Fashion Accessories Market Size

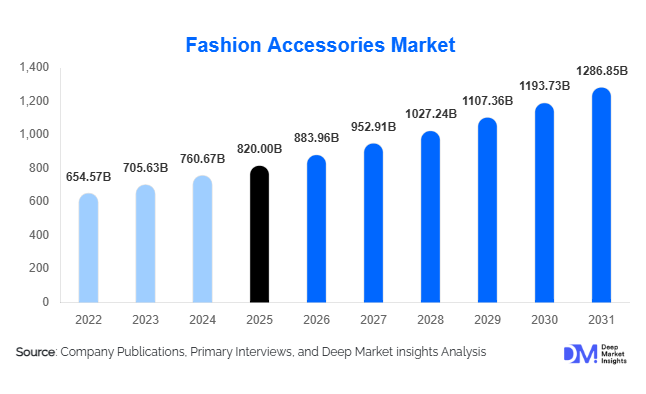

According to Deep Market Insights, the global fashion accessories market size was valued at USD 820.0 billion in 2025 and is projected to grow from USD 883.96 billion in 2026 to reach USD 1,286.85 billion by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The fashion accessories market is experiencing growth driven by increasing consumer expenditure on personal appearance, rising premiumization across fashion categories, growing adoption of online retail channels, and the rapid influence of social media on purchasing behavior. Fashion accessories have evolved from complementary apparel items into essential lifestyle and identity products, supporting strong demand across both luxury and mass-market segments.

Key Market Insights

- Jewelry remains the largest product category, accounting for approximately 46% of global fashion accessories revenue in 2025.

- Asia-Pacific dominates the global market, supported by strong demand from China, India, Japan, and Southeast Asia.

- Women represent the largest consumer segment, accounting for more than half of global accessory purchases.

- E-commerce continues to gain share, driven by omnichannel retail strategies, social commerce, and direct-to-consumer business models.

- Sustainable and ethically sourced accessories are witnessing accelerated adoption, particularly among Gen Z and millennial consumers.

- Smart accessories and wearable technologies are creating new growth opportunities across eyewear, jewelry, and lifestyle accessory categories.

What are the latest trends in the fashion accessories market?

Sustainable and Circular Fashion Accessories Becoming Mainstream

Sustainability has become one of the most influential trends shaping the fashion accessories market. Consumers increasingly prefer products manufactured using recycled materials, vegan leather, ethically sourced gemstones, and low-carbon production processes. Luxury and premium brands are investing heavily in circular business models that include resale programs, repair services, refurbishment initiatives, and sustainable packaging solutions. Companies are also enhancing supply chain transparency to comply with evolving environmental regulations and consumer expectations. The shift toward circular fashion is creating new revenue opportunities while helping brands strengthen customer loyalty and ESG performance.

Technology-Integrated Fashion Accessories Expanding Rapidly

The convergence of fashion and technology is creating entirely new product categories within the industry. Smart watches, connected jewelry, AI-enabled wearable accessories, and smart eyewear are increasingly being adopted by consumers seeking functionality alongside style. Advances in wearable sensors, health monitoring capabilities, augmented reality applications, and wireless connectivity are expanding the value proposition of fashion accessories. Technology integration is particularly attractive to younger consumers, who prioritize personalization, convenience, and digital connectivity when making purchasing decisions. As innovation continues, technology-enabled accessories are expected to become one of the fastest-growing segments of the market.

What are the key drivers in the fashion accessories market?

Growing Fashion Consciousness and Social Media Influence

Social media platforms including Instagram, TikTok, Pinterest, and YouTube have significantly transformed consumer purchasing behavior. Influencer marketing, celebrity endorsements, and user-generated content are accelerating fashion trend adoption and encouraging frequent accessory purchases. Accessories are highly visible products that allow consumers to express personal identity and keep pace with rapidly evolving fashion trends. As digital engagement continues to increase globally, social media will remain a major catalyst for fashion accessory demand.

Rising Disposable Income and Premiumization

Growing disposable incomes, particularly across emerging economies, are supporting increased spending on premium and luxury fashion accessories. Consumers are increasingly willing to invest in high-quality handbags, watches, jewelry, and eyewear that provide both functional and status value. The rise of aspirational purchasing behavior among middle-income consumers is expanding the addressable market for premium brands while driving higher average selling prices across multiple product categories.

What are the restraints for the global market?

Counterfeit Products and Brand Dilution

The widespread availability of counterfeit handbags, watches, jewelry, and luxury accessories remains a major challenge for industry participants. Counterfeit products erode brand value, reduce legitimate sales, and negatively impact consumer trust. The growth of online marketplaces has increased the complexity of monitoring unauthorized products and protecting intellectual property rights globally.

