Private Label Food And Beverages Market Size

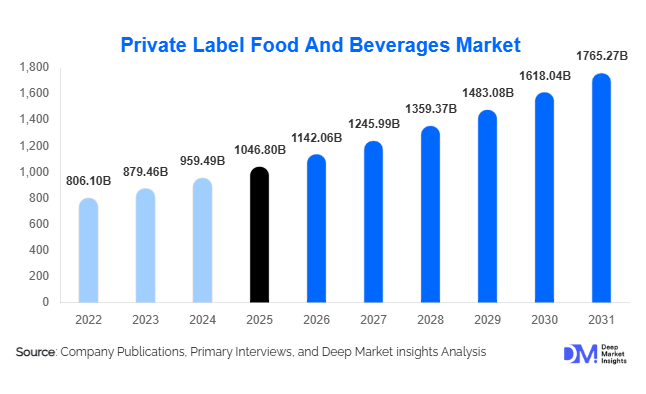

According to Deep Market Insights, the global private label food and beverages market size was valued at USD 1,142.06 billion in 2025 and is projected to grow from USD 1,765.27 billion in 2026 to reach USD 1,742.6 billion by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). The private label food and beverages market growth is primarily driven by increasing consumer preference for value-oriented products, expanding organized retail infrastructure, and growing demand for premium, organic, and clean-label store-brand offerings across developed and emerging economies.

Key Market Insights

- Private label food and beverage products are increasingly shifting toward premiumization and health-focused positioning, with retailers launching organic, plant-based, and functional offerings to compete directly with branded manufacturers.

- Retail chains are aggressively expanding proprietary food portfolios, leveraging higher profit margins, improved customer loyalty, and enhanced shelf visibility through exclusive store-brand products.

- Europe dominates the global market, supported by strong consumer trust in retailer-owned brands and highly mature supermarket ecosystems.

- Asia-Pacific remains the fastest-growing regional market, driven by rapid urbanization, organized retail expansion, and rising middle-class consumption in China and India.

- Online grocery and digital retail ecosystems are reshaping private label adoption, enabling retailers to promote store brands through subscription models, loyalty programs, and personalized recommendations.

- Sustainable packaging and ethical sourcing initiatives are becoming major competitive differentiators, encouraging investment in recyclable materials, local sourcing, and clean-label production.

private label food and beverages market latest trends

Premium and Health-Oriented Private Labels Gaining Momentum

Private label food and beverages are increasingly moving beyond economy positioning toward premium and wellness-focused offerings. Retailers are introducing gourmet ready meals, plant-based beverages, functional snacks, gluten-free bakery products, and organic dairy alternatives that compete directly with multinational branded products. Consumers are showing greater willingness to purchase retailer-owned products when quality, nutritional value, and sustainability credentials are clearly communicated. Clean-label ingredients, reduced sugar formulations, and high-protein foods are becoming central to new product launches. Premium private label portfolios are also expanding across frozen foods, coffee, confectionery, and wellness beverages, helping retailers improve margins while strengthening brand loyalty among health-conscious consumers.

Digital Grocery Platforms Accelerating Store Brand Penetration

The rapid expansion of online grocery retail and quick-commerce platforms is significantly reshaping private label purchasing behavior. Retailers are increasingly using AI-powered recommendation engines, personalized loyalty programs, and dynamic pricing tools to promote proprietary food and beverage products across digital channels. Subscription-based grocery delivery models are also strengthening recurring demand for retailer-owned staples and packaged foods. Mobile apps and digital storefronts now provide nutritional transparency, sustainability ratings, and consumer reviews that improve confidence in private label purchases. Social media marketing and influencer partnerships are further accelerating awareness of premium store brands among younger consumers, particularly millennials and Gen Z shoppers who prioritize affordability alongside convenience and product quality.

private label food and beverages market drivers

Rising Consumer Preference for Value-Based Purchasing

Global inflationary pressures and rising food costs are driving consumers toward affordable alternatives without compromising quality. Private label products typically maintain a price advantage of 15–30% compared to equivalent branded products, making them highly attractive during periods of economic uncertainty. Improvements in product quality, packaging aesthetics, and flavor innovation have significantly changed consumer perception, allowing private label food and beverage products to gain broader acceptance across income groups. Consumers increasingly view retailer-owned products as credible substitutes rather than low-cost alternatives, particularly in packaged foods, dairy products, frozen meals, and beverages.

