Consumer Audio Market Size

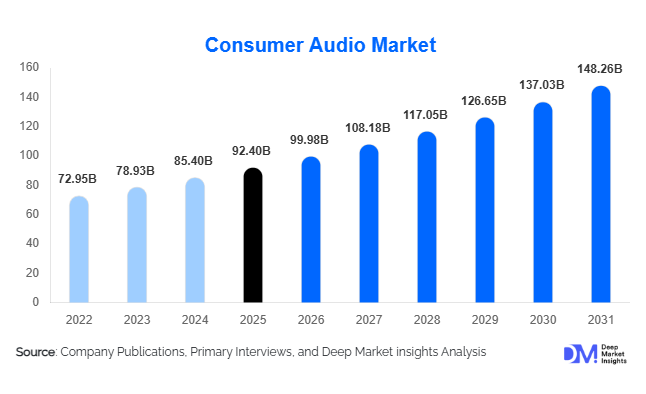

According to Deep Market Insights, the global consumer audio market size was valued at USD 92.4 billion in 2025 and is projected to grow from USD 99.98 billion in 2026 to reach USD 148.26 billion by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The consumer audio market growth is primarily driven by rising adoption of wireless audio devices, increasing demand for immersive entertainment experiences, rapid penetration of streaming platforms, and growing integration of smart technologies into personal audio ecosystems.

Key Market Insights

- True wireless stereo (TWS) earbuds continue to dominate product demand, driven by smartphone ecosystem integration, portability, and premium sound features.

- Wireless audio devices account for the majority of market revenue, supported by advancements in Bluetooth Low Energy connectivity, battery optimization, and seamless multi-device compatibility.

- Asia-Pacific dominates global consumer audio demand, led by China, India, Japan, and South Korea due to strong manufacturing ecosystems and expanding middle-class consumption.

- Premium audio categories are growing faster than mass-market products, supported by rising adoption of active noise cancellation, spatial audio, and AI-powered sound personalization.

- Gaming, content creation, and hybrid work environments are emerging as high-growth demand centers, accelerating adoption of professional-grade headsets and immersive sound systems.

- AI-enabled audio experiences and smart assistant integration are increasingly shaping product differentiation strategies among leading manufacturers.

Consumer Audio Market Trends

Shift Toward Wireless and Smart Audio Ecosystems

The consumer audio industry is rapidly transitioning toward fully wireless and ecosystem-connected devices. Consumers increasingly prefer Bluetooth-enabled headphones, smart speakers, and soundbars that seamlessly integrate with smartphones, smart TVs, wearables, and voice-assistant platforms. The growing adoption of AI-enabled adaptive sound processing, multi-device pairing, and spatial audio technologies is reshaping consumer expectations. Premium brands are focusing heavily on ecosystem retention strategies by offering synchronized audio experiences across multiple devices. This trend is especially strong in North America, China, South Korea, and Western Europe where smart-home adoption continues to accelerate.

Rising Demand for Immersive and Personalized Audio Experiences

Consumers are increasingly prioritizing immersive listening experiences for entertainment, gaming, and productivity applications. Technologies such as active noise cancellation (ANC), Dolby Atmos, head-tracking spatial audio, and AI-based sound optimization are becoming mainstream across premium audio categories. Gaming-focused audio products with ultra-low latency and 3D sound mapping are witnessing strong demand growth globally. In addition, manufacturers are leveraging AI algorithms to customize equalizer settings based on user behavior and environmental conditions. This trend is helping companies improve product differentiation and increase average selling prices in premium segments.

Consumer Audio Market Drivers

Growing Adoption of Streaming Platforms and Digital Entertainment

The expansion of music streaming platforms, podcasts, OTT video services, and online gaming ecosystems continues to drive global demand for high-quality consumer audio devices. Consumers are increasingly investing in premium headphones, soundbars, and smart speakers to improve entertainment experiences at home and on the move. The rapid growth of esports and livestreaming industries is also supporting demand for gaming headsets and immersive audio solutions. Increasing consumption of digital content across smartphones, tablets, laptops, and connected TVs remains one of the strongest long-term growth drivers for the market.

Rapid Expansion of TWS Earbuds and Wireless Audio Devices

The removal of headphone jacks from smartphones has accelerated the shift toward wireless audio technologies globally. TWS earbuds have become mainstream products across both premium and entry-level segments due to improved affordability, compact design, longer battery life, and enhanced sound quality. Consumer preference for mobility, convenience, and cable-free experiences continues to strengthen wireless product adoption. Manufacturers are increasingly focusing on battery innovation, lightweight materials, and seamless device synchronization to support future growth.

