Coffee Roasters Market Size

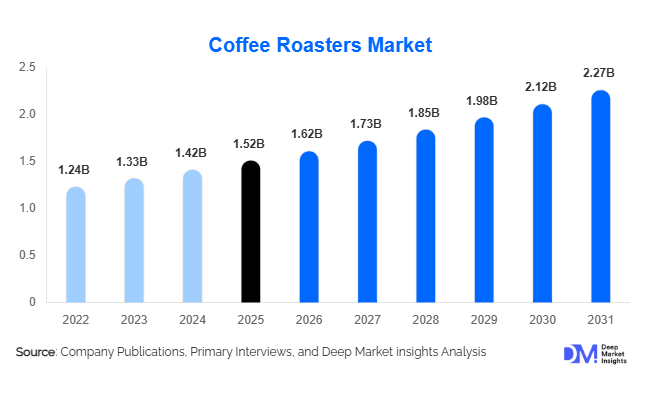

According to Deep Market Insights, the global coffee roasters market size was valued at USD 1.52 billion in 2025 and is projected to grow from USD 1.62 billion in 2026 to reach USD 2.27 billion by 2031, expanding at a CAGR of 6.9% during the forecast period (2026–2031). The coffee roasters market growth is primarily driven by the increasing global demand for specialty coffee, rapid expansion of café chains and artisanal roasteries, and rising investments in automated and energy-efficient roasting technologies. The growing preference for freshly roasted premium coffee beans among consumers is accelerating adoption of advanced roasting systems across commercial and industrial applications.

Key Market Insights

- Specialty coffee culture is rapidly transforming roasting operations globally, increasing demand for precision roasting systems capable of customized flavor profiling and small-batch roasting.

- Automation and AI integration are reshaping coffee roasting infrastructure, enabling improved consistency, predictive maintenance, and real-time roast analytics.

- North America dominates the global coffee roasters market, supported by strong specialty coffee consumption, established café chains, and extensive commercial roasting operations.

- Asia-Pacific is the fastest-growing regional market, driven by urban café expansion, rising disposable incomes, and growing coffee consumption in China, India, and Southeast Asia.

- Sustainability and emission-control technologies are becoming key purchasing criteria, especially in Europe and North America where environmental regulations are tightening.

- E-commerce coffee brands and subscription-based coffee services are creating new demand for modular and scalable roasting equipment globally.

Coffee Roasters Market Trends

Smart and Automated Roasting Systems Gaining Momentum

The coffee roasters industry is increasingly shifting toward automated and digitally connected roasting systems. Commercial coffee producers and specialty cafés are investing in IoT-enabled roasters, AI-based roast profiling software, and cloud-integrated monitoring platforms to improve operational efficiency and product consistency. Automated systems reduce dependence on skilled labor while enabling precise temperature management, airflow optimization, and repeatable roasting outcomes. Manufacturers are also incorporating predictive maintenance features and data analytics to minimize downtime and improve productivity. These innovations are particularly attractive for large-scale industrial coffee processors seeking scalability and energy optimization. Small and medium-sized specialty roasteries are similarly adopting compact smart roasters to differentiate product quality and streamline roasting workflows.

Sustainable and Energy-Efficient Roasting Technologies Expanding

Sustainability has emerged as a defining trend across the global coffee roasters market. Equipment manufacturers are developing low-emission roasting systems, heat recovery technologies, and electric-powered roasters to comply with tightening environmental regulations and rising consumer expectations around sustainable coffee production. Europe is leading adoption of environmentally responsible roasting technologies, particularly in Germany, the Netherlands, and Scandinavian countries. Biomass-fueled and hybrid roasting systems are also gaining traction among specialty coffee producers seeking to reduce carbon footprints. Companies are increasingly integrating energy monitoring tools and emission filtration systems into roasting equipment to improve environmental performance while lowering long-term operational costs.

Coffee Roasters Market Drivers

Growing Global Demand for Specialty Coffee

The rapid expansion of specialty coffee consumption is one of the strongest drivers of the coffee roasters market. Consumers increasingly prefer premium single-origin coffee, artisanal blends, and customized roasting profiles that deliver differentiated flavor experiences. This trend is driving investments in small-batch roasting systems and technologically advanced commercial roasters capable of precision roasting. The rise of third-wave coffee culture across North America, Europe, and Asia-Pacific has accelerated the establishment of boutique cafés and independent roasting businesses. Younger consumers, particularly millennials and Gen Z demographics, are showing strong preference for ethically sourced and freshly roasted coffee products, further supporting market expansion.

Expansion of Café Chains and Foodservice Establishments

The global expansion of café chains and premium foodservice establishments is significantly increasing demand for coffee roasting equipment. International and regional coffee chains are investing in centralized roasting facilities and in-house roasting capabilities to strengthen quality control and brand differentiation. Urbanization, changing lifestyles, and increasing coffee consumption in emerging economies such as China, India, Vietnam, and the UAE are supporting café industry growth. Quick-service restaurants, luxury hotels, and premium restaurants are also integrating boutique roasting operations to offer customized coffee experiences and fresher products to consumers.

