Crocodile Leather Market Size

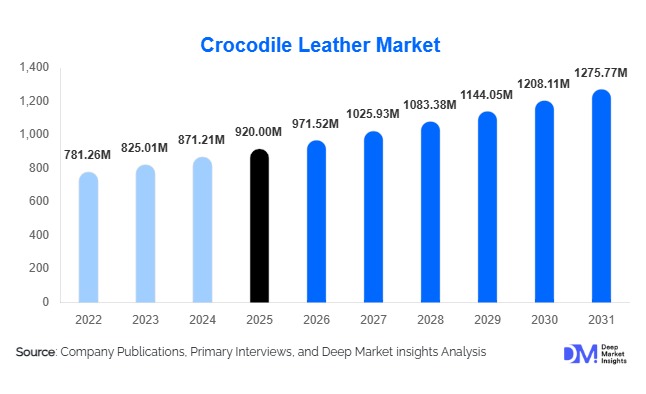

According to Deep Market Insights, the global crocodile leather market size was valued at USD 920 million in 2025 and is projected to grow from USD 971.52 million in 2026 to reach USD 1,275.77 million by 2031, expanding at a CAGR of 5.6% during the forecast period (2026–2031). The crocodile leather market growth is primarily driven by rising global luxury goods consumption, increasing demand for ultra-premium handbags and accessories, growing spending by high-net-worth individuals, and the expanding use of exotic leather in luxury automotive, aviation, and bespoke lifestyle products. The market benefits from controlled supply dynamics, strict international trade regulations, and the exclusivity associated with crocodile leather, enabling manufacturers and luxury brands to maintain premium pricing structures. Increasing consumer preference for traceable and sustainably sourced exotic leather products is further shaping industry developments, while investments in crocodile farming, tanning technologies, and vertically integrated supply chains continue to strengthen market competitiveness globally.

Key Market Insights

- Luxury handbags remain the largest product category, accounting for approximately 42% of global crocodile leather demand in 2025.

- Asia-Pacific dominates the global market, representing nearly 34% of total revenue, supported by strong luxury consumption across China, Japan, South Korea, and Southeast Asia.

- Premium-grade crocodile leather accounts for approximately 68% of market value, reflecting growing demand for high-quality exotic skins among luxury brands.

- Luxury fashion and accessories represent the largest end-use sector, contributing nearly 58% of total market demand.

- Automotive, private aviation, and luxury marine interiors are emerging as high-growth applications for premium crocodile leather products.

- Traceability, sustainability certification, and ESG compliance are becoming key purchasing criteria among global luxury houses.

- Vertical integration strategies by luxury conglomerates continue to reshape sourcing and supply chain management across the industry.

Crocodile Leather Market Trends

Sustainable and Traceable Exotic Leather Supply Chains Becoming Industry Standard

The crocodile leather industry is undergoing a significant transformation toward transparency and sustainability. Luxury brands are increasingly demanding complete traceability from farm to finished product, ensuring compliance with animal welfare, environmental, and international trade regulations. Certified crocodile farms and tanneries are becoming preferred suppliers as luxury consumers seek assurance regarding ethical sourcing practices. Blockchain-enabled traceability platforms, digital authentication systems, and farm certification programs are being implemented to improve visibility throughout the supply chain. As environmental, social, and governance (ESG) considerations become increasingly important within the luxury sector, sustainably sourced crocodile leather is expected to command higher premiums and gain broader acceptance among affluent consumers.

Expansion Beyond Fashion into Luxury Mobility and Interior Applications

Crocodile leather is increasingly finding applications beyond traditional handbags and accessories. Luxury automotive manufacturers, private jet operators, yacht builders, and premium interior designers are incorporating exotic leather into bespoke projects. Customized vehicle interiors, aircraft cabins, executive office furnishings, and luxury residential spaces are creating new demand streams for premium crocodile skins. These applications typically require high-grade leather and offer significantly higher margins than conventional fashion products. The growing popularity of personalization and bespoke luxury experiences among ultra-high-net-worth individuals is expected to accelerate adoption across these emerging applications over the coming decade.

