Coffee Retail Market Size

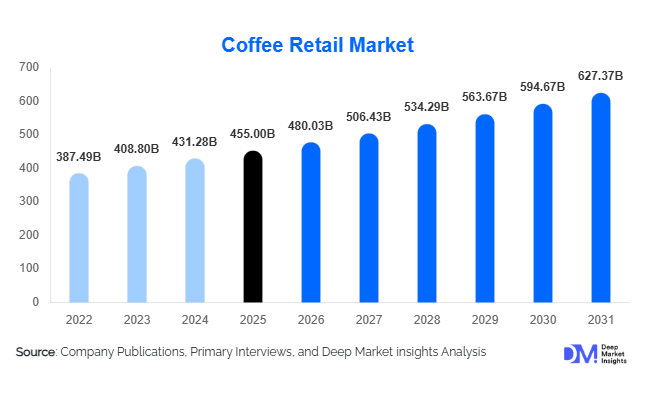

According to Deep Market Insights, the global coffee retail market size was valued at USD 455,000 million in 2025 and is projected to grow from USD 480.03 million in 2026 to reach USD 627.37 million by 2031, expanding at a CAGR of 5.5% during the forecast period (2026–2031). The coffee retail market growth is primarily driven by rising global coffee consumption, increasing demand for premium and specialty coffee, and the rapid expansion of café culture and convenience-based consumption formats such as ready-to-drink beverages and capsules.

Key Market Insights

- Premium and specialty coffee consumption is accelerating globally, driven by consumer preference for high-quality, ethically sourced, and artisanal products.

- Ready-to-drink (RTD) coffee and capsule formats are witnessing rapid growth, supported by convenience-oriented lifestyles and urbanization.

- Europe dominates the global market, supported by high per capita consumption and established coffee traditions.

- Asia-Pacific is the fastest-growing region, fueled by increasing coffee adoption in countries such as China and India.

- Digital retail and e-commerce channels are transforming distribution, enabling direct-to-consumer engagement and subscription-based coffee services.

- Sustainability and traceability are becoming critical differentiators, influencing consumer purchasing decisions and brand positioning.

What are the latest trends in the coffee retail market?

Premiumization and Specialty Coffee Expansion

The coffee retail market is increasingly shifting toward premium and specialty offerings, with consumers prioritizing quality, origin, and unique flavor profiles. Single-origin coffee, organic certifications, and artisanal roasting techniques are gaining traction, particularly in urban markets. This trend is enabling brands to command higher price points and build strong customer loyalty. Retailers are also focusing on storytelling and transparency, highlighting sourcing practices and farmer relationships to enhance brand value. Specialty cafés and micro-roasters are playing a significant role in shaping consumer preferences, contributing to the premiumization wave.

Growth of Convenience-Oriented Formats

Convenience has become a key driver in the coffee retail market, leading to rapid adoption of ready-to-drink coffee, instant mixes, and single-serve capsules. These formats cater to busy consumers seeking quick and consistent coffee experiences. Technological advancements in packaging and preservation have improved product quality and shelf life, making RTD coffee a mainstream option. Additionally, innovations such as cold brew cans, functional coffee beverages, and flavored variants are expanding product diversity and attracting younger consumers.

What are the key drivers in the coffee retail market?

Rising Café Culture and Out-of-Home Consumption

The expansion of café culture worldwide is significantly driving coffee retail growth. Branded coffee chains and independent cafés are not only boosting out-of-home consumption but also influencing at-home purchasing behavior. Consumers increasingly seek café-quality coffee experiences at home, leading to higher demand for premium retail products. The proliferation of coffee chains in emerging markets is further strengthening this trend.

Increasing Disposable Income and Urbanization

Rising disposable incomes, particularly in emerging economies, are enabling consumers to spend more on premium beverages. Urbanization is also contributing to lifestyle changes that favor coffee consumption, especially among younger demographics. As a result, the coffee retail market is witnessing strong growth in both volume and value terms across developing regions.

What are the restraints for the global market?

