Fur Coat Market Size

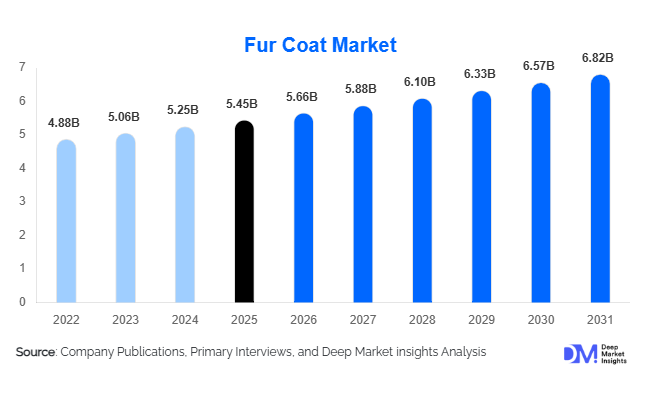

According to Deep Market Insights, the global fur coat market size was valued at USD 5.45 billion in 2025 and is projected to grow from USD 5.66 billion in 2026 to reach USD 6.82 billion by 2031, expanding at a CAGR of 3.8% during the forecast period (2026–2031). The fur coat market growth is primarily supported by rising luxury fashion consumption, increasing demand from affluent consumers in Asia-Pacific and the Middle East, growing interest in premium winter apparel, and the continued relevance of heritage luxury brands in the global outerwear industry. While regulatory restrictions and ethical concerns surrounding natural fur continue to affect market sentiment in several Western countries, demand remains resilient in premium fashion markets where exclusivity, craftsmanship, thermal performance, and status symbolism continue to influence purchasing decisions. Furthermore, the emergence of authenticated vintage fur marketplaces, luxury resale platforms, and traceable sourcing initiatives is creating new opportunities for manufacturers and retailers seeking to modernize the category and attract sustainability-conscious luxury consumers.

Key Market Insights

- Mink fur coats account for the largest product category, representing nearly 38% of global market revenue due to their superior durability, softness, and premium consumer appeal.

- Women’s fur coats dominate global demand, contributing approximately 68% of market revenue owing to wider fashion adoption and larger product portfolios.

- Europe remains the largest regional market, accounting for approximately 33% of global demand, supported by luxury manufacturing hubs in Italy and Greece.

- Asia-Pacific is the fastest-growing region, driven by increasing luxury consumption in China, South Korea, and Japan.

- Luxury fashion applications represent over 58% of total demand, highlighting the market’s strong association with prestige apparel and premium lifestyle positioning.

- Growth of resale and vintage luxury channels is expanding product lifecycle value and creating new revenue opportunities for luxury outerwear brands.

Fur Coat Market Trends

Growing Popularity of Vintage and Circular Luxury Fashion

The fur coat market is witnessing increasing participation in the luxury resale economy. Consumers are increasingly viewing fur coats as long-term investment pieces due to their durability, craftsmanship, and ability to retain value over decades. Luxury resale platforms and authenticated vintage marketplaces have significantly expanded consumer access to premium fur garments while simultaneously addressing sustainability concerns associated with new production. Many luxury consumers now prefer restored vintage fur products because they offer exclusivity, heritage value, and lower environmental impact compared to newly manufactured luxury apparel. As circular fashion continues gaining traction globally, manufacturers are increasingly investing in refurbishment, repair, and authenticated resale programs to capitalize on this emerging demand.

Expansion of Traceable and Certified Fur Supply Chains

Transparency has become a critical trend across the luxury apparel sector. Fur coat manufacturers are increasingly implementing traceability systems, animal welfare certifications, blockchain-based product tracking, and sustainability reporting frameworks to address growing consumer scrutiny. Premium brands are emphasizing responsible sourcing, ethical production practices, and compliance with international welfare standards. These initiatives are particularly important in Europe and North America, where luxury consumers increasingly evaluate sustainability credentials before making purchasing decisions. Advanced product authentication technologies are also being deployed to combat counterfeiting and improve consumer confidence in high-value fur garments.

