Fresh Food Market Size

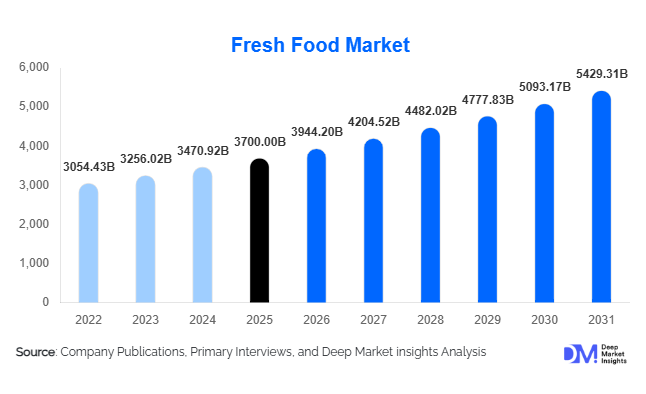

According to Deep Market Insights, the global fresh food market size was valued at USD 3,700.0 billion in 2025 and is projected to grow from USD 3,944.2 billion in 2026 to reach USD 5,429.31 billion by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The fresh food market growth is primarily driven by rising consumer preference for natural and minimally processed foods, increasing awareness of health and nutrition, and expanding cold chain and retail infrastructure globally.

Key Market Insights

- Fresh food demand is increasingly driven by health-conscious consumers, favoring natural, clean-label, and nutrient-rich food options.

- Asia-Pacific dominates the global market, supported by large population bases and rising disposable incomes in China and India.

- Supermarkets and hypermarkets remain the leading distribution channels, though online grocery platforms are rapidly gaining traction.

- Organic and sustainably sourced fresh food is witnessing strong growth, driven by premiumization trends in developed markets.

- Cold chain infrastructure expansion is reducing post-harvest losses and enabling global trade of perishable products.

- Technological integration, including AI-driven supply chain management and blockchain-based traceability, is improving efficiency and transparency.

What are the latest trends in the fresh food market?

Shift Toward Organic and Sustainable Fresh Food

Consumers are increasingly prioritizing organic, pesticide-free, and sustainably sourced fresh food products. This trend is particularly strong in North America and Europe, where environmental awareness and health concerns are driving demand for premium fresh produce. Farmers and producers are adopting regenerative agriculture practices, reducing chemical inputs, and improving soil health to meet evolving consumer expectations. Retailers are also promoting eco-friendly packaging and transparent sourcing, further strengthening the sustainability narrative across the fresh food value chain.

Digitalization and Growth of Online Fresh Food Retail

The rapid expansion of e-commerce platforms is transforming how consumers purchase fresh food. Online grocery platforms, direct-to-consumer farm models, and subscription-based delivery services are gaining popularity, offering convenience and freshness assurance. Advanced technologies such as AI-based demand forecasting, route optimization, and real-time inventory management are enhancing operational efficiency. This trend is particularly prominent in urban areas, where busy lifestyles and increasing internet penetration are accelerating online fresh food adoption.

What are the key drivers in the fresh food market?

Rising Health Awareness and Dietary Shifts

The increasing prevalence of lifestyle-related diseases has led consumers to adopt healthier eating habits, driving demand for fresh fruits, vegetables, and lean proteins. Fresh food is perceived as more nutritious and free from additives, making it a preferred choice among health-conscious individuals. This shift is further supported by government initiatives promoting balanced diets and nutritional awareness.

Urbanization and Rising Disposable Incomes

Rapid urbanization, particularly in emerging economies, is significantly influencing consumption patterns. Growing middle-class populations with higher disposable incomes are adopting diversified diets that include fresh meat, seafood, and dairy products. Urban consumers also demand convenience, leading to increased demand for pre-packaged and ready-to-cook fresh food options.

What are the restraints for the global market?

High Perishability and Supply Chain Complexity

Fresh food products are highly perishable, requiring efficient cold storage, transportation, and distribution systems. Inadequate infrastructure, particularly in developing regions, leads to significant post-harvest losses. Maintaining quality and freshness across long supply chains remains a major challenge for market participants.

Price Volatility and Climate Impact

The fresh food market is highly susceptible to seasonal variations, weather conditions, and climate change. Crop failures, fluctuating input costs, and supply-demand imbalances can lead to price volatility, impacting both producers and consumers. These uncertainties pose a challenge for long-term market stability.

