Tactical Gear Market Size

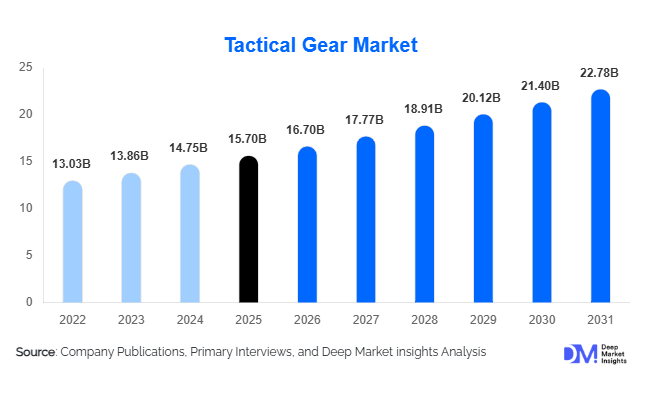

According to Deep Market Insights, the global tactical gear market size was valued at USD 15.7 billion in 2025 and is projected to grow from USD 16.70 billion in 2026 to reach USD 22.78 billion by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The tactical gear market growth is primarily driven by increasing military modernization programs, rising geopolitical tensions, growing law enforcement equipment upgrades, and expanding demand for advanced protective solutions across defense, homeland security, and private security sectors. Continuous innovations in ballistic protection materials, wearable technologies, and integrated communication systems are further supporting market expansion. Governments across developed and emerging economies are prioritizing soldier survivability and operational readiness, resulting in sustained procurement of next-generation tactical equipment.

Key Market Insights

- Military and defense organizations account for the largest share of tactical gear demand, representing approximately 42% of global market revenue in 2025.

- Protective equipment remains the dominant product segment, accounting for nearly 31% of the global tactical gear market.

- North America dominates the market, supported by extensive defense spending and large-scale soldier modernization programs.

- Asia-Pacific is the fastest-growing region, driven by rising defense budgets in China, India, South Korea, and Australia.

- Smart tactical systems and wearable soldier technologies are becoming major procurement priorities among military and law enforcement agencies.

- Advanced ballistic materials such as UHMWPE and next-generation aramid fibers are transforming equipment performance by reducing weight while improving protection levels.

Tactical Gear Market Trends

Smart Soldier Systems Driving Equipment Innovation

Military organizations worldwide are increasingly investing in integrated soldier modernization programs that combine tactical gear with advanced digital technologies. Smart helmets, wearable communication systems, biometric monitoring devices, augmented reality displays, and GPS-enabled battlefield management systems are becoming integral components of modern tactical equipment. These technologies improve situational awareness, command coordination, and operational effectiveness while enhancing soldier safety. Defense agencies are increasingly procuring complete soldier systems rather than standalone equipment, creating opportunities for manufacturers that can offer integrated and interoperable solutions. The convergence of tactical gear and digital technologies is expected to remain one of the most influential trends shaping the market through 2031.

Lightweight Ballistic Protection Becoming a Procurement Priority

Modern armed forces and law enforcement agencies are prioritizing lightweight protection systems that improve mobility without compromising survivability. Advanced materials including ultra-high molecular weight polyethylene (UHMWPE), ceramic composites, and enhanced aramid fibers, are replacing traditional heavy armor systems. These innovations enable soldiers and tactical personnel to operate effectively in demanding environments while reducing fatigue and improving mission endurance. Manufacturers are increasingly focused on developing modular armor systems that can be customized according to threat levels and mission requirements. This trend is accelerating replacement cycles and driving premium product adoption globally.

Tactical Gear Market Drivers

Growing Global Defense Expenditure

Increasing geopolitical tensions, border security concerns, and military modernization initiatives continue to drive global defense spending. Countries including the United States, China, India, Poland, Saudi Arabia, and Australia are significantly expanding defense budgets to strengthen military preparedness. Tactical gear procurement remains a critical component of these investments, particularly in body armor, helmets, communication systems, and combat apparel. Governments are prioritizing soldier survivability programs, resulting in long-term procurement contracts and stable demand for advanced tactical equipment. Rising defense allocations across NATO countries and Asia-Pacific nations are expected to provide sustained growth opportunities for market participants.

Advancements in Protective Materials and Equipment Design

Material innovation is transforming tactical gear performance across multiple product categories. Manufacturers are leveraging advanced ballistic fibers, composite materials, lightweight ceramics, and smart textiles to develop products that offer improved protection, durability, and comfort. These innovations are enhancing operational effectiveness while reducing equipment weight, making tactical gear more attractive to military, law enforcement, and private security users. Continuous investment in research and development is enabling manufacturers to differentiate products and command premium pricing in high-performance equipment categories.

