Electric Guitar Market Size

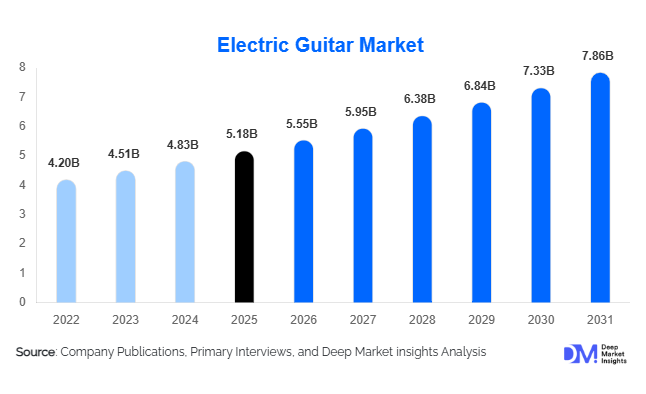

According to Deep Market Insights, the global electric guitar market size was valued at USD 5.18 billion in 2025 and is projected to grow from USD 5.55 billion in 2026 to reach USD 7.86 billion by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The electric guitar market growth is primarily driven by rising participation in music education, increasing popularity of home-based music production, growing demand from independent musicians and content creators, and the resurgence of live music performances worldwide. Technological innovations in pickup systems, digital sound processing, smart connectivity, and online learning ecosystems are further supporting market expansion. Additionally, the increasing availability of high-quality mid-range instruments and growing consumer interest in premium and custom-built guitars are creating favorable conditions for sustained market growth across both developed and emerging economies.

Key Market Insights

- Solid-body electric guitars account for nearly 58% of global revenue, owing to their versatility across rock, pop, blues, and metal music genres.

- Intermediate hobbyists represent the largest end-user category, contributing approximately 38% of global demand as players upgrade from entry-level instruments.

- Asia-Pacific dominates the global market, supported by strong manufacturing capabilities and rising domestic consumption across China, Japan, India, and South Korea.

- North America remains the largest premium electric guitar market, driven by high disposable income and strong participation in live music and recording activities.

- Online sales channels are expanding rapidly, supported by direct-to-consumer strategies and digital retail platforms.

- Smart guitar technologies and digital learning ecosystems are emerging as key differentiators among leading manufacturers.

Electric Guitar Market Trends

Digital Learning Ecosystems Reshaping Guitar Adoption

The electric guitar market is increasingly being influenced by digital learning platforms and subscription-based educational ecosystems. Manufacturers are integrating mobile applications, cloud-based lessons, AI-powered practice tools, and virtual coaching services with guitar purchases. This trend has significantly reduced barriers to entry for beginners while improving retention among new players. Guitar brands are investing heavily in digital content, interactive tutorials, and gamified learning experiences that appeal to younger demographics. The growing popularity of online music education platforms is also encouraging first-time purchases, particularly in emerging markets where access to traditional music instruction remains limited.

Growing Demand for Premium and Custom Instruments

Demand for premium electric guitars continues to grow among professional musicians, collectors, and serious hobbyists. Custom-shop instruments featuring handcrafted construction, premium tonewoods, artist-signature designs, and limited-edition releases are witnessing strong sales growth. Consumers are increasingly viewing electric guitars not only as musical instruments but also as lifestyle products and collectible assets. Premiumization trends are particularly evident in North America, Japan, Germany, and the United Kingdom, where buyers are willing to pay higher prices for craftsmanship, exclusivity, and brand heritage.

Electric Guitar Market Drivers

Expansion of Global Music Education Programs

The increasing inclusion of music education within school curricula and private learning institutions is contributing significantly to electric guitar demand. Governments, educational organizations, and private music academies continue to invest in music instruction programs that encourage instrument adoption among younger populations. The availability of affordable entry-level electric guitars has further strengthened market penetration among students and beginners. Growing participation in extracurricular music activities and online learning programs is expected to sustain long-term demand.