What are the key opportunities in the fresh food industry?

Expansion of Cold Chain Infrastructure in Emerging Markets

Emerging economies in Asia-Pacific, Latin America, and Africa present significant opportunities for investment in cold chain logistics. Improving storage and transportation infrastructure can reduce food wastage, enhance supply chain efficiency, and ensure consistent product quality. Governments and private players are increasingly investing in refrigerated warehouses and transport systems, creating strong growth potential.

Growth of Direct-to-Consumer and Farm-to-Fork Models

Direct sourcing models that connect farmers with consumers are gaining traction globally. These models reduce intermediaries, improve profit margins for producers, and offer fresher products to consumers. Subscription-based fresh food delivery services and farmers' markets are expanding rapidly, particularly in urban areas, creating new revenue streams for market participants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3700 Billion |

| Market Size in 2026 | USD 3944.2 Billion |

| Market Size in 2031 | USD 5429.31 Billion |

| CAGR | 6.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fresh vegetables continue to dominate the global fresh food market, accounting for approximately 34% of the total market share in 2025. This dominance is primarily driven by their daily consumption across households, foodservice establishments, and institutional catering. Vegetables form the backbone of global dietary patterns, particularly in emerging economies where plant-based diets remain the primary source of nutrition. The increasing awareness of preventive healthcare, coupled with rising incidences of lifestyle-related diseases such as obesity, diabetes, and cardiovascular disorders, has significantly strengthened the demand for nutrient-rich vegetables.The growth of this segment is further reinforced by shifting consumer preferences toward functional foods that provide health benefits beyond basic nutrition. Leafy greens such as spinach, kale, lettuce, and cabbage are witnessing accelerated demand due to their high vitamin and mineral content. In addition, the expansion of urban populations and changing food habits are encouraging higher consumption of pre-cut, pre-washed, and ready-to-cook vegetable formats, which offer convenience and time savings for working consumers. Technological advancements in cold chain logistics and improved post-harvest handling practices have also contributed to reducing spoilage and increasing shelf life, thereby enhancing market penetration of fresh vegetables across long-distance supply chains.Another key driver supporting the growth of fresh vegetables is the global shift toward plant-based diets and vegan lifestyles. This trend is particularly strong in North America and Europe, where consumers are actively reducing meat consumption and replacing it with vegetable-based meals. Furthermore, government initiatives promoting healthy eating habits, school nutrition programs, and subsidies for vegetable cultivation are strengthening the supply side, ensuring consistent availability and affordability across markets. As a result, fresh vegetables are expected to maintain their leading position in the global fresh food landscape over the forecast period.

Farming Type Insights

Conventional farming remains the dominant production method in the global fresh food market, accounting for approximately 68% of total market share in 2025. Its dominance is primarily attributed to its ability to deliver high crop yields at relatively lower production costs compared to organic and alternative farming methods. Conventional agriculture benefits from the widespread use of synthetic fertilizers, pesticides, and mechanized farming techniques, which collectively enhance productivity and ensure consistent supply to meet growing global demand.The key growth driver for conventional farming is its scalability, particularly in developing economies where food security remains a priority. Countries in Asia-Pacific, Latin America, and parts of Africa rely heavily on conventional methods to support large populations and expanding urban centers. The economic efficiency of this farming type allows farmers to produce large volumes of crops within short growing cycles, making it essential for meeting both domestic consumption and export requirements.Additionally, advancements in agricultural technology, including genetically improved seed varieties, precision irrigation systems, and mechanized harvesting equipment, have significantly increased the efficiency of conventional farming practices. These innovations have helped reduce production risks associated with weather variability and pest infestations. However, despite its dominance, the segment faces increasing scrutiny due to environmental concerns such as soil degradation, water pollution, and chemical residue in food products. This has led to a gradual shift in consumer awareness, although cost competitiveness continues to sustain its leadership position globally.