Volatility in Raw Coffee Prices

Fluctuations in coffee bean prices due to climate change, supply disruptions, and geopolitical factors pose a significant challenge for market participants. These variations impact production costs and profit margins, particularly for mid-range and economy segments.

Market Saturation in Developed Regions

Highly mature markets such as North America and Europe are experiencing intense competition and saturation. The presence of numerous established brands makes it difficult for new entrants to gain market share without significant investment in innovation and marketing.

What are the key opportunities in the coffee retail industry?

Expansion in Emerging Markets

Emerging economies in Asia-Pacific and Africa present significant growth opportunities due to rising coffee adoption and expanding middle-class populations. Countries such as India and China are witnessing a cultural shift toward coffee consumption, creating new avenues for market expansion. Companies investing in localized products and pricing strategies can capture substantial market share in these regions.

Digital Transformation and E-commerce Growth

The rise of e-commerce platforms and direct-to-consumer models is transforming the coffee retail landscape. Subscription services, personalized recommendations, and online-exclusive products are enhancing customer engagement and driving sales. Digital channels also enable brands to expand their reach without heavy investment in physical retail infrastructure.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 455.00 Billion |

| Market Size in 2026 | USD 480.03 Billion |

| Market Size in 2031 | USD 627.37 Billion |

| CAGR | 5.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global coffee market is segmented by product type into ground coffee, whole bean coffee, instant coffee, ready-to-drink (RTD) coffee, and coffee pods and capsules. Among these, ground coffee continues to dominate the market, accounting for approximately 32% of the global market share in 2025. The leadership of this segment is primarily driven by its ability to strike an optimal balance between convenience, affordability, and flavor quality. Consumers prefer ground coffee for its ease of use while still retaining a relatively rich and authentic taste profile compared to instant variants. Additionally, the widespread availability of ground coffee across retail channels, including supermarkets, hypermarkets, and online platforms, further strengthens its dominance.Instant coffee continues to maintain strong demand, particularly in emerging markets across Asia-Pacific, Latin America, and parts of Africa. Its affordability, long shelf life, and minimal preparation requirements make it highly attractive for consumers in price-sensitive regions. The segment is also witnessing innovation in terms of improved flavor profiles and premium instant coffee offerings, which are helping to shift consumer perception and expand its reach beyond traditional markets.Ready-to-drink (RTD) coffee and coffee pods and capsules represent the fastest-growing product segments within the global coffee market. The growth of RTD coffee is fueled by increasing demand for on-the-go beverage options, especially among younger consumers and urban populations. The availability of diverse flavors, functional ingredients such as protein and vitamins, and attractive packaging formats is further driving adoption. Similarly, the pods and capsules segment is experiencing rapid expansion due to its unparalleled convenience, consistency, and compatibility with modern coffee machines. The increasing adoption of single-serve coffee systems in households and workplaces is a key driver for this segment, alongside continuous product innovation by leading brands.

Application (End-Use Channel) Insights

Based on application, the global coffee market is segmented into household consumption, foodservice and HoReCa (Hotels, Restaurants, and Cafés), and workplace consumption. Among these, household consumption represents the largest segment, contributing nearly 50% of the total market share. The dominance of this segment is primarily attributed to the growing trend of at-home coffee consumption, which has been significantly reinforced by lifestyle changes and remote working arrangements. Consumers are increasingly investing in home brewing equipment and experimenting with different coffee types, thereby boosting demand across product categories.The foodservice and HoReCa segment is the fastest-growing application segment, driven by the global expansion of café chains, quick-service restaurants, and premium coffee outlets. Urbanization, rising disposable incomes, and changing consumer lifestyles are encouraging out-of-home coffee consumption, particularly among millennials and Gen Z consumers. The proliferation of international and regional café brands, along with the increasing popularity of experiential dining, is significantly boosting demand in this segment.Workplace consumption is also witnessing steady growth, as companies increasingly recognize the importance of providing high-quality coffee as a standard employee amenity. The presence of coffee machines and premium coffee offerings in offices is not only enhancing employee satisfaction but also contributing to productivity and workplace culture. As organizations continue to invest in employee well-being, the demand for coffee in workplace settings is expected to grow further.

