Online Food and Grocery Delivery Market Size

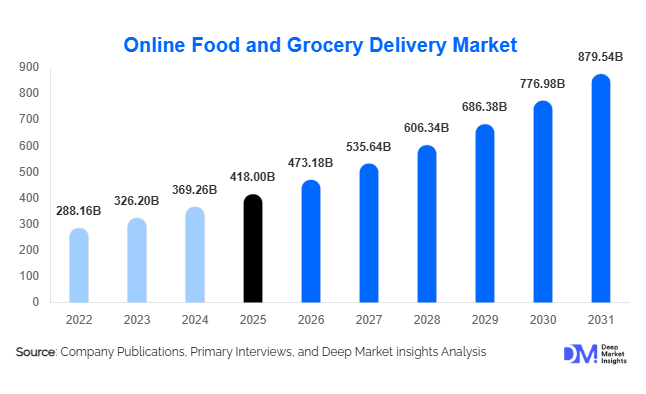

According to Deep Market Insights, the global online food and grocery delivery market size was valued at USD 418 billion in 2025 and is projected to grow from USD 473.18 billion in 2026 to reach USD 879.54 billion by 2031, expanding at a CAGR of 13.2% during the forecast period (2026–2031). The market growth is primarily driven by rapid digitalization of food retail, increasing consumer reliance on convenience-based purchasing, and the expansion of quick commerce models offering ultra-fast deliveries. Rising smartphone penetration, widespread adoption of digital payment systems, and advancements in last-mile logistics infrastructure are transforming food consumption and grocery purchasing behaviors globally.

Key Market Insights

- Quick commerce is redefining delivery expectations, with 10–30 minute fulfillment becoming a competitive benchmark in urban markets.

- Mobile applications dominate ordering behavior, accounting for the majority of global transactions through personalized recommendations and loyalty ecosystems.

- Asia-Pacific leads global demand due to dense urban populations, digital payment adoption, and expanding middle-class consumption.

- Subscription-based delivery models are gaining traction, helping platforms improve customer retention and operational profitability.

- Online grocery delivery is growing faster than restaurant delivery, supported by dark-store infrastructure and recurring household demand.

- AI-driven logistics and automation technologies are enhancing delivery efficiency, route optimization, and inventory forecasting.

What are the latest trends in the online food and grocery delivery market?

Rapid Expansion of Quick Commerce Ecosystems

Quick commerce has emerged as the most disruptive trend within the online delivery industry. Companies are investing heavily in hyperlocal fulfillment centers and dark stores positioned near high-density residential areas to enable deliveries within minutes. Consumers increasingly expect instant access to groceries, snacks, and ready-to-eat meals, shifting demand away from traditional weekly shopping toward frequent smaller purchases. Platforms are optimizing inventory through predictive analytics to ensure high-demand products remain available while minimizing waste. This operational shift is improving order frequency and strengthening customer loyalty, particularly among urban millennials and dual-income households.

AI-Powered Personalization and Automation

Technology integration is reshaping both customer experience and operational efficiency. Artificial intelligence tools analyze purchasing patterns to recommend products, optimize pricing, and forecast demand. Automated picking systems in warehouses and robotics-assisted fulfillment centers are reducing operational costs while improving accuracy. Delivery platforms are also deploying machine learning algorithms to optimize routes, reduce fuel consumption, and shorten delivery times. These innovations are enabling companies to transition from growth-focused expansion toward sustainable profitability models.

What are the key drivers in the online food and grocery delivery market?

Urban Lifestyle Transformation and Convenience Demand

Increasing urbanization and evolving work lifestyles are significantly influencing food consumption patterns. Consumers are prioritizing convenience, time savings, and flexibility, leading to higher reliance on delivery platforms for daily meals and groceries. Busy professionals and dual-income households increasingly substitute physical store visits with app-based ordering, driving sustained demand growth. The expansion of cloud kitchens further supports this trend by creating delivery-first restaurant ecosystems.

Expansion of Digital Payment Infrastructure

The rapid adoption of digital wallets, real-time payment systems, and mobile banking has removed transactional friction across emerging and developed markets. Seamless checkout experiences encourage impulse purchasing and subscription adoption. Countries with strong digital payment ecosystems are witnessing higher order frequency and increased customer retention rates, accelerating overall market growth.

What are the restraints for the global market?

High Operational and Delivery Costs

Despite strong revenue growth, profitability remains a key challenge due to high last-mile logistics expenses, driver incentives, and promotional discounts. Maintaining rapid delivery speeds requires significant investment in infrastructure and workforce management, limiting margin expansion. Companies are increasingly focusing on subscription programs and private-label grocery offerings to offset operational costs.