Crocodile Leather Market Drivers

Growing Global Luxury Goods Consumption

The continued expansion of the global luxury goods industry remains the primary growth driver for the crocodile leather market. Rising disposable incomes among affluent consumers, increasing numbers of high-net-worth individuals, and strong demand for exclusive products have supported sales of crocodile leather handbags, footwear, wallets, belts, and watch straps. Luxury consumers increasingly value craftsmanship, rarity, and status symbolism, all of which are strongly associated with crocodile leather products. Demand growth is particularly evident across Asia-Pacific and the Middle East, where luxury spending continues to outpace many mature markets.

Rising Demand for Bespoke and Personalized Luxury Products

Consumer preferences are shifting toward customized luxury experiences and one-of-a-kind products. Crocodile leather's unique texture and rarity make it highly attractive for bespoke handbags, luxury footwear, personalized accessories, and custom automotive interiors. Luxury brands are increasingly offering made-to-order programs featuring exotic leather materials, enabling consumers to customize colors, finishes, and designs. This trend not only increases product value but also supports higher leather consumption per transaction, contributing positively to overall market growth.

Strategic Investments and Vertical Integration by Luxury Groups

Major luxury conglomerates have significantly expanded investments in crocodile farms, tanneries, and leather processing facilities to secure long-term supply. Vertical integration strategies help manufacturers maintain quality control, reduce supply risks, and improve sustainability compliance. Such investments strengthen supply chain resilience while supporting product exclusivity. Increased ownership of upstream production assets by luxury brands is expected to remain a major industry growth catalyst throughout the forecast period.

Crocodile Leather Market Restraints

Stringent Regulatory Requirements and Ethical Concerns

The crocodile leather industry operates under strict international regulations governing wildlife trade, including CITES requirements and country-specific import-export controls. Compliance increases administrative complexity and operating costs across the value chain. Additionally, growing consumer awareness regarding animal welfare issues presents reputational challenges for luxury brands utilizing exotic leathers. Public scrutiny and advocacy campaigns may influence purchasing decisions among certain consumer segments, potentially constraining market expansion.

Limited Availability of Premium-Grade Skins

The production of high-quality crocodile leather remains constrained by biological growth cycles, breeding limitations, and strict quality requirements. Only a relatively small proportion of harvested skins meet luxury-grade specifications, resulting in limited supply availability. Weather conditions, disease outbreaks, and production inefficiencies can further impact skin quality and output. These factors contribute to persistent supply shortages and upward pricing pressure within the market.

Crocodile Leather Market Opportunities

Expansion of Certified Sustainable Luxury Products

The growing importance of sustainability within the luxury sector presents substantial opportunities for crocodile leather producers and manufacturers. Certified farms, environmentally responsible tanning facilities, and transparent supply chains are increasingly valued by luxury brands and end consumers. Companies capable of demonstrating sustainability credentials and ethical sourcing practices are likely to secure premium contracts and strengthen long-term customer relationships. Emerging digital traceability technologies further support differentiation in this area.

Growth in Luxury Automotive, Aviation, and Marine Interiors

The ultra-premium transportation sector offers significant growth opportunities for crocodile leather suppliers. Luxury automobile manufacturers, private jet operators, yacht builders, and executive transportation providers increasingly incorporate exotic leather materials into customized interior projects. These segments offer higher average transaction values, lower price sensitivity, and growing demand for personalization. As global wealth creation continues, demand for bespoke mobility solutions is expected to support new revenue opportunities across the crocodile leather value chain.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 920 Million |

| Market Size in 2026 | USD 971.52 Million |

| Market Size in 2031 | USD 1275.77 Million |

| CAGR | 5.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Leather Source Type Insights

Saltwater crocodile (Porosus) leather dominated the global crocodile leather market, accounting for approximately 32% of total revenue in 2025. The segment maintains its leadership position primarily due to its exceptional scale uniformity, superior skin quality, minimal blemishes, and distinctive aesthetic appeal, making it the preferred material for ultra-premium luxury products. Global luxury fashion houses consistently prioritize Porosus skins for flagship handbag collections, limited-edition accessories, bespoke footwear, and high-value watch straps because of their rarity and ability to command substantial pricing premiums.

