendly upholstery alternatives, are becoming important competitive differentiators across European markets.

Asia-Pacific

Asia-Pacific represents the fastest-growing gaming chair market globally due to its massive gaming population and rapidly expanding esports ecosystem. China remains the largest regional market and manufacturing hub because of its strong electronics supply chain infrastructure and large gamer base. Japan and South Korea continue to witness strong demand for premium ergonomic gaming furniture supported by advanced gaming cultures. India is emerging as one of the fastest-growing national markets due to rapid mobile gaming growth, increasing disposable incomes, and expanding esports investments. Southeast Asian countries such as Indonesia, Thailand, Vietnam, and the Philippines are also experiencing strong market expansion.

Latin America

Latin America is witnessing steady growth in gaming chair demand, particularly across Brazil and Mexico. Brazil remains the largest regional market supported by strong esports engagement and expanding online gaming participation. Mid-range gaming chairs dominate demand across the region due to consumer price sensitivity. The increasing popularity of gaming influencers and livestreaming platforms is also positively impacting regional product adoption.

Middle East & Africa

The Middle East & Africa gaming chair market is gradually expanding due to rising gaming investments and growing esports activities. GCC countries such as Saudi Arabia and the UAE are increasingly investing in gaming infrastructure, esports tournaments, and entertainment ecosystems. South Africa represents the leading African market for gaming peripherals and gaming furniture. Rising youth populations and increasing internet penetration are expected to support long-term market growth across the region.

Key Players in the Gaming Chair Market

- Secretlab

- Herman Miller

- DXRacer

- Corsair

- Razer

- AKRacing

- AndaSeat

- RESPAWN

- Vertagear

- AutoFull

- Cougar

- X Rocker

- ThunderX3

- Arozzi

- Noblechairs