Regulatory and Labor Compliance Challenges

Government regulations surrounding gig workers, wage protections, and employment classification are increasing operational complexity. Compliance requirements related to data privacy and consumer protection also require continuous investment in cybersecurity and platform governance. These regulatory pressures may slow expansion in certain regions while encouraging consolidation among larger players.

What are the key opportunities in the online food and grocery delivery industry?

Enterprise and Institutional Delivery Solutions

Beyond individual consumers, corporate offices, hospitals, universities, and co-living spaces are increasingly adopting digital meal and grocery procurement solutions. Subscription meal plans and bulk ordering platforms provide stable revenue streams and reduce reliance on promotional consumer demand. Enterprise integration also improves order predictability and operational efficiency for delivery providers.

Technology-Driven Logistics Innovation

Investments in AI analytics, autonomous delivery pilots, and electric vehicle fleets present significant growth opportunities. Companies leveraging predictive analytics can improve demand planning and reduce delivery costs. Drone and robotic delivery trials are expected to enhance efficiency in high-density urban areas over the long term, potentially transforming last-mile economics.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 418 Billion |

| Market Size in 2026 | USD 473.18 Billion |

| Market Size in 2031 | USD 879.54 Billion |

| CAGR | 13.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Service Type Insights

Restaurant food delivery continues to dominate the global online food delivery market, accounting for nearly 48% of total revenue. This dominance is fueled by the high frequency of consumer orders, increasing preference for convenience, and widespread adoption of delivery-first dining models, particularly in urban and suburban areas. Online grocery delivery has emerged as the fastest-growing category, driven by recurring household consumption patterns, rapid expansion of quick commerce networks, and the increasing demand for contactless shopping experiences. Meal kit delivery services are attracting health-conscious and time-sensitive consumers, offering a combination of convenience, portion control, and nutritional balance, which aligns with rising wellness trends. Specialty food delivery, encompassing organic meals, plant-based options, and premium ready-to-eat offerings, is expanding rapidly as consumers increasingly prioritize personalized, sustainable, and high-quality dining experiences. This growth is further supported by the proliferation of mobile ordering apps and AI-driven recommendation systems that enhance the user experience and encourage repeat orders.

Business Model Insights

Hybrid business models are leading the industry, integrating marketplace scalability with inventory-led fulfillment through strategically located dark stores and localized warehouses. This approach allows platforms to maintain control over delivery speed, product availability, and profit margins while scaling operations efficiently. Marketplace-only models remain prevalent in emerging markets, where low capital expenditure and flexible vendor partnerships make them attractive. Subscription-based ecosystems are gaining traction globally, enabling platforms to drive customer loyalty, ensure predictable recurring revenue, and offer value-added benefits such as free deliveries and exclusive discounts. The convergence of these business models is also fostering innovation in AI-powered logistics, predictive inventory management, and dynamic pricing strategies, which collectively enhance operational efficiency and customer satisfaction.

Delivery Speed Insights

Instant delivery services, typically within 30 minutes, are among the fastest-growing segments globally, largely driven by dense urban populations, smartphone penetration, and evolving consumer expectations for immediacy. Same-day delivery remains critical for grocery and bulk orders, catering to households that require larger baskets and prefer planned replenishment. Scheduled deliveries appeal to families and corporate clients seeking predictability in meal planning. Platforms are increasingly differentiating themselves based on delivery reliability, transparency, and speed rather than price alone, leveraging route optimization algorithms, AI-powered demand forecasting, and partnerships with last-mile logistics providers.

Payment Mode Insights

Digital wallets and real-time payment systems dominate global transactions, reflecting a shift toward cashless and seamless online experiences. Card payments remain widely used in developed markets, while cash-on-delivery continues to be relevant in select emerging economies where digital penetration is lower. Subscription billing models are expanding steadily as platforms introduce membership programs, offering perks like free delivery, loyalty points, and exclusive discounts, which not only improve retention but also enhance revenue predictability. Additionally, integration with BNPL (Buy Now, Pay Later) options and cross-platform wallet ecosystems is further facilitating adoption in price-sensitive regions.

End-Use Insights

Individual consumers constitute the largest end-use segment, accounting for approximately three-fourths of global orders, driven by convenience, time-saving benefits, and diverse food options. Corporate and institutional buyers are emerging as high-growth segments, particularly in urban business districts and technology parks where scheduled meal deliveries are increasingly offered as workplace perks. Hospitality businesses and small restaurants are also leveraging online grocery and specialty food platforms for ingredient sourcing, reducing inventory risks, improving supply chain efficiency, and ensuring consistent quality for their offerings. Additionally, collaborations between platforms and local producers are creating new avenues for small-scale suppliers to reach wider audiences.

