Weightlifting Shoes Market Size

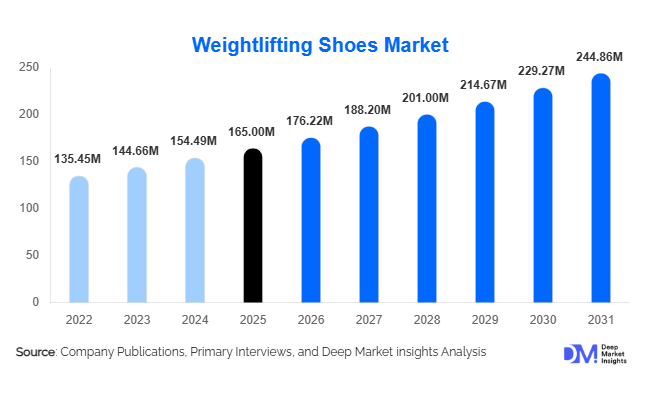

According to Deep Market Insights, the global weightlifting shoes market size was valued at USD 165 million in 2025 and is projected to grow from USD 176.22 million in 2026 to reach USD 244.86 million by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The weightlifting shoes market growth is primarily driven by the rising adoption of strength training worldwide, increasing participation in Olympic weightlifting and powerlifting competitions, growing popularity of CrossFit and functional fitness programs, and greater awareness regarding injury prevention and lifting biomechanics. As resistance training becomes a core component of athletic performance, rehabilitation, and general fitness regimens, demand for specialized footwear designed to improve stability, posture, and force transfer continues to increase across both professional and recreational user groups.

Key Market Insights

- Olympic weightlifting shoes account for the largest product segment, representing approximately 41% of global market revenue due to their widespread use among competitive and recreational lifters.

- Online retail channels dominate global sales, contributing nearly 58% of market revenue as consumers increasingly purchase specialized footwear through direct-to-consumer and e-commerce platforms.

- North America remains the largest regional market, accounting for approximately 36% of global demand, supported by strong gym penetration and a mature strength training ecosystem.

- Asia-Pacific is the fastest-growing region, driven by expanding fitness memberships, rising disposable incomes, and increasing adoption of strength sports across China and India.

- Premium weightlifting footwear is witnessing significant growth, supported by demand for advanced materials, improved durability, customized fit, and enhanced lifting performance.

- Technological innovation, including lightweight TPU heel systems, engineered knit uppers, custom orthotic integration, and sustainable materials, is reshaping product development across the industry.

Weightlifting Shoes Market Trends

Expansion of Functional Fitness and CrossFit Training

The global expansion of CrossFit affiliates, functional fitness centers, and strength-focused gyms has significantly increased demand for specialized weightlifting footwear. Athletes participating in Olympic lifts, squats, cleans, and snatches increasingly recognize the performance benefits of elevated-heel lifting shoes. Manufacturers are responding by developing hybrid models that combine lifting stability with flexibility suitable for multidimensional training environments. As strength-based fitness continues gaining mainstream acceptance, footwear designed specifically for lifting activities is becoming a standard component of gym equipment rather than a niche product category.

Premiumization and Customization of Weightlifting Footwear

Consumers are increasingly seeking premium footwear solutions that provide enhanced comfort, biomechanics, and durability. Brands are investing in customizable heel heights, advanced locking systems, precision fit technologies, and lightweight composite materials. Digital foot scanning, personalized insoles, and direct-to-consumer customization programs are becoming more common among leading manufacturers. Sustainability initiatives, including recycled materials and environmentally responsible production processes, are also influencing purchasing decisions among younger fitness enthusiasts.

Weightlifting Shoes Market Drivers

Growing Global Participation in Strength Training

Strength training has evolved from a niche athletic activity into a mainstream fitness practice embraced by recreational gym users, athletes, and healthcare professionals. Health organizations increasingly recommend resistance training for musculoskeletal health, metabolic improvement, and injury prevention. As participation expands globally, demand for specialized equipment such as weightlifting shoes continues to rise. Fitness chains, sports performance centers, and independent gyms are further contributing to market growth by promoting proper lifting techniques and equipment usage.

Rising Demand for Athletic Performance Optimization

Professional athletes and serious fitness enthusiasts increasingly seek performance advantages through specialized equipment. Weightlifting shoes provide improved stability, enhanced squat depth, superior force transmission, and reduced injury risk during compound lifts. Sports organizations, collegiate athletic programs, and Olympic training facilities continue integrating specialized lifting footwear into athlete development programs. The growing emphasis on measurable athletic performance improvements is creating sustained demand across professional and amateur sports sectors.

Weightlifting Shoes Market Restraints

Premium Pricing Limits Mass-Market Penetration

Weightlifting shoes typically command higher prices than conventional athletic footwear due to specialized design requirements and lower production volumes. Professional-grade models often exceed USD 150–250 per pair, creating affordability challenges for casual gym users. Many consumers continue to use general-purpose training shoes for lifting activities, limiting penetration within broader fitness markets. Economic uncertainty and discretionary spending constraints can further influence purchasing decisions in price-sensitive regions.

Limited Multi-Purpose Functionality

Unlike running shoes or cross-training footwear, weightlifting shoes are designed specifically for strength-training applications. Their rigid construction and elevated heels limit versatility for other athletic activities, causing some consumers to hesitate before making dedicated footwear purchases. Manufacturers continue working to develop hybrid designs that improve versatility while maintaining lifting performance, but balancing these characteristics remains a key industry challenge.