Distribution Channel Insights

The coffee market is distributed through various channels, including supermarkets and hypermarkets, online retail, specialty stores, and others. Supermarkets and hypermarkets lead the distribution landscape, holding around 35% market share. The dominance of this channel is driven by its extensive reach, wide product assortment, and competitive pricing strategies. Consumers prefer these retail formats for their convenience, as they offer a one-stop shopping experience where multiple coffee brands and formats are readily available.The leading driver for this segment is the ability of large retail chains to provide promotional offers, discounts, and private-label products, which attract a broad consumer base. Additionally, the presence of in-store displays and sampling activities helps in influencing consumer purchasing decisions, further strengthening the position of supermarkets and hypermarkets.Online retail is emerging as the fastest-growing distribution channel, supported by the rapid digital transformation and increasing penetration of smartphones and internet connectivity. Consumers are increasingly turning to e-commerce platforms for their coffee purchases due to the convenience of home delivery, access to a wider range of products, and the availability of subscription services. The ability to compare prices, read reviews, and explore niche and specialty coffee brands online is significantly enhancing the appeal of this channel.Specialty coffee stores continue to thrive, particularly in the premium and artisanal segments. These stores offer curated selections of high-quality coffee products, often focusing on single-origin beans, organic options, and unique blends. The personalized shopping experience and expert guidance provided in specialty stores play a crucial role in attracting discerning consumers who are willing to pay a premium for superior quality.

Price Tier Insights

The global coffee market is segmented into economy, mid-range, premium, and ultra-premium price tiers. Among these, the mid-range segment dominates with approximately 40% market share, catering to a broad consumer base that seeks a balance between quality and affordability. The leading driver for this segment is the growing middle-class population worldwide, particularly in emerging economies, which is increasingly willing to spend on better-quality coffee without significantly impacting their budgets.The mid-range segment benefits from strong brand presence, consistent quality, and wide availability across distribution channels. Manufacturers are focusing on offering value-for-money products within this segment, incorporating improved flavor profiles and sustainable sourcing practices to attract a larger audience.Premium and ultra-premium segments are experiencing rapid growth, driven by the rising demand for specialty coffee, single-origin beans, and ethically sourced products. Consumers in developed markets, as well as affluent urban populations in emerging economies, are increasingly prioritizing quality, sustainability, and unique taste experiences over price. This shift in consumer behavior is encouraging brands to expand their premium product portfolios and invest in storytelling, branding, and traceability.Economy products continue to maintain strong demand in price-sensitive markets, particularly in regions where affordability remains a key purchasing factor. These products are widely consumed in developing countries and rural areas, where consumers prioritize cost-effectiveness and accessibility.

Packaging Format Insights

In terms of packaging format, the coffee market includes flexible bags, bottles, cans, pods, capsules, and others. Flexible bags dominate the market, accounting for nearly 45% of the total share, primarily due to their cost efficiency, lightweight nature, and widespread use across different coffee types. The leading driver for this segment is the ability of flexible packaging to preserve freshness while offering convenience in storage and transportation. Additionally, advancements in packaging technology, such as resealable zippers and vacuum sealing, are further enhancing product shelf life and consumer convenience.Bottles and cans are gaining significant popularity, particularly in the RTD coffee segment. The growth of this packaging format is driven by the increasing demand for portable and ready-to-consume beverages. Attractive designs, branding opportunities, and the ability to incorporate functional ingredients make bottles and cans an appealing choice for both manufacturers and consumers.Pods and capsules are experiencing rapid growth, supported by the rising adoption of single-serve coffee machines in households and offices. The convenience, consistency, and minimal preparation time associated with these formats are key factors driving their popularity. Additionally, ongoing innovation in biodegradable and recyclable capsules is addressing environmental concerns, further supporting segment expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Coffee Retail Market Segmentations