Distribution Channel Insights

Supermarkets and hypermarkets represent the leading distribution channels in the global fresh food market, accounting for approximately 42% of total sales. Their dominance is driven by the convenience of one-stop shopping experiences, wide product assortments, and standardized quality control systems. These retail formats provide consumers with access to a diverse range of fresh vegetables, fruits, dairy, and packaged fresh products under controlled storage conditions, ensuring product freshness and safety.The growth of this segment is strongly supported by rapid urbanization and the expansion of organized retail infrastructure, particularly in developing economies. Rising disposable incomes and changing consumer lifestyles have encouraged a shift away from traditional wet markets toward modern retail environments that offer hygiene, transparency, and better product presentation. Additionally, supermarkets and hypermarkets invest heavily in cold chain logistics and inventory management systems, which help minimize wastage and maintain consistent supply.At the same time, online retail channels are emerging as the fastest-growing distribution segment. The increasing penetration of smartphones, digital payment systems, and e-commerce platforms has transformed the way consumers purchase fresh food products. Online grocery delivery services offer convenience, doorstep delivery, and time savings, making them particularly attractive to urban working populations. The integration of artificial intelligence and predictive analytics in supply chain management is further improving delivery efficiency and reducing spoilage rates, thereby strengthening the role of digital platforms in the fresh food ecosystem.

Supply Chain Insights

Domestic supply chains dominate the global fresh food market, accounting for nearly 60% of total supply. This preference is largely driven by the highly perishable nature of fresh food products, which require rapid transportation and minimal handling time to preserve quality and nutritional value. Local sourcing ensures reduced transit time, lower transportation costs, and improved freshness at the point of consumption.The growth of domestic supply chains is strongly supported by the expansion of regional agricultural production hubs and the development of efficient logistics infrastructure. Many countries are investing in farm-to-market connectivity, cold storage facilities, and distribution networks to strengthen local supply resilience. This is particularly important in regions with high population density, where demand for fresh food is consistently strong and supply chain efficiency is critical.International supply chains, although smaller in share, play a crucial role in meeting demand for off-season produce and exotic fruits and vegetables. Global trade agreements, improved air freight systems, and advanced packaging technologies have facilitated cross-border movement of fresh food products. However, challenges such as trade restrictions, tariffs, and logistical complexities continue to limit the expansion of global supply networks compared to domestic systems.

Packaging Insights

Loose and unpackaged fresh food accounts for approximately 55% of the global market, particularly in developing regions where traditional retail systems such as open markets and local vendors remain prevalent. This format is widely preferred due to its affordability, minimal processing requirements, and direct farm-to-consumer distribution model. Consumers in these regions often prioritize cost over packaging convenience, sustaining the dominance of loose fresh food products.However, packaged fresh food is gaining significant traction, especially in urban areas across developed and emerging economies. Rising concerns regarding hygiene, food safety, and contamination are encouraging consumers to shift toward pre-packaged and sealed products. Packaged fresh food also offers advantages such as extended shelf life, portion control, and improved traceability, which are increasingly valued in modern retail environments.Innovation in sustainable packaging materials, including biodegradable films and recyclable containers, is further driving growth in this segment. Retailers and manufacturers are adopting eco-friendly packaging solutions in response to environmental regulations and increasing consumer demand for sustainable products. As urbanization continues to expand, the packaged segment is expected to witness accelerated growth in the coming years.

End-Use Insights

Household consumption remains the dominant end-use segment in the global fresh food market, driven by daily dietary requirements and home-based meal preparation. Fresh food products are an essential component of household nutrition, and their consumption is closely linked to population growth, income levels, and cultural dietary preferences. Increasing health awareness among consumers is further encouraging the inclusion of fresh fruits and vegetables in daily diets.The foodservice industry, however, is emerging as the fastest-growing end-use segment. The rapid expansion of restaurants, hotels, quick-service outlets, and institutional catering services is significantly increasing demand for fresh ingredients. Urbanization and changing lifestyles have led to a rise in out-of-home dining, boosting procurement of fresh food products by commercial establishments. The global foodservice sector is expanding at a CAGR of over 7%, creating substantial opportunities for suppliers across the fresh food value chain.Additionally, the growing popularity of meal kits and ready-to-cook solutions is reshaping consumption patterns. These products cater to busy urban consumers seeking convenience without compromising on nutrition. As a result, fresh food suppliers are increasingly collaborating with foodservice operators and meal kit providers to ensure consistent and high-quality supply.