Coffee Roasters Market Restraints

High Capital Investment Requirements

One of the major challenges in the coffee roasters market is the high capital expenditure associated with industrial roasting equipment. Advanced roasting systems require substantial investment in machinery, installation, emission-control systems, ventilation infrastructure, and skilled operators. Small cafés and emerging specialty roasters often face financing limitations, restricting large-scale equipment adoption. The cost of upgrading to smart and automated roasting systems can also create barriers for smaller operators in price-sensitive markets.

Volatility in Green Coffee Bean Prices

Fluctuations in green coffee bean prices remain a significant restraint for the market. Climate change, supply chain disruptions, geopolitical instability, and adverse weather conditions in major coffee-producing countries such as Brazil and Vietnam have contributed to raw material price volatility. Rising bean costs reduce profitability for coffee roasters and may delay investment decisions related to new roasting equipment. Additionally, increasing energy prices and transportation costs are creating operational pressure across the roasting value chain.

Coffee Roasters Market Opportunities

Growth of Specialty Coffee in Emerging Markets

Emerging economies such as India, China, Indonesia, Saudi Arabia, and Vietnam present significant opportunities for coffee roaster manufacturers. Rapid urbanization, increasing disposable income, and evolving consumer lifestyles are fueling café culture expansion and premium coffee consumption across these regions. Young urban consumers increasingly associate specialty coffee with modern lifestyle experiences, creating strong demand for compact commercial roasters and specialty roasting infrastructure. Regional café chains and artisanal coffee startups are expected to become major contributors to future equipment demand.

Expansion of Sustainable Roasting Technologies

The transition toward environmentally sustainable food processing operations is creating substantial opportunities for manufacturers of low-emission and energy-efficient coffee roasters. Governments and large coffee brands are emphasizing carbon reduction initiatives, encouraging adoption of electric roasters, heat recovery systems, and hybrid roasting technologies. Companies that offer sustainable roasting systems with improved energy efficiency and lower emissions are expected to secure long-term competitive advantages. The increasing adoption of ESG-focused procurement strategies among global coffee brands is further accelerating demand for sustainable roasting infrastructure.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.52 Billion |

| Market Size in 2026 | USD 1.62 Billion |

| Market Size in 2031 | USD 2.27 Billion |

| CAGR | 6.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Roaster Type Insights

Hot air and fluid-bed roasters dominate the market due to their ability to deliver consistent heat distribution, cleaner roasting profiles, and lower smoke generation. These systems are widely adopted by specialty coffee roasteries and premium cafés seeking improved flavor consistency and roasting precision. Drum roasters remain highly preferred among traditional artisanal coffee producers because of their ability to create deeper caramelization and distinctive flavor characteristics. Hybrid roasting systems are gaining popularity as operators seek to combine traditional roasting methods with energy-efficient airflow technologies. The growing preference for customized roast profiles and premium coffee experiences is further supporting demand for technologically advanced roasting systems globally.

Capacity Insights

Medium-capacity commercial roasters ranging between 5–15 kg account for a substantial share of the global market due to widespread adoption among specialty cafés and regional roasting businesses. These systems offer scalability, flexibility, and operational efficiency for small-to-medium coffee producers. Industrial roasting systems above 15 kg capacity are witnessing strong demand from packaged coffee manufacturers and multinational beverage companies seeking high-volume production capabilities. Small-batch roasters are also experiencing rapid growth due to rising consumer demand for limited-edition and artisanal coffee offerings. The increasing number of independent micro-roasteries globally is supporting the expansion of compact roasting equipment demand.

Automation Insights

Semi-automatic roasting systems currently dominate the market because they balance operator control with production efficiency. Specialty coffee roasters often prefer semi-automatic systems to maintain manual control over roasting parameters while benefiting from programmable features and operational consistency. Fully automated smart roasting systems are the fastest-growing segment due to increasing industry demand for labor optimization, quality consistency, and real-time roast monitoring. AI-enabled roasting systems capable of predictive analytics and cloud integration are becoming increasingly important among industrial coffee producers and large specialty roasting businesses.

End-Use Industry Insights

The specialty coffee industry remains the largest end-use segment within the coffee roasters market. Independent roasteries, premium cafés, and direct-to-consumer coffee brands are investing heavily in technologically advanced roasting systems to differentiate flavor quality and brand positioning. Foodservice establishments, including quick-service restaurant chains and luxury hospitality operators, are also expanding in-house roasting capabilities to improve freshness and customer experience. E-commerce coffee brands and subscription-based coffee services are emerging as fast-growing end-use segments, particularly in North America and Europe. Additionally, coffee-producing countries such as Brazil, Colombia, and Vietnam are increasingly investing in domestic roasting infrastructure to export higher-value roasted coffee products.

