Fur Products Market Size

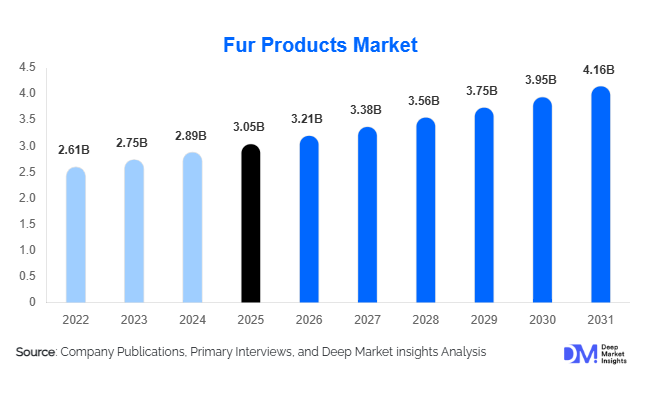

According to Deep Market Insights, the global fur products market size was valued at USD 3.05 billion in 2025 and is projected to grow from USD 3.21 billion in 2026 to reach USD 4.16 billion by 2031, expanding at a CAGR of 5.3% during the forecast period (2026–2031). The fur products market growth is primarily driven by increasing luxury fashion consumption, rising demand for premium winter apparel, growing adoption of fur-based home décor products, and expanding spending among affluent consumers across Asia-Pacific and the Middle East. Despite increasing regulatory scrutiny and ethical concerns surrounding animal-derived materials, the market continues to benefit from strong demand for heritage luxury products, limited-edition collections, and high-end craftsmanship. The integration of traceability systems, sustainable sourcing certifications, and direct-to-consumer luxury retail platforms is further supporting market expansion.

Key Market Insights

- Fur garments remain the largest product category, accounting for approximately 58% of global market revenue in 2025 due to sustained demand for luxury coats, jackets, and winter fashion products.

- Mink fur dominates raw material consumption, representing nearly 44% of total market value owing to its superior durability, texture, and luxury positioning.

- Europe remains the largest regional market, accounting for approximately 36% of global revenue, supported by strong luxury fashion manufacturing and established consumer demand.

- Asia-Pacific is the fastest-growing region, driven by increasing luxury spending in China, South Korea, Japan, and emerging Southeast Asian markets.

- Luxury retail channels continue to dominate sales, with brand-owned stores accounting for nearly 35% of global distribution.

- Sustainability and traceability initiatives are becoming key competitive differentiators as consumers increasingly seek ethically sourced luxury products.

What are the latest trends in the fur products market?

Growth of Sustainable and Certified Fur Products

The fur products industry is witnessing a significant shift toward sustainability and responsible sourcing. Consumers, particularly younger luxury buyers, increasingly demand transparency regarding animal welfare standards, sourcing practices, and environmental impacts. Manufacturers are investing in certification programs, blockchain-enabled traceability platforms, and sustainable processing technologies to demonstrate compliance with evolving consumer expectations. Certified fur products are commanding premium prices in luxury markets, while brands with transparent sourcing policies are strengthening customer loyalty. The adoption of environmental, social, and governance (ESG) frameworks is also becoming increasingly important among luxury retailers and investors.

Expansion of Fur Home Décor Applications

Luxury home décor is emerging as one of the fastest-growing applications for fur products. High-end residential developments, luxury hotels, and premium interior design projects are incorporating fur throws, rugs, cushions, and decorative accessories to enhance aesthetics and exclusivity. Affluent homeowners increasingly view natural fur furnishings as statement products that reflect luxury lifestyles. Growth in premium real estate and luxury hospitality industries is creating additional demand beyond traditional apparel applications. This diversification is helping manufacturers reduce dependence on fashion cycles while accessing new revenue streams in premium interiors.

What are the key drivers in the fur products market?

Growing Global Luxury Goods Consumption

The expansion of the global luxury goods industry remains a primary growth driver for fur products. Increasing disposable incomes among high-net-worth individuals and affluent middle-class consumers are supporting demand for premium fashion products. Luxury consumers continue to view fur garments and accessories as symbols of exclusivity, craftsmanship, and social status. Emerging luxury markets across Asia-Pacific and the Middle East are contributing significantly to overall industry growth, while established luxury markets in Europe and North America continue to generate substantial revenue.