Volatility in Raw Material Costs

Fashion accessory manufacturers remain exposed to fluctuations in the prices of leather, precious metals, gemstones, textiles, and synthetic materials. Rising input costs can negatively impact profit margins, particularly among premium and luxury manufacturers that rely heavily on high-quality raw materials. Supply chain disruptions and geopolitical uncertainties continue to contribute to raw material pricing volatility.

What are the key opportunities in the fashion accessories industry?

Expansion of Smart and Connected Accessories

The growing adoption of wearable technologies presents significant opportunities for both established brands and new market entrants. Smart jewelry, connected eyewear, health-monitoring accessories, and AI-powered wearable products are creating new revenue streams with premium pricing potential. As consumers increasingly seek multifunctional products, technology integration is expected to generate substantial market growth over the coming years.

Emerging Market Premiumization

Rapid urbanization, rising middle-class populations, and increasing luxury consumption across India, Indonesia, Vietnam, Saudi Arabia, and the UAE are creating attractive growth opportunities. International brands are expanding regional footprints through localized product offerings, influencer partnerships, and digital-first retail strategies. Premiumization trends in these markets are expected to contribute significantly to future industry expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 820 Billion |

| Market Size in 2026 | USD 883.96 Billion |

| Market Size in 2031 | USD 1286.85 Billion |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Jewelry dominates the fashion accessories market, accounting for approximately 46% of global revenue in 2025. Demand is supported by fashion jewelry, bridal purchases, gifting occasions, and increasing interest in personalized products. Watches represent another significant category, benefiting from luxury consumption trends and the growing popularity of smart wearables. Handbags and purses continue to generate strong demand across both premium and mass-market segments, driven by evolving fashion trends and brand loyalty. Eyewear, belts, wallets, scarves, and hair accessories contribute additional market value, while technology-enabled accessories are emerging as a rapidly growing product category. The combination of aesthetics, functionality, and lifestyle positioning continues to support strong demand across all major product segments.

Consumer Group Insights

Women account for approximately 53% of global fashion accessories demand, making them the largest consumer segment. This dominance is supported by broader product availability, higher purchase frequency, and greater engagement with fashion trends. Men represent a rapidly growing segment, particularly within watches, luxury leather goods, and premium eyewear categories. The unisex segment continues to expand as brands increasingly adopt gender-neutral product designs. Children's accessories remain a niche category but are experiencing growth through branded and licensed products targeting younger consumers and family-oriented purchasing behavior.

Distribution Channel Insights

Specialty fashion stores account for nearly 39% of global distribution revenues, benefiting from curated product assortments and enhanced customer experiences. Brand-owned retail stores remain important for premium and luxury manufacturers seeking greater control over brand positioning and consumer engagement. Online retail is the fastest-growing distribution channel, driven by convenience, broader product selection, personalized recommendations, and social commerce integration. Direct-to-consumer models continue gaining popularity as brands seek to improve margins and strengthen customer relationships through proprietary digital platforms.

Material Insights

Leather remains the leading material category, accounting for approximately 28% of global market value. Leather-based handbags, wallets, belts, and travel accessories continue to enjoy strong consumer demand due to their durability and premium appeal. Precious metals and gemstones dominate the jewelry segment, while textiles, synthetic materials, and recycled materials are gaining market share as sustainability becomes increasingly important. Smart materials and electronic components are also emerging as significant contributors to innovation within wearable accessory categories.

Explore more data points, trends and opportunities Download Free Sample Report

Fashion Accessories Market Segmentations

By Product Type

- Jewelry

- Watches

- Handbags & Purses

- Wallets & Small Leather Goods

- Eyewear

- Belts

- Scarves & Wraps

- Hats & Caps

- Hair Accessories

- Gloves

- Travel & Lifestyle Accessories

- Tech-Integrated Fashion Accessories

By Consumer Group

- Women

- Men

- Children

- Unisex

By Price Range

- Luxury

- Premium

- Mid-Market

- Economy/Fast Fashion

By Material

- Precious Metals & Gemstones

- Leather

- Synthetic Leather

- Textiles & Fabrics

- Plastics & Polymers

- Sustainable/Recycled Materials

- Smart/Electronic Components

By Distribution Channel

- Brand-Owned Stores

- Specialty Fashion Stores

- Department Stores

- Hypermarkets & Supermarkets

- Online Retail

- Travel Retail/Duty-Free

- Direct-to-Consumer (DTC)

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 47% of the global fashion accessories market in 2026, making it the largest regional market worldwide. The region's dominance is primarily driven by its massive consumer base, rapidly expanding middle-class population, rising disposable incomes, and strong manufacturing capabilities. China remains the largest contributor to regional demand, supported by increasing luxury consumption, strong domestic fashion brands, and growing demand for premium handbags, jewelry, watches, and eyewear. China's position as the world's leading fashion accessories manufacturing hub also strengthens regional supply chain competitiveness.