Distribution Channel Insights

Direct manufacturer sales remain the dominant distribution channel in the coffee roasters market, particularly for industrial-scale equipment and customized roasting solutions. Authorized dealer networks also play a critical role by providing installation support, maintenance services, and localized technical expertise. Online B2B equipment platforms are expanding rapidly as independent cafés and specialty coffee startups increasingly rely on digital procurement channels for cost comparison and product research. Specialty equipment retailers continue serving niche artisan roaster markets by offering training, technical consulting, and customized roasting solutions. Digital marketing and virtual equipment demonstrations are further transforming purchasing behavior within the industry.

Explore more data points, trends and opportunities Download Free Sample Report

Coffee Roasters Market Segmentations

By Roaster Type

- Drum Coffee Roasters

- Hot Air / Fluid Bed Roasters

- Direct Fire Roasters

- Hybrid Roasters

- Centrifugal Roasters

- Infrared Roasters

By Heat Source

- Gas-Fired Roasters

- Electric Roasters

- Hybrid Energy Roasters

- Biomass-Powered Roasters

By Capacity

- Micro Roasters (Up to 1 kg)

- Small Commercial Roasters (1–5 kg)

- Medium Commercial Roasters (5–15 kg)

- Industrial Roasters (15–60 kg)

- Large Industrial Continuous Roasters (Above 60 kg)

By Automation Level

- Manual Roasters

- Semi-Automatic Roasters

- Fully Automatic Roasters

- AI-Integrated Smart Roasters

By Application

- Commercial Coffee Shops

- Industrial Coffee Processing Plants

- Specialty Coffee Roasteries

- Hospitality Sector

- Institutional Foodservice

- Residential/Home Roasting

By Distribution Channel

- Direct Sales

- Authorized Dealers & Distributors

- Online B2B Platforms

- Specialty Equipment Retailers

Regional Insights

North America

North America remains the largest regional market for coffee roasters, accounting for nearly 33% of global market revenue in 2025. The United States dominates regional demand due to strong specialty coffee consumption, extensive café chain presence, and large-scale commercial roasting operations. Consumers increasingly prefer artisanal and freshly roasted coffee products, encouraging investment in advanced roasting infrastructure. Canada is also experiencing growth in premium coffee culture and boutique roasting businesses. The region benefits from strong technological adoption and high investment in automated roasting systems.

Europe

Europe represents one of the most mature and technologically advanced coffee roasting markets globally, contributing approximately 30% of total market share in 2025. Germany, Italy, France, the Netherlands, and the United Kingdom are major demand centers for industrial and specialty roasting equipment. Germany remains a global hub for roasting machinery manufacturing and engineering innovation, while Italy’s espresso culture continues driving commercial roasting demand. European markets are also leading adoption of low-emission and sustainable roasting technologies due to stringent environmental regulations and strong consumer emphasis on sustainability.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is projected to expand at over 8% CAGR through 2031. China and India are witnessing rapid café culture growth supported by urbanization, increasing disposable income, and changing consumer lifestyles. Japan and South Korea remain mature specialty coffee markets emphasizing premium coffee quality and advanced roasting technologies. Southeast Asian countries such as Vietnam, Indonesia, Thailand, and the Philippines are also experiencing rising investments in café infrastructure and domestic roasting operations. Expanding international coffee chains and rising social media influence are accelerating specialty coffee adoption across the region.

Latin America

Latin America plays a strategically important role in the coffee roasters market due to its position as a leading coffee-producing region. Brazil dominates regional demand through its large domestic coffee industry and growing investments in value-added roasting operations. Colombia is increasingly expanding specialty roasting infrastructure to support export-oriented premium coffee production. Regional manufacturers are focusing on improving roasting efficiency and increasing exports of roasted coffee products rather than green beans. Rising domestic specialty coffee consumption is also supporting market growth across Mexico, Argentina, and Chile.

Middle East & Africa

The Middle East & Africa region is emerging as a promising growth market for coffee roasting equipment. The UAE and Saudi Arabia are witnessing rapid café chain expansion and increasing demand for premium coffee experiences driven by tourism growth and high-income consumer segments. Ethiopia, one of the world’s leading coffee-producing nations, is investing in domestic roasting capabilities to improve export value realization. South Africa is also experiencing growth in specialty coffee culture and independent roasting businesses. Rising urbanization and increasing café penetration across Africa are expected to support long-term regional market expansion.

Key Players in the Coffee Roasters Market

- PROBAT AG

- Bühler Group

- Giesen Coffee Roasters

- Diedrich Manufacturing

- Loring Smart Roast

- Toper

- Scolari Engineering

- Neuhaus Neotec

- Petroncini Impianti

- Genio Roasters

- US Roaster Corp

- Joper Roasters

- Brambati

- Coffee-Tech Engineering

- Ambex