Global Food and Grocery Retail Market Size

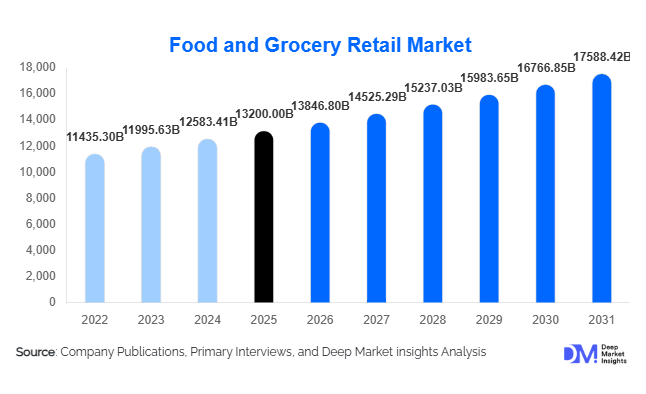

According to Deep Market Insights, the global food and grocery retail market size was valued at USD 13200 billion in 2026 and is projected to grow from USD 13846.80 billion in 2026 to reach USD 17588.42 billion by 2031, expanding at a CAGR of 4.9% during the forecast period (2026–2031). The market growth is primarily driven by rapid urbanization, rising disposable incomes, expansion of organized retail infrastructure, and the accelerated adoption of omni-channel and quick-commerce grocery delivery models across global economies.The food and grocery retail industry continues to represent the backbone of global consumer spending, as food remains an essential and non-discretionary expenditure category. The market is undergoing a structural transformation, shifting from traditional kirana stores and wet markets toward organized supermarkets, hypermarkets, and digital grocery platforms. Increasing demand for convenience, speed, and product variety is reshaping retail formats worldwide. Developed regions such as North America and Europe are characterized by highly organized retail ecosystems, while Asia Pacific is witnessing rapid expansion due to urban population growth and rising middle-class consumption. Emerging economies in Latin America, the Middle East, and Africa are also experiencing steady modernization of retail infrastructure, supported by government investments and foreign direct investment inflows.Technological integration has become a defining force in the market, with AI-driven inventory systems, automated warehouses, and data-based personalized promotions improving operational efficiency. Online grocery retail and quick-commerce platforms are among the fastest-growing segments, significantly altering consumer purchasing behavior. Additionally, increasing demand for organic, healthy, and sustainable food products is driving premiumization across multiple product categories. Despite challenges such as inflationary pressures and supply chain disruptions, the global food and grocery retail market is expected to maintain stable and sustained growth over the forecast period.

Key Market Insights

- Supermarkets and hypermarkets remain the dominant retail formats, accounting for the largest share of global grocery sales due to wide product assortment and strong pricing efficiency.

- Online grocery and quick-commerce platforms are the fastest-growing channels, driven by urban consumer demand for convenience and rapid delivery services.

- Asia Pacific leads global market demand, supported by large population bases, rising incomes, and rapid expansion of organized retail in China and India.

- North America and Europe are highly mature, technology-driven markets with strong penetration of premium, organic, and private-label grocery products.

- Private-label brands are gaining strong traction globally as consumers shift toward cost-effective alternatives during inflationary cycles.

- AI, automation, and data analytics are transforming retail operations through improved inventory forecasting, pricing optimization, and customer personalization.

Global Food and Grocery Retail Market Latest Trends

Rapid Expansion of E-Grocery and Quick Commerce

The food and grocery retail sector is witnessing a structural shift toward online and quick-commerce platforms. Urban consumers increasingly prefer instant delivery models for essential groceries, driving hyperlocal fulfillment networks and automated warehousing systems. Retailers are investing heavily in micro-fulfillment centers to reduce delivery times and improve order accuracy. This trend is especially strong in densely populated cities across Asia-Pacific and North America, where digital penetration and mobile-first shopping behavior are highest. The integration of AI-based demand forecasting is also improving stock availability and reducing wastage.

Rise of Private-Label and Value-Based Retailing

Private-label products are emerging as a key growth driver across global grocery retail. Consumers are increasingly shifting toward retailer-owned brands due to affordability and comparable quality with established FMCG brands. Large retailers are expanding their private-label portfolios across fresh food, packaged goods, and household essentials. This trend is strengthening profit margins for retailers while intensifying competition with branded manufacturers. Inflationary pressures have further accelerated demand for value-based grocery solutions, especially in Europe and North America.

Global Food and Grocery Retail Market Drivers

Urbanization and Changing Consumer Lifestyles

Rising urban populations are significantly increasing dependency on organized grocery retail formats such as supermarkets and convenience stores. Busy lifestyles and dual-income households are driving demand for ready-to-eat meals, packaged foods, and home delivery services. This structural shift is boosting consistent demand for organized retail chains and digital grocery platforms across global cities.