Explore more data points, trends and opportunities Download Free Sample Report

Online Food and Grocery Delivery Market Segmentations

By Service Type

- Restaurant Food Delivery

- Online Grocery Delivery

- Meal Kit Delivery Services

- Specialty & Ready-to-Eat Food Delivery

By Business Model

- Marketplace-Based Platforms

- Inventory-Led (Dark Store) Model

- Hybrid Model

- Subscription-Based Delivery Services

By Delivery Speed

- Instant Delivery

- Same-Day Delivery

- Scheduled Delivery

- Next-Day Delivery

By End User

- Individual Consumers

- Corporate & Institutional Buyers

- Hospitality & Foodservice Businesses

- Small Retail & Cloud Kitchens

By Platform Type

- Mobile Application-Based Platforms

- Website-Based Ordering Platforms

- Voice-Assisted & Smart Device Ordering

Regional Insights

North America

North America accounts for approximately 26% of the global online food delivery market, with the United States and Canada leading adoption. Growth is driven by high consumer spending power, strong acceptance of subscription-based delivery models, and highly developed logistics and urban infrastructure. Suburban households are increasingly adopting grocery delivery services for convenience and time savings, while metropolitan areas show high demand for instant delivery and specialty cuisine offerings. Innovation in autonomous delivery technologies, electric vehicle fleets, and app-based order management systems is further accelerating regional market expansion. Additionally, the rise of sustainability-conscious consumers is prompting companies to adopt eco-friendly packaging and carbon-neutral delivery options.

Europe

Europe contributes around 21% of global demand, with the United Kingdom, Germany, and France as key growth markets. Regional expansion is driven by strong consumer preference for premium and ethically sourced foods, the proliferation of mobile-first ordering, and government-backed sustainability initiatives encouraging electric fleets and eco-conscious packaging. Urbanization, high smartphone penetration, and a mature e-commerce ecosystem are fueling the adoption of instant and same-day delivery services. Subscription models and loyalty programs are widely embraced to secure repeat customers, while technological innovations in route optimization and AI-driven logistics further enhance delivery efficiency and reliability across the region.

Asia-Pacific

Asia-Pacific dominates the market with nearly 39% share, led by China and India. Rapid urbanization, a growing middle class, and mobile-first consumer behavior are key drivers of regional growth. In India, rising disposable incomes, expanding quick commerce networks, and increased smartphone penetration have accelerated adoption, making it one of the fastest-growing markets globally. China continues to benefit from advanced logistics infrastructure, widespread adoption of digital payment systems, and integration of online food delivery with social media and super-app ecosystems. Southeast Asian countries are experiencing robust growth, supported by improving last-mile delivery networks, rising urban populations, and consumer trends favoring convenience, instant gratification, and premium food offerings.

Latin America

Latin America accounts for roughly 9% of global market share, with Brazil and Mexico as key contributors. Growth in the region is driven by increasing digital banking adoption, rising urbanization, and expansion of smartphone penetration, which facilitate higher consumer engagement with online food delivery platforms. Market players are investing heavily in localized delivery networks and micro-fulfillment centers to overcome infrastructure and traffic challenges while ensuring timely and reliable service. Rising demand for premium and specialty foods, combined with promotional and loyalty programs, is also supporting adoption across both individual and corporate consumer segments.

Middle East & Africa

The Middle East and Africa region is witnessing rapid growth, particularly in the UAE and Saudi Arabia. Factors driving expansion include high smartphone penetration, strong urban concentration, rising disposable income, and premium food consumption patterns. Platforms are capitalizing on quick commerce models and subscription services to meet growing consumer expectations for speed and convenience. Government support for digital infrastructure and investments in logistics hubs are enhancing service efficiency, while intra-regional adoption is expanding as consumers increasingly prefer online ordering for both individual and corporate needs. Additionally, the increasing popularity of healthy, organic, and specialty food options is influencing menu offerings and platform growth strategies.

Key Players in the Online Food and Grocery Delivery Market

- Uber Technologies Inc.

- DoorDash Inc.

- Meituan

- Delivery Hero SE

- Just Eat Takeaway.com

- Prosus NV

- Amazon.com Inc.

- Walmart Inc.

- Alibaba Group Holding Ltd.

- JD.com Inc.

- Zomato Ltd.

- Swiggy Ltd.

- Coupang Inc.

- Instacart (Maplebear Inc.)

- HelloFresh SE