Expansion of Organized Retail and Modern Grocery Infrastructure

The rapid growth of supermarkets, hypermarkets, warehouse clubs, and discount retailers is accelerating global private label adoption. Retailers are dedicating larger shelf space to proprietary products because of their higher profitability and stronger customer retention potential. Modern retail chains are also leveraging advanced analytics to identify high-demand categories and launch customized store-brand products faster than traditional branded manufacturers. Emerging economies such as India, China, Brazil, and Indonesia are witnessing rapid organized retail penetration, creating favorable conditions for expansion of private label food and beverage portfolios.

global market restraints

Supply Chain Volatility and Raw Material Cost Fluctuations

Private label manufacturers remain highly sensitive to fluctuations in agricultural commodity prices, packaging material costs, and transportation expenses. Since many retailer-owned products operate under competitive pricing models with narrower margins, disruptions in global supply chains can significantly impact profitability. Rising prices of edible oils, dairy ingredients, grains, and sustainable packaging materials continue creating operational challenges for manufacturers and retailers. Geopolitical instability and climate-related disruptions affecting agricultural production further intensify supply-side uncertainty within the market.

Strong Brand Loyalty Toward Established Manufacturers

Despite growing consumer acceptance, several food and beverage categories remain heavily dominated by multinational brands with strong customer loyalty and extensive marketing investments. Premium carbonated beverages, infant nutrition, luxury confectionery, and specialty packaged foods continue witnessing higher dependence on established global brands. In emerging economies, branded products are often associated with superior quality and aspirational value, creating challenges for private label penetration. Retailers must continuously invest in quality improvement, packaging innovation, and marketing campaigns to compete effectively against well-established manufacturers.

private label food and beverages industry key opportunities

Growth of Sustainable and Ethical Food Portfolios

The growing consumer emphasis on sustainability and responsible sourcing is creating significant opportunities for private label manufacturers and retailers. Consumers increasingly prefer recyclable packaging, locally sourced ingredients, carbon-neutral production, and transparent supply chains. Retailers are responding by launching sustainable private label product lines with eco-friendly packaging and ethical sourcing certifications. Partnerships with local agricultural producers are also strengthening supply-chain resilience while supporting regional economies. Governments in Europe and Asia are encouraging sustainable food manufacturing through waste reduction initiatives and packaging regulations, further expanding opportunities for environmentally responsible private label products.

Emerging Market Retail Expansion

Emerging economies represent one of the largest long-term opportunities for the private label food and beverages market. Rapid urbanization, rising disposable incomes, and expanding middle-class populations are driving supermarket penetration and modern grocery adoption across Asia-Pacific, Latin America, and the Middle East. Retailers entering these markets are increasingly prioritizing proprietary product portfolios to differentiate themselves and improve profitability. Localized private label offerings tailored to regional tastes and dietary preferences are gaining traction, particularly in packaged foods, dairy, snacks, and beverages. E-commerce grocery platforms are also enabling retailers to scale store-brand penetration faster in underserved urban and semi-urban markets.

Product Type Insights

Food products continue to dominate the private label food and beverages market, accounting for nearly 68% of global revenue in 2025, primarily driven by rising price sensitivity among consumers, expanding supermarket private label penetration, and continuous improvements in retailer-owned product quality. Packaged foods, frozen meals, dairy products, bakery items, and snacks represent the largest revenue-generating categories due to strong household consumption patterns, increasing urbanization, and the strategic expansion of retailer shelf space dedicated to store brands. The leading growth driver for food products is the rising consumer shift toward value-for-money alternatives that offer comparable quality to branded products at significantly lower prices, further reinforced by inflationary pressures in major economies.Frozen ready-to-eat meals are experiencing particularly strong growth as urban consumers increasingly adopt convenience-oriented lifestyles, longer working hours, and time-saving meal solutions. Within beverages, functional and wellness beverages are emerging as the fastest-growing category, driven by rising demand for probiotic drinks, plant-based milk alternatives, fortified beverages, and reduced-sugar formulations. The primary growth driver in this segment is heightened consumer awareness regarding preventive healthcare and nutrition, especially among millennials and Gen Z populations. Premium private label coffee and tea portfolios are also expanding rapidly as consumers seek café-style experiences at affordable prices, supported by retail innovation and premiumization strategies. Organic and clean-label products are becoming central to innovation strategies, particularly in Europe and North America, where regulatory support, health consciousness, and sustainability-driven consumption are accelerating demand.