Expansion of Organized Retail Infrastructure

The global expansion of organized retail chains is improving accessibility and product availability. International retailers are aggressively entering emerging markets, while domestic players are scaling operations through franchise and hybrid models. This expansion is reducing reliance on fragmented traditional retail and increasing market consolidation across major economies.

Growth of Digital Grocery Ecosystems

The integration of mobile apps, AI-driven recommendation engines, and automated logistics systems is transforming grocery retail operations. Online grocery platforms are enhancing customer convenience and increasing purchase frequency, particularly in urban regions. Digital payment adoption and improved internet penetration are further accelerating this shift globally.

Global Food and Grocery Retail Market Restraints

Low Profit Margins and High Competition

The grocery retail industry operates on structurally thin margins, typically ranging between 1.5% and 5%. Intense price competition among global and regional players often leads to pricing pressure, limiting profitability. Retailers must rely heavily on scale, operational efficiency, and supply chain optimization to sustain margins.

Supply Chain Disruptions and Cost Volatility

Global food retail is highly dependent on agricultural supply chains, which are vulnerable to climate change, geopolitical instability, and transportation cost fluctuations. These disruptions create inventory management challenges and impact pricing stability, especially for fresh and imported goods.

Global Food and Grocery Retail Market Key Opportunities

Expansion in Emerging Markets

Emerging economies across Asia-Pacific, Africa, and Latin America present significant expansion opportunities due to rising middle-class populations and increasing urbanization. Organized retail penetration remains relatively low in these regions, offering strong long-term growth potential for global retail chains and investors.

AI-Driven Retail Transformation

The adoption of artificial intelligence and predictive analytics is creating opportunities for demand forecasting, inventory optimization, and personalized shopping experiences. Retailers leveraging advanced analytics can reduce wastage, improve efficiency, and enhance customer engagement across both online and offline channels.

Sustainability and Health-Focused Grocery Demand

Growing consumer preference for organic, plant-based, and sustainably sourced food products is creating new revenue streams. Retailers investing in eco-friendly packaging, carbon-neutral supply chains, and health-focused private labels are gaining strong competitive advantage globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13200.00 Billion |

| Market Size in 2026 | USD 13846.80 Billion |

| Market Size in 2031 | USD 17588.42 Billion |

| CAGR | 4.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Packaged and processed foods dominate the global grocery retail market, accounting for approximately 28% of total market share. This leadership is primarily driven by accelerating urbanization, changing dietary habits, and increasing reliance on convenience-oriented consumption, particularly among working populations with limited time for traditional food preparation. The expansion of cold chain logistics and improved shelf stability technologies has further strengthened this segment’s dominance across both developed and emerging economies.Fresh food holds around 22% share, supported by strong daily household demand and the continued importance of localized sourcing ecosystems. Its growth is underpinned by rising consumer preference for minimally processed, clean-label, and locally sourced produce, especially in urban centers where farmers’ markets and organized fresh retail formats are expanding. Dairy and bakery categories remain structurally stable contributors, benefiting from consistent household penetration and recurring consumption cycles, while frozen foods are expanding at a faster pace due to increasing demand for long-shelf-life products, reduced food waste considerations, and the growing penetration of modern retail refrigeration infrastructure. Beverages and household essentials continue to represent high-frequency basket contributors, reinforced by brand loyalty and replenishment-driven purchase behavior across all income segments.

Application Insights

Household consumption remains the dominant application segment, accounting for the majority of global grocery retail demand. This dominance is reinforced by population growth, rising middle-class expenditure, and the increasing shift toward branded and organized retail purchases over traditional unorganized channels.The HoReCa segment is expanding at a strong pace, driven by structural growth in food service industries, tourism recovery, and evolving urban dining culture. Increasing reliance of restaurants and catering services on organized supply chains has further strengthened procurement standardization and bulk purchasing behavior. Institutional demand from corporate cafeterias, hospitals, and educational institutions is also rising steadily, supported by outsourcing trends and growing emphasis on hygiene-compliant, centrally managed food procurement systems.Export-driven grocery trade is gaining strategic importance, particularly for packaged foods, dairy products, and processed ingredients exported from developed economies to emerging markets. This trend is supported by globalization of food supply chains, improved regulatory harmonization, and rising cross-border demand for branded and shelf-stable grocery products.

Distribution Channel Insights

Offline retail continues to dominate the grocery ecosystem with approximately 78% share, anchored by supermarkets, hypermarkets, and convenience stores. The strength of offline channels is reinforced by immediate product availability, consumer trust in physical inspection, and strong penetration in semi-urban and rural markets where digital adoption is still evolving. Large retail networks such as :contentReference[oaicite:0]{index=0}, :contentReference[oaicite:1]{index=1}, and :contentReference[oaicite:2]{index=2} continue to shape global retail standards through scale efficiencies and advanced supply chain integration.However, online grocery platforms are expanding rapidly, driven by quick commerce models, subscription-based replenishment services, and continuous improvements in last-mile logistics infrastructure. Hybrid formats such as click-and-collect are gaining strong traction in urban environments where consumers seek both convenience and flexibility. Digital marketplaces and retailer-owned applications are accelerating omnichannel transformation, reshaping purchase behavior toward digitally influenced, data-driven grocery consumption.