India is expected to be the fastest-growing major market in the region, supported by increasing urbanization, expanding female workforce participation, growing fashion consciousness among millennials and Gen Z consumers, and rising penetration of e-commerce platforms. Government initiatives promoting domestic manufacturing and digital commerce are further supporting industry expansion. Japan and South Korea continue to generate strong demand for luxury and premium accessories, driven by high per-capita spending, mature retail infrastructure, and strong consumer preference for branded products. Meanwhile, Southeast Asian countries including Indonesia, Vietnam, Thailand, and the Philippines are emerging as attractive growth markets due to rising middle-class incomes, increasing smartphone penetration, and growing influence of social commerce platforms. The region also benefits from strong export-oriented production ecosystems that support global accessory supply chains.

North America

North America accounted for approximately 26% of global fashion accessories market revenue in 2026. The United States represents the largest regional market, driven by high consumer purchasing power, strong luxury brand penetration, well-established retail networks, and advanced omnichannel commerce infrastructure. Consumer demand remains particularly robust for premium handbags, luxury watches, designer eyewear, and fine jewelry. The growing popularity of personalized fashion accessories and direct-to-consumer retail models continues to support market expansion.

One of the primary growth drivers in North America is the increasing willingness of consumers to spend on lifestyle and status-oriented products. High levels of social media engagement, influencer marketing, and celebrity-driven fashion trends significantly impact purchasing decisions. The region also leads in technology-enabled fashion accessories, including smart watches, connected jewelry, and wearable devices. Canada contributes additional market growth through increasing luxury spending, rising adoption of sustainable fashion products, and continued expansion of digital retail channels. Furthermore, North America's mature logistics infrastructure and strong consumer preference for premium brands support higher average selling prices compared to most global markets.

Europe

Europe remains one of the most influential regions in the global fashion accessories industry, accounting for approximately 21% of global market demand. The region benefits from a long-established fashion heritage, the presence of globally recognized luxury brands, and strong consumer spending on premium products. France, Italy, Germany, Switzerland, and the United Kingdom represent the largest demand centers, collectively accounting for the majority of regional consumption.

Regional growth is supported by Europe's position as a global luxury manufacturing and export hub. Italy and France continue to dominate premium leather goods, handbags, and luxury fashion accessories, while Switzerland remains the global center for luxury watch production. Increasing tourism across major European fashion capitals such as Paris, Milan, London, and Zurich contributes significantly to luxury accessory sales. Sustainability is also becoming a major purchasing driver, with European consumers demonstrating stronger preferences for ethically sourced materials, recycled products, and transparent supply chains than many other regions. Additionally, growing adoption of circular fashion models, including resale platforms and refurbishment services, is creating new revenue opportunities across the region.

Latin America

Latin America represents a smaller but steadily expanding market for fashion accessories, with Brazil and Mexico accounting for the majority of regional demand. Market growth is being driven by increasing fashion awareness, rising urbanization, improving retail infrastructure, and growing penetration of e-commerce platforms. Consumers in major metropolitan areas are increasingly adopting international fashion trends, creating opportunities for both global and regional brands.

Brazil remains the largest market in the region due to its sizeable consumer population and established fashion industry. Mexico continues to benefit from increasing disposable incomes, proximity to North American supply chains, and growing luxury retail investments. The expansion of digital payment systems, social commerce, and mobile shopping applications is improving product accessibility across the region. Premiumization trends among upper-middle-income consumers are also contributing to rising demand for luxury handbags, watches, jewelry, and designer accessories. Despite economic volatility in some countries, increasing participation of younger consumers in fashion spending continues to support long-term market growth.

Middle East & Africa

The Middle East & Africa region is emerging as one of the fastest-growing markets for fashion accessories globally. The Middle East, particularly Saudi Arabia, the United Arab Emirates, and Qatar, is witnessing strong growth in luxury accessory demand due to high disposable incomes, expanding affluent populations, and increasing tourism activity. Luxury handbags, fine jewelry, premium watches, and designer eyewear represent the most sought-after product categories across Gulf Cooperation Council (GCC) countries.

Regional growth is further supported by government-led economic diversification programs, including Saudi Vision 2031 and major tourism development projects across the UAE and Saudi Arabia. These initiatives are attracting international luxury brands and increasing consumer spending on premium lifestyle products. In Africa, South Africa remains the largest market due to its relatively developed retail infrastructure and growing middle-income consumer base. Nigeria, Kenya, and Egypt are also emerging as attractive markets as urbanization, digital commerce adoption, and fashion awareness continue to increase. Tourism-related luxury purchases, particularly in Dubai and other major retail destinations, contribute significantly to regional accessory sales. The increasing presence of international luxury retailers and growing consumer demand for branded products are expected to sustain strong market growth throughout the forecast period.