Fur Coat Market Drivers

Growing Global Luxury Goods Expenditure

The continued expansion of luxury goods spending remains one of the strongest growth drivers for the fur coat market. Rising disposable incomes among affluent consumers, particularly in China, South Korea, the UAE, and North America, have increased demand for premium outerwear products. Fur coats continue to serve as status symbols within luxury fashion circles, benefiting from strong brand heritage, exclusivity, and superior craftsmanship. Luxury consumers increasingly prioritize personalized products, limited-edition collections, and high-end apparel experiences, all of which favor premium fur coat manufacturers. The growing population of high-net-worth individuals globally is expected to provide sustained support for market expansion throughout the forecast period.

Strong Demand from Cold-Climate Regions

Demand for fur coats remains particularly strong in regions experiencing prolonged and severe winter conditions. Countries including Russia, Canada, Northern China, Finland, Norway, and Kazakhstan continue to generate significant demand for natural fur outerwear due to its superior thermal insulation properties. In these markets, fur coats serve both functional and fashion-oriented purposes. The combination of extreme weather conditions and luxury consumption patterns has helped maintain stable market demand despite increasing availability of synthetic alternatives. Seasonal demand peaks during winter months continue to contribute significantly to annual revenue generation across key markets.

Fur Coat Market Restraints

Increasing Regulatory Restrictions on Fur Production

The fur coat market faces increasing regulatory pressure from governments introducing restrictions on fur farming, processing, and retail sales. Several European countries have implemented fur farming bans or enhanced animal welfare requirements, increasing operational costs and reducing production capacity. Regulatory inconsistencies across global markets create supply chain complexity and may discourage investment in new manufacturing facilities. Compliance costs associated with certification, traceability, and animal welfare monitoring continue to rise, creating barriers for smaller producers and independent manufacturers.

Growing Consumer Preference for Faux Fur Alternatives

The increasing popularity of faux fur products represents a significant challenge for traditional fur coat manufacturers. Younger consumers, particularly in Western Europe and North America, are demonstrating greater preference for synthetic alternatives that align with ethical and sustainability values. Major fashion houses have expanded faux fur collections to address evolving consumer expectations. Social media campaigns, animal welfare advocacy, and changing fashion trends continue to influence purchasing decisions, particularly among Generation Z and Millennial consumers. These developments may limit long-term demand growth in mature markets unless manufacturers successfully address transparency and sustainability concerns.

Fur Coat Market Opportunities

Expansion of Luxury Demand Across Asia-Pacific

Asia-Pacific presents the most attractive growth opportunity for fur coat manufacturers. China continues to represent the largest luxury consumption market globally, while South Korea and Japan maintain strong demand for premium fashion products. Growing wealth creation, urbanization, and increasing luxury brand penetration are supporting demand for high-end outerwear. International luxury brands are expanding retail footprints, digital commerce capabilities, and localized collections tailored to Asian consumer preferences. The continued growth of affluent middle-class populations throughout the region is expected to create significant revenue opportunities over the next decade.

Sustainable and Traceable Fur Product Development

Manufacturers investing in certified sourcing, animal welfare standards, and supply chain transparency can unlock substantial competitive advantages. Luxury consumers increasingly value authenticity and ethical production credentials. Companies implementing blockchain verification systems, traceable raw material sourcing, and independently audited welfare programs are likely to gain stronger acceptance among premium buyers. Sustainable production initiatives can also help mitigate reputational risks while improving long-term market positioning.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.45 Billion |

| Market Size in 2026 | USD 5.66 Billion |

| Market Size in 2031 | USD 6.82 Billion |

| CAGR | 3.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Fur Type Insights

Mink fur coats dominate the global fur coat market, accounting for approximately 38% of total revenue in 2025, making them the largest fur type segment worldwide. The segment's leadership is primarily driven by the superior balance of softness, lightweight characteristics, durability, and luxurious appearance that mink fur offers compared to other natural fur materials. Mink fur has long been considered the benchmark for luxury outerwear and continues to enjoy strong demand among affluent consumers in China, South Korea, Russia, Italy, and North America. In addition, mink garments possess excellent insulation properties while maintaining a refined aesthetic, making them suitable for both fashion-oriented and functional winter wear applications.

