Weight Loss Diet Market Size

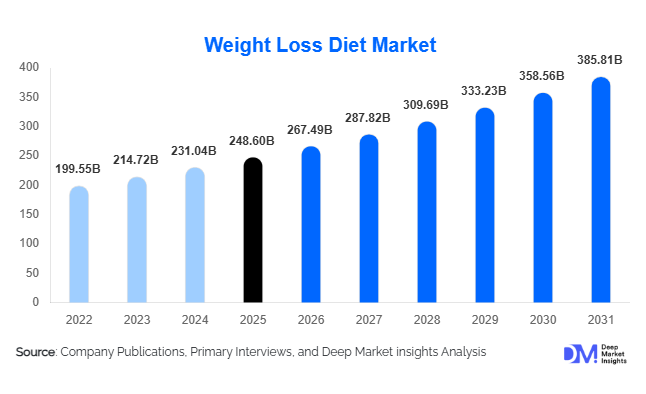

According to Deep Market Insights, the global weight loss diet market size was valued at USD 248.6 billion in 2025 and is projected to grow from USD 267.49 billion in 2026 to reach USD 385.81 billion by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The market is benefiting from rising obesity prevalence, increasing consumer focus on preventive healthcare, growing adoption of personalized nutrition solutions, and expanding demand for scientifically formulated weight management programs. The integration of digital health technologies, mobile nutrition applications, wearable health monitoring devices, and AI-driven dietary recommendations is further accelerating market expansion across developed and emerging economies.

Key Market Insights

- Personalized nutrition programs are becoming mainstream, supported by advances in genomics, microbiome analysis, and artificial intelligence-based dietary recommendations.

- Intermittent fasting and low-carbohydrate diet programs continue gaining global acceptance, particularly among consumers seeking sustainable and non-pharmaceutical weight management solutions.

- North America dominates the global market, accounting for approximately 38.5% of global revenue in 2025 due to high obesity prevalence and strong consumer spending on wellness products.

- Asia-Pacific represents the fastest-growing regional market, supported by increasing urbanization, rising disposable incomes, and growing awareness of lifestyle-related diseases.

- Digital weight management platforms and subscription-based nutrition services are rapidly expanding, reshaping traditional diet program delivery models.

- Healthcare providers and insurers are increasingly incorporating weight management programs into preventive healthcare initiatives to reduce long-term treatment costs associated with obesity and chronic diseases.

Weight Loss Diet Market Trends

Personalized Nutrition and Precision Diet Programs Gaining Momentum

One of the most significant trends transforming the weight loss diet market is the growing adoption of personalized nutrition. Consumers are increasingly moving away from generic diet plans toward customized solutions designed around individual metabolic profiles, genetic predispositions, lifestyle habits, and health goals. Companies are leveraging DNA testing, microbiome sequencing, and AI-powered analytics to develop personalized meal plans that improve adherence and outcomes. The trend is particularly strong among premium consumers in North America, Europe, Japan, and South Korea. Subscription-based personalized nutrition platforms are experiencing double-digit growth rates as consumers seek evidence-based approaches to weight management.

Digital Health Integration Reshaping Weight Management

Digital transformation continues to redefine the weight loss diet ecosystem. Mobile applications, wearable devices, telehealth nutrition counseling, and AI-powered coaching platforms are becoming integral components of weight management programs. Consumers increasingly expect real-time calorie tracking, personalized recommendations, behavioral coaching, and progress monitoring through connected platforms. Integration between smartwatches, fitness trackers, and nutrition applications is improving user engagement and retention rates. The growing use of predictive analytics and machine learning is enabling providers to deliver adaptive diet plans that evolve according to user behavior and health outcomes, improving long-term success rates.

Weight Loss Diet Market Drivers

Growing Global Obesity and Overweight Population

The increasing prevalence of obesity remains the primary growth driver for the weight loss diet market. Rising sedentary lifestyles, unhealthy eating habits, urbanization, and increasing consumption of processed foods have significantly increased obesity rates across developed and emerging economies. Governments and healthcare systems are prioritizing obesity prevention due to its association with diabetes, cardiovascular diseases, hypertension, and certain cancers. As a result, consumers are actively investing in structured diet programs, meal replacement solutions, and weight management services.

