Art and Sculpture Market Size

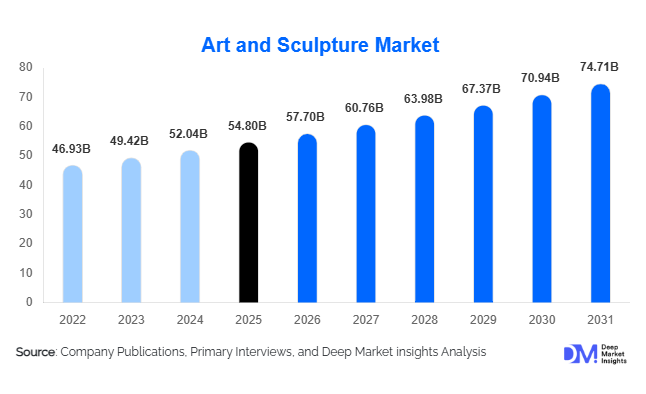

According to Deep Market Insights, the global art and sculpture market size was valued at USD 54.8 billion in 2025 and is projected to grow from USD 57.7 billion in 2026 to reach USD 74.6 billion by 2031, expanding at a CAGR of 5.3% during the forecast period (2026–2031). The art and sculpture market growth is primarily driven by rising global wealth creation, increasing participation from younger collectors, growing demand for alternative investment assets, and expanding public and private investments in cultural infrastructure. The integration of digital sales platforms, blockchain-based authentication systems, and virtual exhibitions has significantly broadened market accessibility, allowing artists, galleries, and auction houses to reach global audiences more efficiently than ever before.

Key Market Insights

- Paintings and fine art remain the largest revenue-generating category, accounting for nearly 46% of total market value due to strong collector demand and institutional acquisitions.

- Private collectors represent the dominant buyer segment, contributing more than half of global art purchases through both primary and secondary market transactions.

- North America dominates the global market, supported by a mature collector ecosystem, leading auction houses, and significant museum procurement activities.

- Asia-Pacific is the fastest-growing regional market, driven by rising high-net-worth populations, increasing cultural investments, and expanding art fairs.

- Online art sales continue to reshape industry dynamics, enabling cross-border transactions and attracting younger collectors through digital platforms.

- Public art installations and smart-city projects are emerging as major demand drivers, creating new revenue opportunities for sculptors, galleries, and commissioning agencies.

Art and Sculpture Market Trends

Growing Adoption of Digital Art Commerce

The global art market is experiencing a profound digital transformation as galleries, auction houses, and artists increasingly leverage online platforms to expand buyer access. Digital exhibitions, virtual galleries, livestream auctions, and AI-powered recommendation systems are reshaping purchasing behavior. Younger collectors are particularly comfortable purchasing artworks online, contributing to growth in both affordable and premium art categories. Blockchain-enabled provenance verification and digital certificates of authenticity are also becoming increasingly important in reducing fraud risks and improving buyer confidence. As technology continues to evolve, digital channels are expected to capture a growing share of global art transactions.

Expansion of Public Art and Cultural Infrastructure

Governments worldwide are investing heavily in cultural infrastructure, museums, urban beautification programs, and public art projects. Large-scale sculptures, interactive installations, and commissioned artworks are becoming central elements of smart-city developments, transportation hubs, public parks, and mixed-use developments. Countries across the Middle East, Asia-Pacific, and Europe are allocating substantial budgets toward cultural tourism and placemaking initiatives. This trend is creating sustained demand for sculptors, artists, public art consultants, and fabrication specialists while broadening the commercial applications of art beyond traditional galleries and museums.

Art and Sculpture Market Drivers

Rising Global High-Net-Worth Individual Population

The increasing number of high-net-worth individuals globally is significantly supporting market expansion. Art is increasingly viewed as a wealth preservation and portfolio diversification asset, particularly during periods of financial market volatility. Wealth growth across North America, China, India, Southeast Asia, and the Middle East is generating strong demand for both established and emerging artists. High-value artwork acquisitions have become an important component of luxury asset portfolios, contributing to sustained market liquidity.