Growth of Independent Music Creation and Content Production

The rapid growth of content creation platforms such as YouTube, TikTok, Instagram, and music streaming services has increased demand for musical instruments among creators and aspiring artists. Home recording studios and digital audio workstations have become more accessible, encouraging musicians to produce and distribute music independently. Electric guitars remain central to many music genres, supporting demand from content creators seeking authentic sound production and live performance capabilities.

Electric Guitar Market Restraints

Raw Material Supply Constraints

The electric guitar industry remains dependent on premium woods such as mahogany, maple, rosewood, and ebony. Environmental regulations, sustainable forestry requirements, and restrictions on international timber trade can affect material availability and increase production costs. These factors create pricing pressures for manufacturers and may impact profit margins, particularly within premium product categories.

Competition from Digital Music Production Technologies

The increasing adoption of electronic music production software, MIDI controllers, and virtual instrument technologies presents a challenge to traditional instrument markets. Younger creators increasingly utilize software-based music production tools that require limited instrumental proficiency. While electric guitars continue to maintain strong cultural relevance, competition from digital alternatives remains an important long-term restraint affecting market expansion.

Electric Guitar Market Opportunities

Expansion Across Emerging Consumer Markets

Countries including India, Indonesia, Vietnam, Brazil, Mexico, and the UAE represent significant growth opportunities for electric guitar manufacturers. Rising disposable incomes, expanding middle-class populations, and increasing exposure to global music trends are driving demand for musical instruments. Market penetration remains substantially lower than in developed economies, providing considerable room for expansion through localized pricing strategies, regional distribution networks, and educational partnerships.

Sustainable and Smart Guitar Development

Sustainability and technological innovation are creating new opportunities for manufacturers to differentiate products and attract younger consumers. The development of guitars using certified sustainable woods, recycled materials, and alternative composites is gaining momentum. Simultaneously, smart guitars featuring wireless connectivity, integrated effects processing, Bluetooth functionality, and digital recording capabilities are expanding the addressable customer base. These innovations support premium pricing while addressing evolving consumer preferences.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.18 Billion |

| Market Size in 2026 | USD 5.55 Billion |

| Market Size in 2031 | USD 7.86 Billion |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Solid-body electric guitars dominate the market with approximately 58% share of global revenue. Their versatility across multiple music genres, durability, affordability, and compatibility with a wide range of amplifiers and effects systems make them the preferred choice among both professional musicians and beginners. Semi-hollow body guitars continue to gain popularity within blues, jazz, and alternative music segments, while hollow-body electric guitars maintain a strong presence among niche professional users. Extended-range electric guitars, including seven-string and eight-string variants, are witnessing increasing demand from progressive metal and modern rock musicians. Premium custom-shop models and artist-signature guitars continue to generate strong margins for manufacturers despite lower sales volumes.

Price Range Insights

Mid-range electric guitars priced between USD 300 and USD 1,000 account for the largest portion of global revenue, representing approximately 42% of the market. Improvements in manufacturing quality have significantly enhanced product performance within this segment, attracting both new players and upgrading hobbyists. Entry-level instruments remain critical for market expansion, particularly in developing countries where affordability is a key purchase consideration. Premium and luxury guitars continue to outperform broader market growth rates due to increasing demand from professionals, collectors, and affluent consumers seeking exclusivity and craftsmanship.

Distribution Channel Insights

Offline retail stores remain the dominant distribution channel, accounting for approximately 61% of global sales. Consumers often prefer physical stores due to the ability to test instruments before purchasing and receive expert guidance. Specialty music retailers continue to play a crucial role in product demonstrations and after-sales support. However, online channels are expanding rapidly as manufacturers invest in direct-to-consumer strategies, virtual product demonstrations, and e-commerce platforms. Digital retail channels offer broader product selection, competitive pricing, and convenient purchasing experiences, making them increasingly popular among younger consumers.

End User Insights

Intermediate hobbyists represent the largest end-user segment, contributing approximately 38% of total market demand. This segment is characterized by frequent product upgrades, accessory purchases, and increasing investment in premium instruments. Professional musicians continue to drive demand for high-end and custom-built guitars, particularly within touring, recording, and performance applications. Music schools, universities, and private academies represent a growing institutional customer base, supported by increasing investment in music education. Content creators and home studio users are emerging as one of the fastest-growing end-user groups, fueled by the continued expansion of digital media and independent music production.