Rising Preventive Healthcare Awareness

Consumers are increasingly viewing weight management as an essential component of preventive healthcare rather than merely an aesthetic objective. Growing awareness regarding the long-term health risks associated with excess weight is encouraging adoption of medically supervised diet programs and nutritional interventions. Employers, insurance providers, and healthcare organizations are also promoting preventive wellness initiatives, further expanding market demand.

Weight Loss Diet Market Restraints

Low Long-Term Consumer Adherence Rates

Despite strong demand, many consumers struggle to maintain long-term adherence to structured weight loss diets. High dropout rates, behavioral challenges, unrealistic expectations, and difficulties maintaining lifestyle modifications limit sustained program effectiveness. This remains a significant challenge for market participants seeking long-term customer retention.

Regulatory Scrutiny and Product Credibility Concerns

The market faces ongoing regulatory oversight regarding health claims, supplement efficacy, labeling requirements, and consumer protection. Products or programs making unsupported weight loss claims may face regulatory actions, negatively impacting consumer confidence. Increasing demand for scientific validation is forcing manufacturers and service providers to invest heavily in clinical research and compliance programs.

Weight Loss Diet Market Opportunities

Expansion of Corporate Wellness Programs

Organizations worldwide are increasingly implementing employee wellness initiatives focused on weight management, nutrition education, and lifestyle improvement. Corporate wellness programs represent a significant growth opportunity for providers offering scalable digital nutrition platforms, personalized coaching, and subscription-based dietary services. Employers are recognizing that healthier employees contribute to improved productivity, lower absenteeism, and reduced healthcare expenditures.

AI-Driven Nutrition Platforms

Artificial intelligence is creating substantial opportunities across the weight loss diet market. AI-powered applications can analyze dietary patterns, health metrics, behavioral data, and activity levels to generate highly personalized recommendations. Companies investing in predictive nutrition technologies are expected to gain competitive advantages through enhanced customer outcomes and engagement.

Emerging Market Penetration

Rapid urbanization and increasing disposable incomes across India, China, Indonesia, Brazil, Mexico, Saudi Arabia, and Southeast Asia are creating substantial demand for affordable weight management solutions. Rising awareness of obesity-related diseases combined with expanding digital healthcare infrastructure presents significant opportunities for both established companies and new market entrants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 248.6 Billion |

| Market Size in 2026 | USD 267.49 Billion |

| Market Size in 2031 | USD 385.81 Billion |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Diet Program Type Insights

Macronutrient-specific diets represent the largest segment of the weight loss diet market, accounting for approximately 31.8% of global revenue in 2025. Within this category, ketogenic and low-carbohydrate diets have achieved widespread adoption due to their perceived effectiveness in delivering rapid weight reduction and improved metabolic outcomes. Intermittent fasting programs account for nearly 18.4% market share and represent one of the fastest-growing segments globally. Personalized nutrition programs, although currently accounting for approximately 11.6% of the market, are expected to record the highest growth rates through 2031 as consumers increasingly seek individualized weight management solutions.

Product Offering Insights

Meal replacement products remain the dominant product category, representing approximately 34.2% of market revenue in 2025. Consumers increasingly prefer convenient and portion-controlled solutions that simplify calorie management. Weight loss functional foods account for nearly 27.5% of global demand, supported by growing consumer preference for healthier snacks and ready-to-eat meals. Functional beverages and protein-based drinks continue to experience strong demand among fitness-focused consumers seeking nutritional support alongside weight management objectives.

Distribution Channel Insights

E-commerce has emerged as the largest distribution channel, accounting for approximately 36.7% of global market revenue. Consumers increasingly prefer online platforms due to convenience, product variety, subscription options, and personalized recommendations. Direct-to-consumer channels are also expanding rapidly as brands strengthen digital engagement strategies and leverage consumer data analytics to improve retention and customer lifetime value.