The key growth driver for this segment is the continued expansion of the global ultra-luxury goods industry, particularly among high-net-worth individuals (HNWIs) and ultra-high-net-worth individuals (UHNWIs) seeking exclusive and investment-grade luxury products. Luxury brands increasingly utilize Porosus leather to differentiate premium collections and reinforce brand prestige. Additionally, controlled farming operations in Australia and Southeast Asia ensure stable quality standards while maintaining scarcity, supporting long-term price appreciation.

Nile crocodile leather remains the second-largest segment due to its favorable balance between quality, availability, and cost-effectiveness, making it widely used across premium handbags and accessories. American alligator leather continues to maintain strong demand in North America, particularly within luxury footwear, belts, and watch straps. Meanwhile, caiman leather serves the more accessible luxury segment, providing manufacturers with a lower-cost alternative while retaining the exotic leather appeal sought by aspirational consumers. Growing investments in certified crocodile farming, sustainable sourcing programs, and digital traceability technologies are expected to further strengthen demand for premium Porosus leather throughout the forecast period.

Product Type Insights

Handbags and luxury bags represented the largest product segment, accounting for approximately 42% of global crocodile leather market demand in 2025. The segment's dominance is directly linked to the strategic importance of handbags within the global luxury goods industry. Luxury handbags typically serve as flagship products for leading fashion houses and generate some of the highest profit margins across luxury portfolios. Crocodile leather handbags are often positioned as ultra-premium, limited-production products that enhance brand exclusivity and attract affluent consumers seeking status-driven purchases.

The primary driver supporting segment growth is the continued expansion of luxury personal goods spending globally, particularly in Asia-Pacific, North America, and the Middle East. Consumers increasingly view exotic leather handbags as collectible assets and symbols of wealth, creating strong replacement and repeat purchase demand. Furthermore, the rise of bespoke luxury services allows customers to customize colors, finishes, hardware, and designs, increasing the value and attractiveness of crocodile leather handbags.

Wallets, card holders, and other small leather goods continue to generate significant demand due to their relatively lower entry price points within the luxury segment, enabling brands to expand their customer base. Premium footwear, belts, and watch straps also maintain stable growth, supported by increasing demand for personalized luxury accessories. Meanwhile, luxury travel goods and luggage are emerging as a high-growth niche as affluent consumers seek coordinated luxury lifestyle products across multiple categories. The increasing popularity of limited-edition collections, celebrity endorsements, and luxury resale platforms is expected to further strengthen the handbags segment's leadership position over the coming years.

Grade Insights

Premium-grade crocodile leather accounted for approximately 68% of total market value in 2025, making it the dominant quality segment globally. This leadership is primarily attributed to the market's strong concentration within luxury applications where visual perfection, durability, and craftsmanship are critical purchasing criteria. Premium-grade skins feature highly symmetrical scale patterns, uniform texture, superior tensile strength, and minimal natural imperfections, making them suitable for the highest-value luxury products. The key growth driver for this segment is the increasing consumer preference for exclusivity and artisanal craftsmanship. Luxury consumers are increasingly willing to pay substantial premiums for products manufactured using flawless exotic leather materials. In addition, luxury brands maintain strict quality control requirements and often reject skins that do not meet premium specifications, reinforcing demand for top-grade raw materials.

Growing wealth concentration among affluent consumers, combined with increasing demand for bespoke products and limited-edition luxury collections, continues to support premium-grade leather consumption. Furthermore, luxury brands are investing heavily in supply chain traceability and quality assurance programs to secure access to high-grade skins and maintain product consistency. Standard-grade crocodile leather primarily serves premium commercial products, while lower-grade materials are utilized in niche applications where functionality is prioritized over aesthetic perfection. However, premium-grade products are expected to maintain market leadership due to their strong association with luxury exclusivity and brand positioning.