Increasing Demand for Alternative Investments

Investors are increasingly allocating capital toward tangible alternative assets, including art and sculpture. Compared with traditional financial instruments, artworks offer potential long-term appreciation, portfolio diversification benefits, and protection against inflationary pressures. Institutional investors, family offices, and private wealth managers are increasingly recommending art investments as part of broader alternative asset strategies. This shift is strengthening demand across both contemporary and historical art segments.

Art and Sculpture Market Restraints

Authentication and Provenance Challenges

One of the most significant restraints facing the market is the continued prevalence of authenticity concerns, provenance disputes, and art forgery. Buyers increasingly require extensive due diligence, expert verification, and provenance documentation before completing transactions. These requirements can increase transaction costs and extend sales cycles, particularly for high-value artworks. The complexity of ownership histories and cross-border transactions further amplifies authentication challenges.

Market Liquidity and Pricing Volatility

Unlike publicly traded financial assets, artworks often exhibit relatively low liquidity and irregular transaction frequency. Market values can fluctuate significantly based on artist reputation, economic conditions, collector sentiment, and auction performance. The concentration of value among a relatively small number of artists and collectors can create additional volatility, particularly in the contemporary art segment. Such uncertainty may discourage participation from risk-averse investors and new market entrants.

Art and Sculpture Market Opportunities

Corporate and Hospitality Art Procurement

Hotels, luxury resorts, corporate headquarters, commercial real estate projects, and premium retail developments are increasingly incorporating curated art collections into their brand positioning strategies. Developers are commissioning sculptures, murals, and large-scale installations to differentiate properties and enhance visitor experiences. This growing integration of art into commercial environments presents significant opportunities for artists, galleries, and art consultants to secure recurring institutional contracts.

Public Art Programs and Smart City Development

Urbanization and government-led infrastructure development programs are creating substantial opportunities for public art commissions. Smart cities increasingly utilize sculptures and cultural installations to improve public engagement, strengthen local identity, and attract tourism. National cultural initiatives in Saudi Arabia, the UAE, China, India, and Southeast Asia are supporting long-term procurement pipelines for public art projects. These investments provide stable revenue streams that are less dependent on collector demand and auction market cycles.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 54.8 Billion |

| Market Size in 2026 | USD 57.70 Billion |

| Market Size in 2031 | USD 74.71 Billion |

| CAGR | 5.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Paintings and fine art continue to dominate the art and sculpture market, accounting for approximately 46% of global revenue in 2025. The segment benefits from established collector demand, strong museum acquisitions, and consistent auction activity across major international markets. Contemporary art remains particularly attractive to younger investors seeking both cultural value and capital appreciation potential. Sculptures represent the second-largest category, driven by rising demand from public infrastructure projects, luxury hospitality developments, and corporate commissions. Decorative art, photography, digital art, and limited-edition prints are also gaining momentum as more accessible entry points for first-time collectors and emerging investors.

Buyer Type Insights

Private collectors represent the largest buyer segment, accounting for approximately 52% of global market demand. Wealth creation across developed and emerging economies continues to expand the collector base, particularly among younger high-net-worth individuals. Museums and cultural institutions remain important buyers, particularly for historically significant works and heritage preservation projects. Corporate buyers are becoming increasingly influential as organizations use art collections to enhance workplace environments, reinforce brand identity, and improve employee engagement. Real estate developers and hospitality operators are also emerging as major procurement channels for commissioned sculptures and site-specific installations.

Sales Channel Insights

Dealers and galleries remain the leading sales channel, representing approximately 39% of global market value. Their continued dominance stems from artist representation services, advisory expertise, and strong collector relationships. Auction houses continue to play a critical role in high-value transactions and price discovery, particularly for blue-chip artists and rare artworks. Online art platforms are among the fastest-growing channels, supported by improved digital experiences, virtual viewing rooms, transparent pricing structures, and secure payment systems. Direct artist sales are also increasing as creators leverage social media and e-commerce platforms to engage collectors directly.

Price Tier Insights

The affordable art segment, consisting of artworks priced below USD 10,000, accounts for the largest share of transaction volume globally. This category is benefiting from growing participation among younger collectors, digital-native buyers, and first-time investors entering the art market. The mid-market segment remains highly active, supported by established galleries and emerging artist demand. While ultra-high-end artworks generate significant revenue through individual transactions, overall volume remains concentrated within the affordable and mid-priced categories, reflecting broader democratization of art ownership.