Rising Demand for Premium Winter Fashion

Fur products continue to benefit from demand for high-performance winter apparel. Fur garments offer superior insulation and durability compared to many alternative materials, making them highly desirable in colder climates. Countries including the United States, Canada, China, Russia, Finland, and South Korea continue to generate strong demand for luxury outerwear. Premium winter fashion collections from leading luxury brands increasingly incorporate fur elements, supporting steady market growth despite broader industry challenges.

Digital Transformation of Luxury Retail

Luxury e-commerce platforms, virtual showrooms, AI-powered personalization tools, and direct-to-consumer retail strategies are transforming the fur products market. Digital platforms enable brands to reach affluent consumers globally while enhancing customer engagement through customization and virtual product visualization. Online luxury sales continue to increase, particularly among younger consumers who prioritize convenience, personalization, and omnichannel shopping experiences.

What are the restraints for the global market?

Regulatory Restrictions and Ethical Concerns

Animal welfare concerns continue to create challenges for market participants. Several countries and regions have implemented restrictions on fur farming, while consumer advocacy groups increasingly campaign against natural fur products. Regulatory uncertainty can affect investment decisions, disrupt supply chains, and limit expansion opportunities in certain markets. Luxury brands must continuously adapt sourcing practices and communication strategies to address evolving regulatory requirements and consumer expectations.

Competition from Faux Fur and Alternative Materials

Technological advancements in synthetic textiles have significantly improved the quality and appearance of faux fur products. Many consumers seeking luxury aesthetics at lower prices are increasingly opting for high-quality alternatives. Growing environmental and ethical awareness further supports demand for synthetic materials, creating competitive pressure on traditional fur manufacturers. This trend is particularly evident among younger consumers in North America and Europe.

What are the key opportunities in the fur products industry?

Expansion of Luxury Consumption Across Asia-Pacific

Asia-Pacific represents the most attractive growth opportunity for fur product manufacturers. China remains one of the largest luxury consumer markets globally, while South Korea, Japan, Singapore, Thailand, and Vietnam continue to experience growth in premium spending. Increasing urbanization, rising disposable incomes, and strong demand for status-oriented fashion products are creating substantial opportunities for premium fur brands. Retail expansion and luxury shopping tourism are further accelerating regional growth.

Premium Home Décor and Hospitality Applications

The increasing popularity of luxury home décor products presents significant opportunities for market participants. Fur throws, cushions, rugs, and decorative accessories are becoming increasingly common in luxury residences, boutique hotels, and premium hospitality projects. This trend is expected to create a complementary revenue stream alongside traditional apparel applications, reducing exposure to seasonal fluctuations in fashion demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.05 Billion |

| Market Size in 2026 | USD 3.21 Billion |

| Market Size in 2031 | USD 4.16 Billion |

| CAGR | 5.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fur garments accounted for approximately 58% of the global fur products market revenue in 2025, making them the dominant product segment. The segment's leadership is primarily driven by the high average selling price (ASP) of luxury fur coats, jackets, capes, and premium outerwear products compared to accessories, footwear, and home furnishing applications. Fur coats continue to represent the largest revenue contributor within the category due to their strong association with luxury fashion, superior insulation properties, and long product life cycle. Demand remains particularly strong across North America, Europe, China, South Korea, and other cold-climate regions where premium winter apparel serves both functional and status-oriented purposes. The growing number of high-net-worth individuals (HNWIs), increasing luxury fashion expenditures, and the expansion of premium retail networks continue to support segment growth. Fur-trimmed jackets and outerwear have witnessed rising adoption among younger luxury consumers seeking contemporary fashion aesthetics. In addition, luxury fashion houses continue to incorporate fur into seasonal collections, reinforcing demand through brand positioning and exclusivity.

Home furnishing fur products represent the fastest-growing product category, driven by rising investments in luxury residential construction, premium interior design projects, boutique hospitality developments, and high-end vacation properties. Fur throws, rugs, cushions, and decorative accessories are increasingly viewed as premium lifestyle products rather than seasonal purchases, creating new long-term growth opportunities for market participants.