By Product Type

- Whole Bean Coffee

- Ground Coffee

- Instant Coffee

- Ready-to-Drink Coffee

- Coffee Pods & Capsules

By Coffee Type

- Arabica Coffee

- Robusta Coffee

- Blended Coffee

- Specialty Coffee

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Coffee Stores

- Online Retail

- Vending & Automated Retail

By Price Tier

- Economy

- Mid-Range

- Premium

- Ultra-Premium

By End-Use Channel

- Household

- Foodservice & HoReCa

- Workplace & Institutional

Regional Insights

North America

North America holds approximately 28% of the global coffee market share, with the United States being the primary contributor. The region's growth is driven by high per capita coffee consumption, a well-established café culture, and a strong preference for premium and specialty coffee products. Consumers in North America are increasingly seeking high-quality, ethically sourced coffee, which is driving demand for organic, fair-trade, and single-origin products.Another key growth driver in the region is the rapid expansion of specialty coffee chains and independent cafés, which are introducing innovative beverages and enhancing consumer experiences. The widespread adoption of advanced coffee machines in households and workplaces is also contributing to increased consumption. In Canada, the market is supported by growing interest in sustainable and health-conscious products, as well as the rising popularity of plant-based and functional coffee beverages.

Europe

Europe accounts for around 30% of the global market share, making it the largest regional market for coffee. The region's dominance is underpinned by deeply rooted coffee traditions, high consumption levels, and a strong preference for quality and authenticity. Countries such as Germany, Italy, and France are key contributors, with well-established coffee cultures and high per capita intake.The growth of the European market is driven by increasing demand for premium and sustainable coffee products. Consumers are becoming more conscious of environmental and social factors, leading to a rise in demand for ethically sourced and eco-friendly coffee. Additionally, the popularity of specialty coffee shops and artisanal roasting techniques is further enhancing market growth. The presence of stringent quality standards and certifications also ensures high product quality, which attracts discerning consumers.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the global coffee market, with a CAGR exceeding 7%. The region's growth is primarily driven by rapid urbanization, rising disposable incomes, and changing consumer preferences. Emerging markets such as China and India are witnessing a significant shift from traditional tea consumption to coffee, particularly among younger demographics.The expansion of international coffee chains, increasing influence of Western lifestyles, and growing café culture are key drivers in the region. Additionally, the proliferation of e-commerce platforms and digital payment systems is facilitating easier access to a wide range of coffee products. In mature markets like Japan and South Korea, innovation in product offerings, including RTD coffee and functional beverages, is sustaining growth.

Latin America

Latin America plays a unique dual role as both a major coffee producer and a growing consumer market. Brazil leads the region in both production and domestic consumption, while Mexico is emerging as a significant retail market. The region's growth is supported by increasing urbanization, rising middle-class populations, and expanding retail infrastructure.Another important driver is the growing appreciation for locally produced coffee, which is boosting domestic consumption. Governments and industry players are also investing in improving coffee quality and promoting exports, which indirectly supports market growth. The expansion of café culture in urban centers is further contributing to increased coffee consumption across the region.

Middle East & Africa

The Middle East and Africa region is witnessing steady growth in the coffee market, driven by expanding café culture, urbanization, and increasing consumer awareness. Countries such as the UAE and Saudi Arabia are experiencing rapid growth due to the proliferation of international coffee chains and premium café concepts.In Africa, South Africa stands out as a key market, supported by rising disposable incomes and growing interest in coffee consumption. The region's growth is also influenced by cultural shifts, increasing exposure to global trends, and the development of modern retail channels. Additionally, the presence of coffee-producing countries within Africa is fostering greater awareness and appreciation of coffee, further supporting market expansion.

Key Players in the Coffee Retail Market

- Nestlé S.A.

- Starbucks Corporation

- JDE Peet’s N.V.

- The Kraft Heinz Company

- Tata Consumer Products Limited

- Luigi Lavazza S.p.A.

- Keurig Dr Pepper Inc.

- Strauss Group Ltd.

- Tchibo GmbH

- Dunkin’ Brands Group, Inc.

- Illycaffè S.p.A.

- Melitta Group

- Costa Coffee

- Peet’s Coffee

- Café de Coral Holdings