Consumer Audio Market Restraints

Intense Price Competition in Mid-Range and Budget Segments

The consumer audio market remains highly competitive, particularly in entry-level and mid-range categories where numerous regional and Chinese manufacturers compete aggressively on pricing. This intense competition places pressure on profit margins for established global brands. Frequent product launches and shorter replacement cycles further increase inventory risks and pricing volatility. Companies operating in budget segments often struggle to maintain profitability while balancing feature innovation and cost efficiency.

Supply Chain Volatility and Raw Material Dependency

The market remains vulnerable to disruptions in semiconductor supply, battery material pricing, logistics costs, and geopolitical trade tensions. Rising lithium-ion battery costs, semiconductor shortages, and transportation bottlenecks can significantly impact manufacturing economics and product availability. Dependence on concentrated manufacturing hubs in East Asia also increases operational risks during geopolitical or supply chain disruptions. Environmental regulations regarding battery disposal and electronic waste management are adding further compliance costs for manufacturers globally.

Consumer Audio Market Opportunities

AI-Enabled Audio Personalization and Smart Hearables

Artificial intelligence integration is creating substantial opportunities across premium consumer audio categories. Manufacturers are increasingly introducing AI-powered adaptive sound tuning, real-time voice enhancement, hearing optimization, and personalized equalization capabilities. Hearables and smart wearable audio devices are emerging as important next-generation growth categories with applications extending beyond entertainment into wellness, productivity, and healthcare-adjacent use cases. The expansion of voice-assistant ecosystems and connected smart-home platforms is expected to further accelerate demand for intelligent audio devices globally.

Emerging Market Expansion and Affordable Wireless Penetration

Emerging economies across Asia-Pacific, Latin America, and the Middle East present significant long-term opportunities for market participants. Rising smartphone penetration, improving internet connectivity, growing middle-class populations, and increasing digital entertainment consumption are driving adoption of affordable wireless audio devices. Countries such as India, Indonesia, Vietnam, Brazil, and Saudi Arabia are witnessing strong demand growth for Bluetooth earphones and portable speakers. Regional manufacturing expansion and localized pricing strategies are expected to further strengthen market penetration across price-sensitive consumer segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 92.4 Billion |

| Market Size in 2026 | USD 99.98 Billion |

| Market Size in 2031 | USD 148.26 Billion |

| CAGR | 8.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Headphones remain the dominant product segment within the consumer audio market, accounting for the largest share of global revenue due to strong demand for TWS earbuds, gaming headsets, and premium noise-cancelling devices. Consumers increasingly prioritize portability, seamless smartphone integration, and immersive sound experiences, driving sustained adoption across both developed and emerging markets. Portable Bluetooth speakers continue to experience strong demand growth due to affordability, outdoor entertainment usage, and increasing adoption among younger demographics. Smart speakers are also gaining momentum as smart-home ecosystems expand globally. Soundbars are witnessing rising adoption alongside premium television upgrades and home entertainment investments, particularly in North America and Europe where Dolby Atmos-enabled systems are becoming mainstream.

Connectivity Technology Insights

Wireless audio technologies dominate the global consumer audio market, accounting for more than two-thirds of total market revenue in 2025. Bluetooth-enabled devices continue to lead adoption due to improved connectivity stability, lower power consumption, and enhanced compatibility across multiple consumer electronics platforms. Wi-Fi-enabled speakers and smart-home audio systems are also gaining traction due to multi-room synchronization capabilities and smart assistant integration. Wired audio products continue to maintain relevance within professional audio, audiophile, and gaming applications where low latency and high-fidelity sound remain critical purchase considerations.

Distribution Channel Insights

Online retail platforms dominate global consumer audio sales, supported by expanding e-commerce penetration, competitive pricing, and increasing direct-to-consumer strategies adopted by major brands. E-commerce marketplaces enable consumers to compare product specifications, reviews, and pricing efficiently, significantly improving purchasing convenience. Brand-owned digital storefronts are also growing rapidly as manufacturers seek stronger customer engagement and margin control. Offline retail channels, including consumer electronics stores and specialty audio retailers, continue to play an important role in premium product demonstrations and experiential marketing. Omnichannel retail strategies are increasingly becoming critical for customer acquisition and retention.