Fur Source Insights

Mink fur remained the largest fur source segment, accounting for approximately 44% of global market value in 2025. Its market leadership is primarily attributed to its superior softness, lightweight characteristics, durability, and premium appearance, making it the preferred material for luxury apparel manufacturers worldwide. Mink fur also offers greater versatility in processing, coloring, and garment construction compared to many alternative fur types, enabling wider application across coats, jackets, accessories, and luxury fashion products. The dominance of mink fur is further supported by its established supply chain infrastructure and strong acceptance among luxury consumers in China, Europe, North America, and South Korea. Premium brands continue to utilize mink fur in flagship collections due to its ability to command higher margins and reinforce luxury brand positioning.

Fox fur remains the second-largest source segment, benefiting from strong demand in outerwear trim, collars, cuffs, and luxury accessories. Rabbit fur continues gaining traction due to its affordability and broader accessibility across premium consumer segments. Meanwhile, chinchilla and sable furs occupy ultra-luxury niches characterized by limited production volumes and exceptionally high pricing, appealing primarily to affluent collectors and bespoke fashion buyers. Shearling and lamb fur products are increasingly benefiting from growing consumer preference for versatile luxury materials suitable for both apparel and home décor applications.

Distribution Channel Insights

Brand-owned retail stores accounted for approximately 35% of global fur product sales in 2025 and remain the leading distribution channel. The segment's dominance is driven by luxury brands' strategic focus on maintaining exclusivity, controlling pricing structures, strengthening customer relationships, and delivering personalized shopping experiences. Direct retail channels allow manufacturers to preserve brand image while maximizing profit margins by reducing dependence on intermediaries. The growth of flagship luxury stores in major fashion capitals such as Paris, Milan, New York, Shanghai, Seoul, and Dubai continues to reinforce channel dominance. Personalized consultations, custom tailoring services, limited-edition collections, and VIP customer programs further enhance the appeal of brand-owned retail formats among affluent consumers.

While traditional luxury department stores remain important sales channels, particularly in Europe and North America, the fastest growth is occurring within online direct-to-consumer (DTC) platforms. Luxury brands are increasingly investing in virtual showrooms, AI-powered personalization tools, digital customization features, and omnichannel retail strategies to improve customer engagement and capture younger luxury buyers. The expansion of luxury e-commerce ecosystems is expected to significantly increase the contribution of online channels over the forecast period.

End-Use Insights

Fashion and apparel applications accounted for approximately 67% of total global fur products demand in 2025, making it the largest end-use segment. The segment's leadership is primarily driven by the long-standing association between fur products and luxury fashion, as well as the continued popularity of premium outerwear among affluent consumers. Fur garments command significantly higher average transaction values compared to other applications, contributing disproportionately to total market revenue. The increasing global luxury apparel market, growing winter fashion spending, and rising demand for premium lifestyle products continue to support segment growth. Luxury fashion brands are increasingly introducing limited-edition collections, customized products, and seasonal fur apparel offerings to attract high-value consumers. Strong demand from China, the United States, Italy, France, South Korea, and Japan remains a major growth catalyst for this segment.

Luxury accessories represent the second-largest end-use category, benefiting from consumer preference for entry-level luxury products that provide premium brand ownership at lower price points than full garments. Meanwhile, home décor applications represent the fastest-growing end-use segment, supported by rising luxury residential construction, increasing demand for premium interior furnishings, and growing investments in luxury hospitality infrastructure globally. Collectibles and heritage products continue to serve a niche but highly profitable market characterized by bespoke craftsmanship and limited-production luxury goods.

Explore more data points, trends and opportunities Download Free Sample Report

Fur Products Market Segmentations

By Product Type

- Fur Garments

- Fur Accessories

- Fur Footwear

- Home Furnishing Fur Products

By Fur Source

- Mink Fur

- Fox Fur

- Rabbit Fur

- Chinchilla Fur

- Sable Fur

- Raccoon Dog Fur

- Shearling & Lamb Fur

- Other Natural Fur Types

By Distribution Channel

- Brand-Owned Retail Stores

- Luxury Department Stores

- Specialty Fur Boutiques

- Online Direct-to-Consumer Platforms

- Multi-Brand Luxury Retailers

By End Use

- Fashion & Apparel

- Luxury Accessories

- Home Décor & Furnishings

- Collectibles & Heritage Products

Regional Insights

North America

North America accounted for approximately 29% of global fur products market revenue in 2025. The United States remains the largest regional market, representing nearly 24% of global demand, while Canada contributes significantly through both consumption and production activities. Market growth in the region is primarily driven by high disposable incomes, a large concentration of affluent consumers, established luxury retail infrastructure, and sustained demand for premium winter apparel. The presence of globally recognized luxury brands, expanding direct-to-consumer sales channels, and growing consumer interest in certified and responsibly sourced luxury products continue supporting market expansion.