The segment also benefits from strong brand adoption among luxury fashion houses, which continue to incorporate mink fur into premium collections due to its versatility and ability to support high-margin pricing strategies. Furthermore, the growth of luxury consumption in Asia-Pacific and the increasing demand for premium outerwear among high-net-worth individuals continue to reinforce mink fur's market leadership. Fox fur coats remain the second-largest segment due to their distinctive texture, longer hair structure, and widespread use in luxury trims and statement fashion pieces. Rabbit fur products maintain steady demand within mid-premium price categories due to their affordability and accessibility, while chinchilla and sable fur occupy ultra-luxury niches characterized by limited supply, exclusivity, and exceptionally high retail pricing. Shearling and lamb fur products are experiencing growing adoption among younger consumers due to their combination of luxury aesthetics, practicality, and contemporary fashion appeal.

Product Type Insights

Full-length fur coats accounted for approximately 34% of global market revenue in 2025, making them the leading product category. Their dominance is largely attributed to premium pricing structures, strong luxury positioning, and continued demand from consumers residing in cold-weather regions. Full-length coats typically utilize larger quantities of premium fur materials, resulting in significantly higher average selling prices than shorter garment formats. This allows manufacturers and luxury brands to generate higher revenue contributions from the segment despite comparatively lower sales volumes.

Demand for full-length fur coats remains particularly strong in Northern Europe, Russia, Canada, Northern China, and other regions experiencing prolonged winter seasons where consumers prioritize both thermal performance and luxury appeal. The segment additionally benefits from its status as a traditional luxury investment piece, often viewed as a long-term wardrobe asset rather than a seasonal fashion purchase. Mid-length fur coats continue gaining popularity among urban consumers seeking a balance between functionality and contemporary styling. Meanwhile, short fur jackets are experiencing rapid growth among younger luxury buyers due to their versatility, lighter weight, and compatibility with modern fashion trends. Reversible fur garments, bespoke designs, and custom-made collections are also witnessing increasing demand as consumers seek personalized luxury experiences and unique fashion statements.

Distribution Channel Insights

Brand-owned retail stores accounted for nearly 29% of global fur coat sales in 2025, making them the leading distribution channel within the industry. The segment's dominance is driven by the premium nature of fur coat purchases, where consumers often require personalized consultations, product authentication, customization services, and assurance regarding material quality before committing to high-value transactions. Luxury consumers generally prefer purchasing directly from flagship stores and brand boutiques because these channels provide exclusive collections, superior customer service, and stronger brand experiences.

The continued expansion of luxury retail infrastructure in major metropolitan markets such as Shanghai, Beijing, Dubai, Milan, Paris, New York, and Seoul has further strengthened this channel's position. Additionally, direct retail stores allow brands to maintain pricing control, enhance customer loyalty, and improve profit margins compared to third-party retail arrangements. Luxury department stores continue to play a significant role, particularly in North America and Europe, where consumers frequently purchase premium outerwear through established luxury retail networks. E-commerce represents the fastest-growing channel, supported by advances in virtual consultations, digital product visualization, authentication technologies, and cross-border luxury commerce. Meanwhile, authenticated resale platforms and luxury vintage marketplaces are becoming increasingly important contributors to market growth by extending product life cycles and attracting sustainability-conscious consumers.

Consumer Group Insights

Affluent consumers represented approximately 47% of global fur coat demand in 2025, making them the largest consumer segment. The dominance of this group is primarily driven by rising disposable incomes, increasing luxury consumption, and growing interest in premium lifestyle products. Affluent consumers often seek products that combine exclusivity, craftsmanship, heritage value, and status symbolism, characteristics that align closely with luxury fur garments.