End-Use Insights

Residential and personal entertainment applications account for the largest share of the consumer audio market due to increasing streaming consumption, smart-home adoption, and rising investments in home entertainment ecosystems. Gaming and esports applications represent one of the fastest-growing end-use segments, driven by cloud gaming expansion, competitive esports participation, and increasing demand for immersive sound technologies. Professional content creation, podcasting, and livestreaming applications are also contributing significantly to demand growth for studio-grade headphones and microphones. Corporate and hybrid work environments continue to support adoption of noise-cancelling headphones and conference audio systems as remote collaboration becomes increasingly normalized across industries.

Explore more data points, trends and opportunities Download Free Sample Report

Consumer Audio Market Segmentations

By Product Type

- Headphones

- Portable Bluetooth Speakers

- Smart Speakers

- Soundbars

- Home Theater & Hi-Fi Audio Systems

- Gaming Headsets

- Wearable & Smart Hearables

By Connectivity Technology

- Wired Audio Devices

- Bluetooth Audio Devices

- Wi-Fi Audio Systems

- Hybrid Connectivity Audio Systems

By Distribution Channel

- Online Retail

- Brand-Owned Stores

- Consumer Electronics Stores

- Hypermarkets & Supermarkets

- Specialty Audio Retailers

By End Use

- Residential & Personal Entertainment

- Gaming & Esports

- Professional Content Creation

- Corporate & Remote Work Applications

- Fitness & Sports

- Education & E-Learning

Regional Insights

North America

North America accounted for approximately 29% of the global consumer audio market in 2025, supported by strong premium product adoption, mature streaming ecosystems, and high disposable income levels. The United States remains the largest regional market due to widespread adoption of premium wireless earbuds, gaming headsets, smart speakers, and advanced home audio systems. Consumers in the region demonstrate strong preference for ecosystem-integrated products offering spatial audio, AI-based sound tuning, and seamless connectivity across devices. Canada also represents an important premium consumption market with growing adoption of home entertainment systems and smart speakers.

Europe

Europe remains a major market for premium consumer audio products, accounting for nearly 22% of global revenue. Germany, the United Kingdom, and France lead regional demand due to strong consumer electronics spending and increasing adoption of smart-home ecosystems. European consumers increasingly prioritize sustainability, energy-efficient electronics, and high-fidelity audio systems, encouraging manufacturers to focus on recyclable materials and environmentally responsible production practices. Demand for luxury audio products and audiophile-grade systems remains particularly strong across Western Europe.

Asia-Pacific

Asia-Pacific dominates the global consumer audio market with approximately 38% market share in 2025 and remains the fastest-growing region globally. China continues to serve as both the largest manufacturing hub and one of the largest consumer markets for audio products worldwide. India is witnessing rapid demand growth due to expanding smartphone penetration, affordable wireless device adoption, and rising digital entertainment consumption. Japan and South Korea remain key innovation centers for premium audio technologies, including AI-enabled sound processing, spatial audio, and advanced gaming audio systems. Southeast Asian countries are also emerging as important demand centers supported by growing middle-class populations and rising internet penetration.

Latin America

Latin America is experiencing steady growth in consumer audio adoption, led by Brazil and Mexico. Expanding digital entertainment ecosystems, increasing smartphone usage, and improving e-commerce infrastructure are supporting regional market expansion. Consumers in the region increasingly prefer affordable wireless earphones and portable speakers that balance functionality and pricing. International manufacturers are increasingly focusing on localized pricing strategies to improve penetration across price-sensitive markets.

Middle East & Africa

The Middle East & Africa region is witnessing increasing demand for premium consumer electronics driven by urbanization, rising disposable incomes, and strong smartphone penetration. Saudi Arabia and the UAE represent the leading premium consumption markets within the region, supported by strong luxury electronics demand and expanding smart-home adoption. South Africa remains an important market for affordable wireless audio products and portable entertainment devices. Regional demand is also benefiting from younger demographics and increasing digital content consumption.

Key Players in the Consumer Audio Market

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Sony Group Corporation

- Bose Corporation

- Harman International Industries

- Sonos Inc.

- Sennheiser Electronic GmbH & Co. KG

- Logitech International S.A.

- Xiaomi Corporation

- Panasonic Holdings Corporation

- JBL

- Skullcandy Inc.

- Edifier Technology Co., Ltd.

- Bang & Olufsen

- Anker Innovations