Canada remains an important market due to its long-standing fur industry heritage, cold climate conditions, and export-oriented fur production activities. Demand for luxury outerwear and premium accessories remains particularly strong across major metropolitan markets such as New York, Toronto, Vancouver, Chicago, and Boston.

Europe

Europe represented the largest regional market, accounting for approximately 36% of global revenue in 2025. The region's leadership is supported by its deep-rooted luxury fashion heritage, world-renowned design houses, established fur craftsmanship expertise, and strong consumer spending on premium apparel products. Italy, France, Germany, Greece, Denmark, and Finland serve as major production, processing, and consumption hubs.

Italy continues to lead regional demand due to its position as a global luxury fashion manufacturing center, while France benefits from the presence of several leading luxury brands and high-end retail networks. Greece remains one of the most important fur processing and export centers globally. Growth across Europe is additionally supported by tourism-driven luxury spending, premium fashion exports, and increasing demand for bespoke luxury apparel. Although regulatory scrutiny surrounding fur products has intensified, strong brand heritage and affluent consumer demand continue to sustain market growth.

Asia-Pacific

Asia-Pacific accounted for approximately 25% of global market revenue in 2025 and is expected to record the fastest growth rate through 2031. Regional expansion is being driven by rapid wealth creation, growing luxury consumption, increasing urbanization, and the rising number of high-net-worth individuals across China, South Korea, Japan, and Southeast Asia.

China remains the largest market within the region, accounting for approximately 15% of global demand, supported by strong luxury spending and increasing premium fashion adoption. South Korea benefits from robust luxury retail penetration and fashion-conscious consumers, while Japan maintains stable demand for premium craftsmanship and heritage luxury products. Emerging markets including Thailand, Vietnam, Indonesia, and Singapore are becoming increasingly important due to growing affluent populations and expanding luxury retail infrastructure. Continued investment by international luxury brands and increasing digital luxury commerce penetration are expected to make Asia-Pacific the primary engine of global market growth over the forecast period.

Latin America

Latin America accounted for approximately 4% of global market revenue in 2025. Brazil and Mexico represent the largest markets within the region, driven by luxury retail expansion, growing upper-income consumer groups, and increasing exposure to international luxury fashion brands. Market growth is further supported by rising urbanization, premium shopping center development, and the gradual expansion of luxury e-commerce platforms.

Although regional demand remains relatively concentrated among affluent consumers in major metropolitan areas such as São Paulo, Rio de Janeiro, Mexico City, and Monterrey, increasing luxury consumption trends are expected to create long-term growth opportunities. Tourism-driven luxury purchases also contribute to regional market development.

Middle East & Africa

The Middle East & Africa region accounted for approximately 6% of global market revenue in 2025. The UAE and Saudi Arabia remain the primary growth engines due to high per-capita incomes, expanding luxury retail infrastructure, and strong demand for premium fashion products. The rapid development of luxury shopping destinations, international fashion events, and high-end tourism activities continues to stimulate demand for luxury apparel and accessories.

Dubai has established itself as one of the world's leading luxury retail hubs, attracting affluent consumers from across the Middle East, Asia, Europe, and Africa. Saudi Arabia's ongoing economic diversification initiatives and increasing luxury consumption are further supporting market growth. In Africa, South Africa contributes through premium retail activity and luxury tourism spending. The combination of rising wealth, expanding luxury retail presence, and growing international tourism is expected to support above-average growth across the region during the forecast period.

Key Players in the Fur Products Market

- Saga Furs

- Kopenhagen Fur

- Fendi

- Yves Salomon

- Dennis Basso

- Braschi

- Manakas Frankfurt

- The Fur Vault

- Rindi

- Pologeorgis

- Revillon

- Blackglama

- NAFA

- Guliana Teso

- Simonetta Ravizza