The expansion of upper-middle-income and affluent populations across China, the United States, South Korea, Japan, the UAE, and key European economies continues to strengthen demand from this segment. Additionally, growing participation in luxury fashion events, designer collections, and premium retail experiences further reinforces purchasing activity among affluent buyers. High-net-worth individuals remain a particularly lucrative segment due to their preference for bespoke garments, ultra-luxury fur types, and limited-edition designer products. Fashion-oriented consumers continue supporting seasonal demand through luxury apparel purchases influenced by celebrity endorsements and runway trends. Furthermore, collectors and vintage luxury enthusiasts are emerging as increasingly important customer groups due to the growing popularity of authenticated resale markets and investment-grade luxury fashion products.

End-Use Insights

Luxury fashion applications accounted for approximately 58% of total fur coat market demand in 2025, making them the largest end-use segment globally. The segment's leadership is primarily driven by the continued perception of fur coats as premium status symbols that communicate exclusivity, wealth, and luxury craftsmanship. Luxury fashion houses continue incorporating fur garments into seasonal collections, reinforcing consumer demand across established and emerging luxury markets.

The increasing concentration of wealth among affluent consumer groups, coupled with rising luxury apparel expenditure across Asia-Pacific and the Middle East, remains a key growth driver for this segment. Fur coats are frequently positioned as long-term investment garments due to their durability, heritage value, and premium material composition. Winter protection apparel remains the second-largest application segment, particularly in colder geographies where superior thermal insulation supports functional demand. Celebrity styling, film production, luxury editorial campaigns, and red-carpet appearances further contribute to market visibility and aspirational purchasing behavior. Additionally, rental services, luxury wardrobe subscription models, and authenticated vintage marketplaces are creating new demand streams that are expected to support long-term market expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Fur Coat Market Segmentations

By Fur Type

- Mink Fur Coats

- Fox Fur Coats

- Rabbit Fur Coats

- Chinchilla Fur Coats

- Sable Fur Coats

- Shearling & Lamb Fur Coats

- Raccoon Fur Coats

- Beaver Fur Coats

- Mixed-Fur Fur Coats

- Other Specialty Fur Coats

By Product Type

- Full-Length Fur Coats

- Mid-Length Fur Coats

- Short Fur Jackets

- Fur Vests

- Reversible Fur Coats

- Custom-Made Fur Coats

- Designer/Luxury Fur Coats

By Gender

- Women’s Fur Coats

- Men’s Fur Coats

- Unisex Fur Coats

By Price Category

- Ultra-Luxury (Above USD 10,000)

- Premium Luxury (USD 5,000–10,000)

- Mid-Premium (USD 2,000–5,000)

- Entry Luxury (Below USD 2,000)

By Distribution Channel

- Brand-Owned Retail Stores

- Department Stores

- Specialty Luxury Retailers

- E-Commerce Platforms

- Multi-Brand Fashion Boutiques

- Auction & Vintage Channels

Regional Insights

Europe

Europe accounted for approximately 33% of global fur coat market revenue in 2025, maintaining its position as the largest regional market. The region benefits from a unique combination of luxury fashion leadership, established manufacturing expertise, and strong consumer demand for premium outerwear. Italy remains the dominant market due to its concentration of luxury fashion houses, high-end garment manufacturing capabilities, and strong export presence. Greece continues to serve as one of the world's most important fur garment production and processing hubs, supplying products to international luxury markets.

Demand across Germany, France, Switzerland, and the Nordic countries is supported by high disposable incomes, mature luxury retail infrastructure, and a strong preference for premium apparel. Cold winter conditions across Northern and Eastern Europe also contribute to functional demand for high-performance outerwear. Additionally, Europe's leadership in luxury fashion innovation, designer collections, and heritage craftsmanship continues to support premium product sales. The presence of globally recognized luxury brands and established distribution networks remains one of the region's most important competitive advantages.