Consumer Type Insights

Adults aged 18–44 years represent the largest consumer group, contributing approximately 46.5% of total market demand. This demographic exhibits high awareness regarding physical appearance, fitness, and preventive healthcare. Middle-aged consumers represent another significant segment due to growing concerns regarding obesity-related health conditions and age-related metabolic changes. Senior consumers increasingly participate in medically supervised weight management programs focused on improving overall health outcomes.

End-Use Insights

Individual consumers remain the largest end-use segment, accounting for approximately 61.3% of global market revenue. However, healthcare providers and clinics are emerging as the fastest-growing end-user category due to increasing integration of nutritional therapy into chronic disease management programs. Corporate wellness programs are also expanding rapidly, driven by employer investments in workforce health optimization and preventive healthcare initiatives.

Explore more data points, trends and opportunities Download Free Sample Report

Weight Loss Diet Market Segmentations

By Diet Program Type

- Calorie-Restricted Diets

- Macronutrient-Specific Diets

- Functional & Therapeutic Diets

- Plant-Based Weight Loss Diets

- Intermittent Fasting Programs

- Personalized Nutrition Programs

By Product Offering

- Meal Replacement Products

- Weight Loss Functional Foods

- Weight Management Beverages

- Weight Loss Supplements

By Consumer Type

- Adults (18–44 Years)

- Middle-Aged Consumers (45–64 Years)

- Senior Consumers (65+ Years)

- Adolescents and Youth

By Distribution Channel

- E-Commerce Platforms

- Retail Pharmacies

- Supermarkets & Hypermarkets

- Specialty Nutrition Stores

- Direct-to-Consumer (DTC)

By End User

- Individual Consumers

- Corporate Wellness Programs

- Healthcare Providers & Clinics

- Fitness Centers & Health Clubs

- Insurance & Preventive Healthcare Programs

Regional Insights

North America

North America accounted for approximately 38.5% of global market revenue in 2025, making it the largest regional market. The United States represents over 80% of regional demand, driven by high obesity prevalence, advanced healthcare infrastructure, strong consumer spending on wellness products, and widespread adoption of digital health technologies. Canada continues to experience steady growth supported by government-led public health initiatives and increasing consumer awareness regarding nutrition and preventive healthcare.

Europe

Europe accounted for approximately 28.2% of global market revenue in 2025. Germany, the United Kingdom, France, Italy, and Spain represent the region's largest markets. Growing demand for plant-based diets, preventive healthcare programs, and scientifically validated nutritional interventions is driving regional growth. Regulatory emphasis on healthier lifestyles and obesity prevention continues supporting market expansion.

Asia-Pacific

Asia-Pacific accounted for nearly 22.7% of global revenue and represents the fastest-growing regional market, expected to expand at a CAGR exceeding 9.5% through 2031. China leads regional demand due to rising obesity rates and growing middle-class spending on wellness products. India is emerging as one of the fastest-growing national markets, supported by increasing urbanization, digital health adoption, and rising awareness of lifestyle diseases. Japan, South Korea, and Australia continue to demonstrate strong demand for premium and personalized nutrition programs.

Latin America

Brazil, Mexico, Argentina, and Chile are leading markets within Latin America. Rising obesity prevalence, expanding middle-class populations, and increasing healthcare awareness are contributing to market growth. Brazil accounts for the largest share of regional demand, supported by strong consumer engagement in fitness and wellness activities.

Middle East & Africa

The Middle East and Africa region is witnessing increasing demand for structured weight management solutions. Saudi Arabia and the UAE lead regional growth due to high obesity rates, rising healthcare expenditures, and growing adoption of digital health technologies. South Africa remains the largest African market, benefiting from increasing consumer awareness regarding preventive health and wellness.

Key Players in the Weight Loss Diet Market

- WW International (WeightWatchers)

- Herbalife Ltd.

- Nestlé Health Science

- Nutrisystem

- Noom Inc.

- Medifast Inc.

- Jenny Craig

- Huel Ltd.

- The Simply Good Foods Company

- Glanbia Nutritionals

- Abbott Nutrition

- Amway Corporation

- Nature's Sunshine Products

- Shaklee Corporation

- Profile Plan