Weightlifting Shoes Market Opportunities

Emerging Demand Across Developing Fitness Markets

Rapid growth in fitness infrastructure across Asia-Pacific, Latin America, and the Middle East presents substantial opportunities for manufacturers. Countries such as India, China, Brazil, Saudi Arabia, and Indonesia are witnessing increasing gym memberships, rising disposable incomes, and growing participation in strength sports. Local manufacturing initiatives and expanding distribution networks can help brands capture demand in these underpenetrated markets while reducing logistics costs and improving product accessibility.

Advanced Material Technologies and Personalized Products

The integration of advanced polymers, lightweight composite materials, engineered knit uppers, and customized fitting technologies offers significant growth potential. Consumers increasingly value footwear tailored to their biomechanics, training styles, and performance goals. Brands investing in digital customization platforms, 3D foot scanning, and personalized insoles can achieve stronger differentiation while commanding premium pricing. The continued evolution of sports science and biomechanics research is expected to support innovation-led growth throughout the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 165 Million |

| Market Size in 2026 | USD 176.22 Million |

| Market Size in 2031 | USD 244.86 Million |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Olympic weightlifting shoes dominate the global market, accounting for approximately 41% of revenue in 2025. These products are widely adopted by competitive weightlifters, CrossFit athletes, and strength coaches due to their elevated heels and superior stability characteristics. Powerlifting shoes represent a significant secondary segment, particularly among athletes prioritizing deadlift and squat performance. Cross-training weightlifting shoes are experiencing rapid growth as consumers seek versatile products suitable for both strength training and functional fitness activities. General strength training footwear continues to attract beginner and recreational users looking for affordable entry-level options within the category.

Heel Height Insights

Medium heel shoes with elevations between 15 mm and 20 mm represent the largest segment, accounting for approximately 47% of global revenue. These products offer an optimal balance between mobility enhancement and lifting stability, making them suitable for a broad range of users. High-heel models are preferred among competitive Olympic lifters requiring maximum squat depth, while low-heel options continue to attract powerlifters and consumers favoring a more natural lifting position.

Material Insights

Synthetic leather remains the leading upper material segment, accounting for more than 52% of market revenue due to its durability, affordability, and resistance to wear. Engineered mesh and knit materials are gaining popularity as manufacturers focus on weight reduction and breathability. Genuine leather products maintain demand within premium market segments, while hybrid composite materials continue emerging as brands seek to combine performance, comfort, and sustainability objectives.

Distribution Channel Insights

Online retail channels account for approximately 58% of global sales, supported by direct-to-consumer business models, specialized e-commerce platforms, and enhanced product visualization technologies. Brand-owned websites continue gaining importance as manufacturers seek higher margins and stronger customer engagement. Specialty sporting goods stores remain influential, particularly for premium products requiring fit assessment and in-person evaluation. Fitness centers and sports academies also contribute to market demand through institutional purchases and on-site retail programs.

End-User Insights

Recreational gym members represent the largest end-user segment, accounting for approximately 34% of global demand. Growing awareness regarding proper lifting mechanics and injury prevention has increased footwear adoption among non-competitive users. Professional weightlifters and powerlifters continue generating strong demand for premium products, while CrossFit athletes represent one of the fastest-growing user groups. Sports academies, collegiate athletic programs, and strength and conditioning facilities are increasingly incorporating specialized footwear into athlete training programs, further supporting market expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Weightlifting Shoes Market Segmentations

By Product Type

- Olympic Weightlifting Shoes

- Powerlifting Shoes

- Cross-Training Weightlifting Shoes

- General Strength Training Shoes

By Heel Height

- Low Heel (<15 mm)

- Medium Heel (15–20 mm)

- High Heel (>20 mm)

By Upper Material

- Synthetic Leather

- Mesh & Knit Materials

- Genuine Leather

- Composite/Hybrid Materials

By Distribution Channel

- Online Retail

- Sporting Goods Stores

- Specialty Fitness Stores

- Brand-Owned Stores

- Gym-Based Retail Sales

By End User

- Professional Weightlifters

- Powerlifters

- CrossFit Athletes

- Recreational Gym Members

- Strength & Conditioning Programs

- Sports Academies & Training Centers

Regional Insights

North America

North America accounted for approximately 36% of global market revenue in 2025, making it the largest regional market. The United States drives regional demand through widespread gym memberships, strong participation in CrossFit and strength sports, and a mature sports performance industry. Canada also contributes steady growth through expanding fitness participation and increasing awareness of specialized athletic footwear.

Europe

Europe represents approximately 27% of global demand, led by Germany, the United Kingdom, France, Italy, and Spain. The region benefits from established weightlifting federations, growing sports performance programs, and increasing consumer spending on premium athletic equipment. Germany remains the largest European market due to strong participation in Olympic lifting and strength training activities.

Asia-Pacific

Asia-Pacific accounts for approximately 29% of global market revenue and is expected to record the highest growth rate during the forecast period. China dominates regional demand through its large fitness population and manufacturing capabilities, while India is emerging as the fastest-growing country market. Rising disposable incomes, expanding gym infrastructure, and increasing participation in strength-focused fitness programs continue supporting regional growth.

Latin America

Latin America contributes approximately 4%–5% of global demand, with Brazil representing the largest market. Growing fitness awareness, increasing commercial gym penetration, and expanding participation in strength sports are driving demand for specialized footwear. Mexico and Argentina are also emerging as important markets for international footwear brands.

Middle East & Africa

The Middle East and Africa account for approximately 4%–5% of global market revenue. Saudi Arabia and the United Arab Emirates are witnessing rapid growth due to government-supported fitness initiatives and increasing investment in sports infrastructure. South Africa remains the largest market within Africa, supported by established athletic communities and growing gym memberships.