Tactical Gear Market Restraints

High Cost of Advanced Tactical Systems

Modern tactical equipment incorporating advanced materials and integrated technologies often carries significantly higher acquisition costs than conventional alternatives. Premium body armor systems, smart helmets, wearable communication platforms, and specialized protective gear require substantial investment, creating budget constraints for smaller military organizations and law enforcement agencies. Cost pressures are particularly evident in emerging markets where procurement budgets may be limited despite increasing security requirements. The high cost of replacement and maintenance further adds to total ownership expenses.

Export Regulations and Procurement Compliance Requirements

Tactical gear products are subject to stringent export controls, military standards, and procurement regulations across many jurisdictions. Manufacturers seeking international expansion must navigate complex licensing requirements, certification processes, and government procurement procedures. Regulatory compliance can increase operational costs and extend sales cycles, particularly for advanced ballistic protection systems and military-grade communication equipment. These barriers can slow market penetration and limit opportunities for smaller manufacturers seeking global expansion.

Tactical Gear Market Opportunities

Expansion of Soldier Modernization Programs

Governments worldwide are implementing comprehensive soldier modernization initiatives designed to improve battlefield effectiveness, mobility, and survivability. Programs in North America, Europe, Asia-Pacific, and the Middle East are creating significant demand for advanced tactical equipment, including body armor, helmets, integrated communications, and wearable technologies. Suppliers capable of delivering complete soldier systems are well-positioned to secure long-term procurement contracts and expand market share. The growing emphasis on digitized warfare and network-centric operations further strengthens this opportunity.

Rising Demand from Private Security and Civilian Users

The tactical gear market is increasingly benefiting from demand beyond traditional military and law enforcement customers. Private security contractors, critical infrastructure operators, emergency response organizations, and outdoor enthusiasts are driving demand for professional-grade tactical equipment. Growing awareness of personal preparedness, survival training, and adventure activities has expanded the civilian customer base. E-commerce platforms are enabling manufacturers to access these emerging customer segments directly, creating new revenue streams and reducing reliance on government procurement cycles.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15.7 Billion |

| Market Size in 2026 | USD 16.70 Billion |

| Market Size in 2031 | USD 22.78 Billion |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Protective equipment dominates the tactical gear market, accounting for approximately 31% of global revenue in 2025. Body armor systems, ballistic helmets, tactical vests, and protective eyewear represent essential equipment for military and law enforcement personnel operating in high-risk environments. Tactical apparel constitutes another major segment, supported by growing demand for flame-resistant uniforms, camouflage clothing, and weather-resistant combat apparel. Load-carrying equipment, including backpacks, chest rigs, and modular pouch systems, continues to gain popularity due to increasing requirements for mobility and mission flexibility. Tactical communication devices and navigation systems are emerging as high-growth product categories as digital battlefield integration becomes a strategic priority for defense organizations.

End User Insights

Military and defense forces remain the largest end-user segment, accounting for approximately 42% of market demand. Ongoing modernization programs and defense procurement initiatives continue to support strong equipment purchases globally. Law enforcement agencies represent the second-largest segment, driven by increasing investments in officer safety, riot control, and tactical response capabilities. Homeland security organizations are expanding procurement of advanced tactical equipment to strengthen border security and critical infrastructure protection. Private security contractors are emerging as a high-growth segment, particularly in regions experiencing rising demand for commercial security services. Outdoor enthusiasts and survival-focused consumers are also contributing to market growth through increased adoption of tactical apparel, backpacks, and accessories.

Material Type Insights

Ultra-high molecular weight polyethylene (UHMWPE) has emerged as one of the most important material categories in the tactical gear market, accounting for approximately 24% of material-related demand. The material offers superior strength-to-weight performance and is widely used in body armor and ballistic helmets. Aramid fibers continue to hold a significant share of the market due to their proven ballistic protection characteristics and widespread military adoption. Composite materials are gaining traction as manufacturers seek to improve durability and reduce equipment weight. Smart textiles represent an emerging segment, enabling integration of biometric sensors, communication systems, and environmental monitoring capabilities into tactical apparel and protective equipment.

Distribution Channel Insights

Direct government procurement remains the dominant distribution channel, accounting for nearly 48% of market revenue. Defense ministries, military agencies, and law enforcement organizations typically procure tactical equipment through long-term contracts and centralized purchasing programs. Defense contractors and system integrators play a critical role in supplying integrated tactical solutions and managing large procurement projects. Specialty tactical retailers continue to serve law enforcement professionals, private security personnel, and civilian users. E-commerce platforms are experiencing rapid growth as manufacturers increasingly leverage digital channels to reach commercial and consumer markets. Online distribution is particularly important for tactical apparel, accessories, and outdoor-focused equipment categories.