Application Insights

Household consumption remains the largest application segment within the private label food and beverages market, driven by growing grocery purchases through supermarkets, discount retailers, and online grocery platforms. The leading driver for this segment is sustained consumer preference for affordable daily essentials amid rising living costs, coupled with increasing trust in retailer-owned brands due to improved quality assurance and branding strategies. Consumers increasingly prefer store-brand packaged foods, dairy products, snacks, and beverages for everyday consumption, supported by frequent promotions and expanding product assortments.Foodservice and hospitality applications are also witnessing substantial growth as hotels, restaurants, and quick-service chains increasingly source private label ingredients and beverages to optimize operating costs and maintain consistent quality standards. The key driver in this segment is cost optimization pressure across the hospitality industry combined with supply chain flexibility requirements. Institutional catering applications across schools, hospitals, airlines, and corporate cafeterias are expanding steadily due to demand for standardized, cost-efficient food procurement solutions and large-volume supply contracts. Functional food and beverage applications linked to health and wellness trends are emerging as high-growth areas, particularly for protein-rich foods, plant-based beverages, and nutritional snack products, supported by rising preventive healthcare awareness and institutional wellness programs.

Distribution Channel Insights

Hypermarkets and supermarkets dominate the private label food and beverages market, accounting for over 52% of global sales in 2025 due to strong shelf visibility, aggressive promotional strategies, and wide product assortments. The leading growth driver for this channel is retailer-led private label expansion strategies aimed at increasing margins and strengthening customer loyalty through exclusive in-store offerings. Discount retailers continue gaining market share by offering competitively priced store-brand products across essential food categories, supported by consumer demand for cost savings and value purchasing behavior.Online retail and e-commerce grocery platforms are emerging as the fastest-growing distribution channels, driven by digital adoption, home delivery convenience, and AI-powered personalized recommendations that enhance product discovery and repeat purchases. Direct-to-consumer grocery platforms are also expanding as retailers strengthen digital ecosystems and data-driven engagement strategies. Wholesale and cash-and-carry channels remain important for institutional buyers and small businesses seeking bulk procurement efficiency, supported by growing demand from foodservice operators and independent retailers.

Consumer Category Insights

Mass-market consumers represent the largest consumer category for private label food and beverages due to widespread demand for affordable packaged foods and grocery staples. The primary driver for this segment is persistent cost sensitivity among households, reinforced by inflationary pressures and increased availability of high-quality private label alternatives across retail formats. Budget-conscious households continue driving strong demand across economy and mid-tier private label portfolios, supported by expanding retailer penetration in emerging and developed markets alike.Health-conscious consumers are emerging as a rapidly growing segment, driven by increasing awareness of nutrition, clean-label ingredients, and lifestyle-related health concerns. Millennials and Gen Z consumers are significantly influencing product innovation by prioritizing sustainability, transparency, and ethically sourced ingredients, making them a key driver for premiumization and clean-label product expansion. Premium consumers are also contributing to market growth through rising demand for gourmet retailer-owned products, artisanal bakery items, premium coffee blends, and specialty beverages that offer high-quality experiences at lower price points compared to branded premium alternatives.

Packaging Type Insights

Flexible packaging dominates the private label food and beverages market due to cost efficiency, lightweight transportation advantages, and suitability across snacks, frozen foods, bakery products, and dry grocery items. The leading driver for flexible packaging is operational efficiency combined with retailer demand for reduced logistics costs and improved shelf-life performance. Bottles and cartons remain highly preferred for beverages, dairy products, and liquid food applications, supported by consumer convenience and product protection requirements.Sustainable packaging solutions are rapidly gaining traction as retailers prioritize recyclable, compostable, and biodegradable materials in response to environmental regulations and evolving consumer expectations. The primary driver for this shift is increasing sustainability commitments by global retailers and growing consumer preference for environmentally responsible packaging. Smart packaging technologies, including QR-code traceability and freshness indicators, are also emerging across premium private label food categories, driven by demand for transparency and food safety assurance. Glass containers continue maintaining strong demand in premium beverages, sauces, and gourmet packaged foods where product presentation, premium perception, and recyclability are key value drivers.