Asia-Pacific

Asia-Pacific accounted for approximately 31% of global demand in 2025 and represents the fastest-growing regional market, with growth significantly outpacing mature Western markets. China remains the largest country-level market globally, accounting for nearly 20% of worldwide fur coat consumption. The region's growth is driven primarily by rapid wealth creation, expanding upper-middle-class populations, increasing luxury brand penetration, and rising discretionary spending on premium fashion products.

South Korea and Japan continue to exhibit strong demand for luxury outerwear, supported by sophisticated fashion industries and high consumer spending on designer apparel. Increasing urbanization, luxury mall development, and the expansion of digital luxury commerce platforms have improved product accessibility throughout the region. Additionally, cultural acceptance of luxury status products and growing participation in global fashion trends continue driving demand. Asia-Pacific is expected to remain the fastest-growing region due to sustained economic growth, luxury market expansion, and increasing numbers of affluent consumers entering premium fashion categories.

North America

North America accounted for approximately 20% of global market revenue in 2025, with the United States representing the region's largest consumer market. Demand is supported by a well-established luxury fashion ecosystem, high disposable income levels, and strong spending on premium outerwear products. The presence of major luxury retailers, department stores, and designer boutiques provides extensive distribution coverage across the region.

Canada contributes significantly to regional demand due to harsh winter conditions that support functional demand for high-performance outerwear. Another important growth driver is the rapid expansion of authenticated luxury resale platforms, which have increased consumer access to premium and vintage fur garments. Furthermore, increasing interest in investment-grade fashion products and luxury collectibles is supporting demand among affluent consumers. Despite growing popularity of sustainable alternatives, premium consumers continue to purchase fur garments based on quality, craftsmanship, and heritage value.

Latin America

Latin America represented approximately 7% of global fur coat demand in 2025, with Brazil, Mexico, Argentina, and Chile serving as the region's primary luxury consumption markets. Although climatic conditions limit widespread functional demand, increasing luxury fashion adoption among affluent urban populations continues supporting market growth. Major metropolitan centers such as São Paulo, Mexico City, Buenos Aires, and Santiago remain important hubs for premium apparel consumption.

The expansion of luxury retail infrastructure, increasing international tourism, and growing exposure to global fashion trends are key drivers supporting regional demand. Additionally, rising numbers of high-net-worth individuals and expanding luxury brand presence across major cities continue contributing to market development. While the market remains relatively niche compared to Europe and Asia-Pacific, luxury-focused consumption patterns are expected to support steady long-term growth.

Middle East & Africa

The Middle East and Africa accounted for approximately 9% of global market revenue in 2025, driven primarily by luxury consumption rather than climatic necessity. The UAE, Saudi Arabia, Qatar, and Kuwait represent the largest regional markets due to high levels of wealth concentration and strong demand for prestige-oriented luxury products. Fur coats are frequently purchased as fashion and status symbols among affluent consumers seeking exclusivity and premium craftsmanship.

The region's growth is supported by the rapid expansion of luxury retail developments, premium shopping destinations, and international fashion events. Dubai, in particular, has emerged as a major luxury retail hub attracting high-spending consumers from across the Middle East, Africa, and Asia. Increasing tourism, growing luxury expenditure, and continued wealth generation among ultra-high-net-worth individuals remain the primary drivers of regional market growth. Additionally, luxury brands continue expanding their direct retail presence throughout the Gulf Cooperation Council countries, further strengthening demand for premium outerwear products.

Key Players in the Fur Coat Market

- Fendi

- Yves Salomon

- Prada

- Max Mara

- Saga Furs

- Dennis Basso

- Braschi

- Simonetta Ravizza

- Helen Yarmak

- Kopenhagen Fur Design Partners

- Valentino

- Loro Piana

- J. Mendel

- Giuliana Teso

- Revillon