Explore more data points, trends and opportunities Download Free Sample Report

Food and Grocery Retail Market Segmentations

By Product Category

- Fresh Food

- Packaged & Shelf-Stable Food

- Frozen Food

- Beverages

- Household & Personal Care Essentials

- Organic & Specialty Grocery Products

By Retail Format

- Supermarkets

- Hypermarkets

- Convenience Stores

- Discount Stores

- Warehouse Clubs & Cash-and-Carry

- Online Grocery Retail

- Specialty Grocery Stores

By Business Model

- Organized Retail

- Unorganized Retail

- Omni-Channel Retail

- Franchise & Cooperative Retail

By Customer Type

- Household Consumers

- HoReCa

- Institutional Buyers

- Small Retail Resellers

By Pricing Positioning

- Economy Segment

- Mid-Priced Segment

- Premium Grocery Segment

- Luxury & Gourmet Segment

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the global grocery retail market at approximately 42%, with China, India, and Southeast Asia serving as key growth engines. The region’s expansion is primarily driven by rapid urbanization, a large and growing population base, rising disposable incomes, and significant expansion of modern retail infrastructure. India is emerging as one of the fastest-growing markets, supported by accelerated retail modernization, increasing penetration of e-grocery platforms, and improving logistics and cold-chain networks. China continues to lead in scale and digital adoption, with highly developed e-commerce ecosystems and strong integration of online grocery platforms into daily consumer behavior. Southeast Asian countries are witnessing robust growth due to expanding middle-class populations, increasing foreign retail investments, and rapid development of organized retail formats. Overall regional growth is strongly supported by digital transformation in retail, rising demand for convenience foods, and continuous expansion of supermarket and hypermarket chains across urban centers.

North America

North America accounts for around 28% of the global market, with the United States representing the most significant contributor. The region’s growth is driven by high consumer purchasing power, mature and highly efficient retail infrastructure, and strong adoption of advanced supply chain and inventory management technologies. The presence of major retailers such as Walmart, Kroger, and Costco supports large-scale distribution efficiency and competitive pricing strategies. A key growth driver is the increasing penetration of private-label products, which offer cost-effective alternatives and strong retailer margins. The rapid expansion of e-grocery platforms, subscription-based delivery services, and omnichannel retail strategies is further reshaping consumer purchasing behavior. Additionally, demand for organic, health-oriented, and premium grocery products continues to grow, supported by rising health consciousness and lifestyle-oriented consumption trends.

Europe

Europe represents nearly 20% of the global grocery retail market, with Germany, the United Kingdom, and France acting as primary contributors. The region’s growth is significantly influenced by strong discount retail penetration, led by major players such as Aldi and Lidl under the Schwarz Group, which have reshaped consumer expectations around pricing and value-driven purchasing. Sustainability considerations are a major structural driver in Europe, with increasing demand for organic, locally sourced, and environmentally friendly products influencing retail strategies. Regulatory frameworks promoting food safety, labeling transparency, and carbon footprint reduction further shape market dynamics. Inflationary pressures have also strengthened demand for private-label and discount formats, as consumers prioritize affordability without compromising quality. Additionally, digital grocery adoption is steadily increasing, supported by improved logistics and growing omnichannel integration across major retail chains.

Latin America

Latin America, led by Brazil, Mexico, and Argentina, is experiencing steady growth driven by urbanization, rising middle-class consumption, and gradual formalization of retail structures. The transition from traditional small-scale retail to organized supermarket chains is a key structural driver of market expansion. Improvements in logistics infrastructure and supply chain efficiency are enhancing product availability across urban and semi-urban regions. Financial technology adoption, including digital payments and mobile wallets, is further supporting retail modernization and facilitating online grocery adoption in major cities. Although offline retail remains dominant, e-grocery platforms are gradually gaining traction, particularly among younger consumers seeking convenience and competitive pricing. The region’s growth is also supported by increasing foreign investment in retail infrastructure and expanding presence of multinational grocery chains.

Middle East & Africa

The Middle East and Africa region is emerging as a high-growth market, driven by rising import dependency, expanding urban populations, and significant investments in retail infrastructure development. Countries such as the United Arab Emirates, Saudi Arabia, South Africa, and Nigeria are witnessing strong growth in supermarket and hypermarket penetration. A major growth driver is increasing consumer demand for imported packaged foods and premium grocery products, supported by rising income levels and changing consumption patterns. Tourism expansion, particularly in Gulf Cooperation Council (GCC) countries, is also contributing to higher demand for diverse food categories. Infrastructure development in logistics and cold-chain systems is improving supply chain efficiency, enabling better availability of perishable and frozen goods. Additionally, rapid urbanization and government-led economic diversification initiatives are accelerating the shift toward modern retail formats and organized grocery distribution networks.