Distribution Channel Insights

Direct luxury brand boutiques accounted for approximately 45% of global crocodile leather product sales in 2025, making them the largest distribution channel. This dominance reflects the luxury industry's emphasis on brand-controlled customer experiences, product authentication, and premium service offerings. Consumers purchasing crocodile leather products often seek personalized consultations, exclusive access to limited collections, and assurance regarding product authenticity, all of which are most effectively delivered through brand-owned retail networks. The primary growth driver for this segment is the continued expansion of global luxury retail infrastructure, particularly in key luxury consumption hubs such as China, the United States, the UAE, France, Italy, Japan, and South Korea. Leading luxury houses continue investing in flagship stores and experiential retail concepts that enhance customer engagement and reinforce brand exclusivity.

Specialty luxury retailers remain important distribution partners, particularly for independent luxury brands and bespoke product manufacturers. Online luxury platforms are experiencing rapid growth due to increasing digital adoption among affluent consumers and advancements in luxury e-commerce capabilities. However, the high-value nature of crocodile leather products means many consumers still prefer in-person purchasing experiences before making significant luxury investments. Omnichannel retail strategies, digital authentication systems, and personalized clienteling services are expected to further strengthen direct-to-consumer sales channels throughout the forecast period.

End-Use Industry Insights

Luxury fashion and accessories remained the largest end-use industry, accounting for nearly 58% of total crocodile leather consumption globally in 2025. The segment's leadership reflects crocodile leather's long-standing association with prestige, exclusivity, and luxury craftsmanship. Handbags, footwear, wallets, belts, watch straps, and other high-end accessories continue to represent the primary commercial applications for premium crocodile leather products. The principal growth driver is the continued expansion of the global luxury personal goods industry, which exceeds several hundred billion dollars in annual retail sales and remains highly resilient among affluent consumer segments. Rising disposable incomes, increasing luxury spending by younger affluent consumers, and expanding luxury retail penetration across emerging markets continue to stimulate demand for exotic leather products.

Luxury automotive interiors represent the fastest-growing end-use segment, supported by increasing customization demand among premium vehicle buyers. Manufacturers of luxury automobiles, private jets, and superyachts increasingly incorporate crocodile leather into seating, dashboards, steering wheels, and cabin interiors to enhance exclusivity. Similarly, luxury furniture and interior design applications are gaining traction as wealthy consumers seek differentiated residential and hospitality environments. European luxury manufacturing hubs, particularly France and Italy, continue to drive substantial export-oriented demand by importing premium crocodile skins and converting them into high-value finished goods for global distribution. As luxury spending continues to expand globally, fashion and accessories are expected to remain the dominant end-use segment throughout the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Crocodile Leather Market Segmentations

By Leather Source Type

- Saltwater (Porosus) Crocodile Leather

- Nile Crocodile Leather

- American Alligator Leather

- Caiman Leather

- Other Crocodilian Leather Types

By Product Type

- Handbags & Luxury Bags

- Wallets & Small Leather Goods

- Footwear

- Belts

- Apparel & Garments

- Watch Straps

- Travel Goods & Luggage

- Luxury Accessories

- Automotive Interior Components

- Furniture & Decorative Upholstery

By Grade

- Premium Grade

- Standard Commercial Grade

- Lower Grade / Utility Grade

By Distribution Channel

- Direct Luxury Brand Boutiques

- Specialty Leather Goods Retailers

- Department Stores

- Online Luxury Retail Platforms

- Wholesale & B2B Supply

By End-Use Industry

- Luxury Fashion & Accessories

- Luxury Footwear

- Luxury Watches & Jewelry

- Automotive Interiors

- Furniture & Interior Design

- Corporate Gifting & Bespoke Products

- Aviation & Marine Luxury Interiors

Regional Insights

North America

North America accounted for approximately 22% of global crocodile leather market demand in 2025, with the United States representing nearly 20% of total global consumption. The region's strong market position is supported by one of the world's largest concentrations of high-net-worth consumers, robust luxury spending patterns, and a highly developed luxury retail ecosystem. The United States remains a major consumer of premium handbags, luxury footwear, watch straps, and bespoke accessories manufactured using exotic leathers.