End-Use Insights

Residential collections account for approximately 41% of total market demand, supported by private collectors seeking both aesthetic and investment value. Museums and heritage institutions continue to drive demand for culturally significant acquisitions, while commercial offices increasingly utilize artwork to enhance workplace design and employee experience. Hospitality remains one of the fastest-growing end-use sectors as luxury hotels, resorts, and mixed-use developments integrate curated art programs into their guest experience strategies. Public infrastructure projects, educational institutions, and cultural centers are also contributing to sustained demand for sculptures and commissioned artworks.

Explore more data points, trends and opportunities Download Free Sample Report

Art and Sculpture Market Segmentations

By Product Type

- Paintings & Fine Art

- Sculptures

- Decorative & Antique Art

- Photography Art

- Prints & Editions

- Digital Art & NFT-linked Art

- Installation & Public Artworks

By Sales Channel

- Auction Houses

- Galleries

- Art Dealers

- Online Art Marketplaces

- Art Fairs & Exhibitions

- Direct Artist Sales

- Corporate Art Procurement Firms

By Buyer Type

- Private Collectors

- Museums & Cultural Institutions

- Corporate Buyers

- Real Estate Developers

- Hospitality Industry Buyers

- Government & Public Authorities

- Interior Designers & Consultants

By Price Tier

- Ultra-High-End (Above USD 1 Million)

- High-End (USD 100,000 – 1 Million)

- Mid-Market (USD 10,000 – 100,000)

- Affordable Art (Below USD 10,000)

By End Use

- Residential Collections

- Museums & Heritage Institutions

- Commercial Offices

- Hospitality Sector

- Public Infrastructure & Urban Development

- Educational Institutions

- Religious & Cultural Spaces

Regional Insights

North America

North America accounted for approximately 42% of global market revenue in 2025, making it the largest regional market. The United States alone contributes nearly 38% of global demand, supported by a highly developed collector ecosystem, major auction houses, extensive museum networks, and strong private wealth generation. Canada contributes additional demand through institutional acquisitions and growing collector participation. Continued investment in cultural institutions and alternative asset management is expected to support long-term growth across the region.

Europe

Europe represents approximately 30% of global market value, led by the United Kingdom, France, Germany, Italy, and Switzerland. London remains one of the world's most important art trading hubs, while Paris continues to attract significant gallery and museum activity. European demand is supported by strong cultural traditions, established collector communities, and substantial public investment in heritage preservation. The region also benefits from a robust network of art fairs, galleries, and auction houses that facilitate international trade.

Asia-Pacific

Asia-Pacific accounts for approximately 21% of global market demand and is projected to be the fastest-growing region through 2031. China remains the largest market within the region, followed by Japan, South Korea, Hong Kong, Singapore, Australia, and India. Rising disposable incomes, expanding high-net-worth populations, and increasing government support for cultural industries are driving market expansion. International galleries and auction houses are continuing to strengthen their presence across major Asian cities to capitalize on growing collector demand.

Latin America

Latin America contributes approximately 3% of global demand, with Brazil, Mexico, Argentina, Chile, and Colombia representing the largest markets. Regional growth is supported by increasing participation in international art fairs, expanding private collections, and growing cultural tourism initiatives. While the market remains relatively small compared to North America and Europe, long-term growth prospects remain positive as economic development expands collector participation.

Middle East & Africa

The Middle East and Africa account for approximately 4% of global market revenue. The UAE, Saudi Arabia, and Qatar are emerging as major art investment hubs through museum construction, cultural districts, and international exhibition programs. Saudi Arabia's Vision 2031 initiative is expected to drive significant future demand for public art and cultural infrastructure. South Africa remains the largest African market, while Nigeria, Kenya, and Morocco are developing rapidly as centers for contemporary African art.

Key Players in the Art and Sculpture Market

- Christie's

- Sotheby's

- Phillips

- Bonhams

- China Guardian Auctions

- Poly Auction

- Heritage Auctions

- Ketterer Kunst

- Artcurial

- Dorotheum

- Gagosian

- Hauser & Wirth

- David Zwirner

- Pace Gallery

- White Cube