| By Product Type | By Pricing Tier | Distribution Channel | By Consumer Category | By Packaging Type |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for nearly 29% of the global private label food and beverages market in 2025, led primarily by the United States and Canada. The leading growth driver in this region is inflation-driven consumer trade-down behavior, where shoppers increasingly shift from branded products to high-quality private label alternatives to manage household budgets. The United States alone contributed approximately 24% of global demand due to strong supermarket penetration, aggressive retailer private label expansion strategies, and increasing consumer trust in store-owned brands. Warehouse clubs and discount retailers are significantly expanding premium and organic store-brand portfolios across packaged foods, beverages, dairy products, and frozen meals, further strengthening market penetration. Canada is also witnessing rising adoption of clean-label and health-focused private label products, supported by strong consumer awareness regarding sustainability and wellness trends.

Europe

Europe remains the largest regional market, representing approximately 38% of global revenue in 2025, driven by highly mature retail ecosystems and deep consumer trust in retailer-owned brands. The key growth driver in Europe is the long-established dominance of supermarket chains and discount retailers, which actively promote private label offerings as core value propositions. Countries such as Germany, the United Kingdom, France, Spain, Italy, and the Netherlands maintain highly developed private label ecosystems supported by strong retail infrastructure and consistent product innovation. The United Kingdom contributed nearly 9% of global market revenues in 2025 due to aggressive private label expansion strategies by leading supermarket chains. Germany continues to lead discount retail penetration, while France and Spain are experiencing strong growth in premium organic retailer-owned products. Europe also leads globally in sustainable packaging adoption and clean-label innovation, driven by strict regulatory frameworks and environmentally conscious consumers.

Asia-Pacific

Asia-Pacific is projected to remain the fastest-growing regional market, expanding at a CAGR exceeding 11% during the forecast period, driven by rapid urbanization, rising disposable incomes, and expanding modern retail infrastructure. The primary growth driver in this region is the rapid expansion of organized retail and digital grocery platforms that are making private label products more accessible to a large and increasingly middle-class population. China and India are the primary growth engines due to strong urban migration and shifting consumption patterns toward branded-like affordability with improved quality perception. Chinese consumers are increasingly purchasing premium and imported-style private label foods through supermarket chains and digital grocery platforms. India is witnessing rapid expansion of supermarket-led private label portfolios in packaged foods, snacks, dairy products, and beverages. Japan and South Korea continue contributing through strong demand for premium convenience foods, while Southeast Asia is emerging as a major growth hub for affordable packaged food products supported by rapid retail modernization.

Latin America

Latin America is experiencing steady private label growth driven by inflationary pressures, currency volatility, and increasing supermarket penetration across Brazil, Mexico, Argentina, and Chile. The key growth driver in this region is persistent economic uncertainty, which is encouraging consumers to shift toward affordable store-brand staples and packaged foods. Retailers are expanding mid-tier private label product portfolios to attract value-conscious consumers while improving profitability and customer retention. Brazil remains the largest market within the region, supported by expanding discount retail formats, rising packaged food consumption, and increasing private label acceptance among middle-income households.

Middle East & Africa

The Middle East & Africa market is gradually expanding due to rising supermarket development, urbanization, and increasing demand for affordable packaged foods. The primary growth driver in this region is rapid retail modernization combined with rising population growth and changing dietary habits. Countries such as the UAE and Saudi Arabia are witnessing rising demand for premium imported-style private label products among high-income consumers, supported by strong retail investment and tourism-driven consumption. South Africa remains a major retail hub for private label food products within Africa due to established supermarket infrastructure and growing middle-class demand. Increasing investment in food manufacturing capabilities, cold-chain logistics, and retail expansion across the Gulf region is further supporting long-term market growth.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Private Label Food And Beverages Market

- Walmart Inc.

- Costco Wholesale Corporation

- The Kroger Co.

- Aldi Group

- Lidl Stiftung & Co. KG

- Tesco PLC

- Carrefour S.A.

- Target Corporation

- Amazon.com Inc.

- Albertsons Companies Inc.

- Edeka Group

- REWE Group

- Seven & i Holdings Co., Ltd.

- Aeon Co., Ltd.

- Marks and Spencer Group plc