The primary growth driver for North America is the increasing demand for customized luxury products and limited-edition collections among affluent consumers. Additionally, the region benefits from a strong luxury automotive customization industry and growing demand for premium lifestyle products. Rising adoption of luxury e-commerce platforms and expanding resale markets for investment-grade luxury goods are also contributing to regional market growth.

Europe

Europe accounted for approximately 30% of global crocodile leather demand in 2025, making it the second-largest regional market and the world's leading luxury manufacturing hub. France contributed approximately 11% of global demand, while Italy accounted for nearly 9%, reflecting their dominant roles in luxury fashion, leather craftsmanship, and export-oriented manufacturing.

The key growth driver for Europe is its unparalleled concentration of global luxury brands, tanneries, and high-end manufacturing facilities. France houses many of the world's largest luxury fashion groups, while Italy remains a center for premium leather processing and artisanal production. Strong export demand from Asia-Pacific, North America, and the Middle East further supports regional consumption of crocodile leather. In addition, increasing investments in sustainable luxury manufacturing and supply chain traceability continue to strengthen Europe's competitive position.

Asia-Pacific

Asia-Pacific led the global crocodile leather market with approximately 34% market share in 2025 and is expected to remain the fastest-growing regional market through 2031. China alone accounted for nearly 15% of global demand, followed by Japan, South Korea, and rapidly expanding Southeast Asian luxury markets.

The primary growth driver is the rapid expansion of affluent consumer populations across China, India, Southeast Asia, and South Korea. Rising disposable incomes, increasing luxury brand penetration, and growing consumer preference for status-oriented products continue to stimulate demand for crocodile leather accessories. The region also benefits from significant crocodile farming and leather processing activities, particularly in Thailand and Vietnam, which support regional supply chains.

India is emerging as one of the fastest-growing luxury markets globally, supported by increasing wealth creation, luxury retail expansion, and a growing appetite for premium international brands. Social media influence, luxury tourism, and digital luxury commerce are further accelerating regional market growth.

Latin America

Latin America accounted for approximately 6% of global crocodile leather demand in 2025. Brazil and Mexico remain the region's largest markets due to expanding affluent consumer populations and growing penetration of international luxury brands.

The primary growth driver for Latin America is the gradual expansion of luxury consumption among upper-income households and increasing investment in premium retail infrastructure. Brazil also contributes to regional market development through crocodilian farming activities and local leather production capabilities. While market penetration remains lower than in mature luxury regions, increasing urbanization, rising disposable incomes, and expanding luxury retail networks are expected to support long-term growth.

Middle East & Africa

The Middle East & Africa region accounted for approximately 8% of global market revenue in 2025. The UAE and Saudi Arabia remain the largest luxury consumption centers, while Africa plays a critical role in crocodile farming and raw material supply.

The key growth driver for the Middle East is the region's high concentration of ultra-high-net-worth individuals, strong luxury purchasing power, and increasing investment in premium retail developments. Luxury tourism, international fashion retail expansion, and growing demand for bespoke products continue to stimulate crocodile leather consumption. In Africa, expanding commercial crocodile farming operations, improving export capabilities, and increasing investment in sustainable wildlife management programs are supporting supply-side growth and strengthening the region's strategic importance within the global crocodile leather value chain.

Key Players in the Crocodile Leather Market

- Hermès International

- LVMH

- Kering

- Heng Long International

- Pan Am Leathers

- TopCroc

- Crocodile Products Industries

- American Tanning & Leather

- Mekong Delta Crocodile

- Rojana Industrial Crocodile Farm

- Wild Croc International

- Croc Stock & Barra

- Siam Crocodile

- Nuti Ivo Group

- France Croco