Explore more data points, trends and opportunities Download Free Sample Report

Fresh Food Market Segmentations

By Product Type

- Fresh Fruits

- Fresh Vegetables

- Fresh Meat & Poultry

- Fresh Seafood

- Fresh Dairy Products

- Fresh Herbs & Microgreens

By Farming Type

- Conventional Farming

- Organic Farming

- Hydroponic/Controlled Environment Agriculture

- Regenerative Agriculture

By Distribution Channel

- Supermarkets & Hypermarkets

- Traditional Grocery Stores/Wet Markets

- Convenience Stores

- Online Retail/E-commerce

- Direct-to-Consumer Channels

By Supply Chain Type

- Domestic Supply

- Imported Supply

- Local/Short Supply Chain

By Packaging Type

- Loose/Unpackaged

- Pre-packaged Fresh Produce

- Modified Atmosphere Packaging

- Vacuum Packaging

Regional Insights

Asia-Pacific

Asia-Pacific leads the global fresh food market, accounting for approximately 38% of total market share in 2025. The region’s dominance is primarily driven by its large population base, strong agricultural production capacity, and rapidly increasing urbanization. China plays a central role in both production and consumption, supported by extensive farmland and advanced distribution networks. India is also witnessing strong growth due to rising disposable incomes, changing dietary patterns, and government initiatives supporting agricultural modernization.The key growth drivers in Asia-Pacific include expanding middle-class populations, increasing awareness of nutritional health, and rising demand for diversified food products. Additionally, technological advancements in farming practices and improved supply chain infrastructure are enhancing productivity and reducing wastage. The growing penetration of organized retail and e-commerce platforms is further transforming food distribution systems across the region.

North America

North America holds approximately 22% of the global market share, with the United States being the primary contributor. The region is characterized by high consumer awareness regarding health and nutrition, leading to strong demand for organic and premium fresh food products. Advanced cold chain logistics, efficient supply networks, and highly organized retail systems support market stability and growth.The key growth drivers include increasing adoption of healthy eating habits, rising demand for organic produce, and strong purchasing power among consumers. Additionally, technological innovations in agriculture, such as precision farming and vertical farming, are enhancing domestic production capabilities. The region also benefits from a well-established import network that ensures year-round availability of diverse fresh food products.

Europe

Europe accounts for nearly 20% of the global market, driven by strong consumer demand for sustainable, organic, and high-quality food products. Countries such as Germany, France, and the United Kingdom are leading contributors to regional consumption. Strict food safety regulations and sustainability initiatives play a crucial role in shaping market dynamics.The primary growth drivers include increasing preference for organic farming, government support for sustainable agriculture, and rising awareness of environmental impact. European consumers are highly conscious of food origin and production methods, which has led to increased demand for traceable and ethically produced fresh food. The region also benefits from well-developed retail infrastructure and strong supply chain integration.

Latin America

Latin America plays a significant role as a global exporter of fresh fruits and vegetables, with countries such as Brazil and Mexico leading production. The region benefits from favorable climatic conditions, fertile soil, and abundant agricultural resources. These natural advantages support large-scale cultivation and export-oriented farming systems.The key growth drivers include increasing global demand for tropical fruits, expansion of export markets, and foreign investment in agricultural infrastructure. Additionally, improvements in logistics and trade agreements are strengthening the region’s position in the global supply chain. Domestic consumption is also rising due to improving economic conditions and urbanization.

Middle East & Africa

The Middle East & Africa region is the fastest-growing market, with a projected CAGR exceeding 7.5%. Limited arable land and harsh climatic conditions have resulted in high dependency on imported fresh food products, particularly in Gulf countries such as the UAE and Saudi Arabia. This import reliance is a major driver of market growth.Key growth drivers include rising population growth, increasing urbanization, and expanding hospitality and tourism industries. Governments in the region are also investing in agricultural innovation, including hydroponics and vertical farming, to improve domestic production capabilities. Additionally, the growing retail sector and expansion of cold chain infrastructure are enhancing market accessibility and product availability.

Key Players in the Fresh Food Market

- Dole plc

- Fresh Del Monte Produce Inc.

- Chiquita Brands International

- Tyson Foods Inc.

- JBS S.A.

- Cargill Incorporated

- Sysco Corporation

- Archer Daniels Midland Company

- WH Group Limited

- Nestlé S.A.

- Danone S.A.

- Hormel Foods Corporation

- Maruha Nichiro Corporation

- Mitsubishi Corporation (Food Division)

- Greenyard NV