Application Insights

Rock music remains the largest application segment, accounting for approximately 34% of global electric guitar demand. The genre's longstanding association with electric guitar performance continues to support instrument sales worldwide. Metal music represents a significant market for extended-range guitars and active pickup systems, while blues and jazz applications maintain demand for semi-hollow and hollow-body instruments. Pop music, worship music, and alternative genres are contributing to broader market diversification. Increasing demand from content creators, streaming performers, and social media musicians is creating new application opportunities beyond traditional music industry channels.

Explore more data points, trends and opportunities Download Free Sample Report

Electric Guitar Market Segmentations

By Product Type

- Solid Body Electric Guitars

- Semi-Hollow Body Electric Guitars

- Hollow Body Electric Guitars

- Electro-Acoustic / Acoustic-Electric Guitars

By End User

- Beginner / Learner Musicians

- Intermediate Hobbyists

- Professional Musicians

- Music Institutions & Academies

- Recording Studios & Production Houses

By Distribution Channel

- Offline Retail Stores

- Brand-Owned Stores

- Multi-Brand Musical Instrument Retailers

- Online Retail Platforms

- Direct-to-Consumer Brand Websites

By Pickup Configuration

- Single Coil

- Humbucker

- P90

- Active Pickup Systems

- Hybrid Pickup Configurations

By Price Range

- Entry-Level (Below USD 300)

- Mid-Range (USD 300–1,000)

- Premium (USD 1,000–3,000)

- Luxury / Custom Shop (Above USD 3,000)

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 38% of the global electric guitar market and remains both the largest production center and the fastest-growing consumption region. China serves as the world's primary manufacturing hub, supplying entry-level and mid-range instruments globally. Japan remains a major premium market supported by strong domestic brands and high consumer spending on musical instruments. India is emerging as one of the fastest-growing national markets, driven by expanding music education programs, rising disposable incomes, and growing youth interest in contemporary music. South Korea and Indonesia continue to benefit from strong music culture and increasing instrument adoption among younger demographics.

North America

North America holds approximately 27% of global market revenue and remains the most profitable regional market for premium electric guitars. The United States alone contributes over 22% of worldwide demand due to its extensive musician base, strong live entertainment industry, and concentration of leading guitar brands. Canada also demonstrates stable growth supported by music education initiatives and a vibrant independent music scene. Premium instruments, custom-shop models, and digital learning platforms perform particularly well across North America.

Europe

Europe represents approximately 24% of global demand, with Germany, the United Kingdom, France, Italy, and Spain serving as key markets. Germany functions as a major import and distribution hub for musical instruments, while the United Kingdom maintains strong demand due to its influential music culture and large population of active musicians. European consumers demonstrate increasing interest in sustainable manufacturing practices and premium instrument categories, supporting growth across both professional and enthusiast segments.

Latin America

Brazil and Mexico account for the majority of electric guitar demand across Latin America. Rising disposable incomes, expanding music education programs, and growing popularity of contemporary music genres are supporting market expansion. Local music cultures continue to create opportunities for both international and regional guitar brands.

Middle East & Africa

The Middle East and Africa currently represent the smallest regional market but offer strong long-term growth potential. The UAE and Saudi Arabia are witnessing increased demand due to investments in entertainment infrastructure, live events, and music education. South Africa remains the largest market within Africa, supported by a well-established music industry and growing consumer interest in modern musical instruments.

Key Players in the Electric Guitar Market

- Fender Musical Instruments Corporation

- Gibson Brands

- Ibanez (Hoshino Gakki)

- Yamaha Corporation

- PRS Guitars

- ESP Guitars

- Schecter Guitar Research

- Cort Guitars

- Jackson Guitars

- Music Man

- Gretsch

- Godin Guitars

- Charvel

- Reverend Guitars

- Rickenbacker International Corporation