Protection Level Insights

Hard armor systems represent the leading protection category, accounting for approximately 38% of global market demand. Increasing concerns regarding high-caliber ballistic threats and battlefield survivability are driving adoption among military and specialized law enforcement units. Soft armor systems continue to be widely used by police departments and security personnel due to their lightweight construction and flexibility. Hybrid armor solutions are gaining market share as organizations seek to balance protection, mobility, and wearer comfort. The trend toward modular protection systems is enabling users to customize armor configurations based on mission-specific threat assessments.

Explore more data points, trends and opportunities Download Free Sample Report

Tactical Gear Market Segmentations

By Product Type

- Protective Equipment

- Tactical Apparel

- Tactical Footwear

- Load-Carrying Equipment

- Tactical Accessories

- Communication & Navigation Equipment

- Weapon Support Accessories

By End User

- Military & Defense Forces

- Law Enforcement Agencies

- Homeland Security Agencies

- Private Security Contractors

- Fire & Rescue Services

- Outdoor & Survival Enthusiasts

- Industrial Hazard Response Teams

By Material Type

- Aramid Fiber (Kevlar)

- Ultra-High Molecular Weight Polyethylene (UHMWPE)

- Nylon

- Polyester

- Cotton Blends

- Composite Materials

- Smart Textile Materials

By Distribution Channel

- Direct Government Procurement

- Defense Contractors & Integrators

- Specialty Tactical Stores

- E-commerce Platforms

- Outdoor Equipment Retailers

By Protection Level

- Soft Armor Systems

- Hard Armor Systems

- Hybrid Armor Systems

Regional Insights

North America

North America accounted for approximately 37% of global tactical gear market revenue in 2026, making it the largest regional market worldwide. The United States alone contributes nearly 31% of global demand, supported by the world's highest defense expenditure and continuous investments in soldier modernization programs. The U.S. Department of Defense remains a major purchaser of advanced body armor systems, ballistic helmets, tactical communication devices, load-bearing equipment, and next-generation wearable technologies. Growing emphasis on network-centric warfare, integrated battlefield management systems, and enhanced soldier survivability continues to support procurement of premium tactical gear.

Canada contributes significantly through military capability enhancement programs, border security investments, and modernization initiatives undertaken by law enforcement agencies. The region also benefits from the presence of major tactical gear manufacturers, advanced defense R&D capabilities, and established procurement frameworks. Rising investments in homeland security, counterterrorism preparedness, and special operations equipment continue to strengthen demand across both military and civilian security sectors. The increasing adoption of smart tactical equipment and lightweight ballistic protection systems is expected to further reinforce North America's leadership position throughout the forecast period.

Europe

Europe represented approximately 26% of global tactical gear market revenue in 2026. Demand is concentrated across Germany, France, the United Kingdom, Poland, Italy, and several Nordic countries. Regional growth is being driven by rising defense budgets, military readiness programs, and increasing commitments by NATO member states to strengthen combat preparedness and operational capabilities. The geopolitical environment in Eastern Europe has accelerated procurement of tactical protective equipment, communications systems, and soldier modernization technologies across the region.

Germany, France, and the United Kingdom continue to invest heavily in advanced soldier systems and next-generation battlefield equipment. Poland has emerged as one of the fastest-growing tactical gear markets globally due to large-scale military expansion programs, increased troop deployments, and significant procurement of protective equipment and combat systems. In addition, growing investments in border security, counter-drone capabilities, and rapid-response units are supporting tactical gear demand. European manufacturers are also increasingly focused on lightweight armor technologies, sustainable military textiles, and integrated soldier platforms, further contributing to market growth.

Asia-Pacific

Asia-Pacific accounted for approximately 24% of global tactical gear market demand in 2026 and is projected to register the fastest growth through 2031. Regional expansion is primarily driven by rising geopolitical tensions, military modernization initiatives, territorial security concerns, and growing defense expenditure across major economies. China remains the largest market within the region due to substantial investments in military modernization, indigenous defense manufacturing, and advanced soldier systems.

India is expected to be one of the fastest-growing country markets, supported by defense modernization initiatives, increasing procurement of domestically manufactured tactical equipment, and government programs aimed at strengthening military self-reliance. South Korea and Japan continue to invest in advanced protective systems, communication technologies, and special operations equipment in response to evolving regional security requirements. Australia is expanding defense spending through modernization programs focused on enhancing combat readiness and force protection. The region's growth is further supported by expanding local manufacturing capabilities, increasing adoption of lightweight ballistic materials, and rising demand for technologically advanced soldier equipment.

Latin America

Latin America accounted for approximately 5% of global tactical gear market revenue in 2026. Brazil, Mexico, Colombia, and Chile represent the primary demand centers across the region. Although defense budgets remain comparatively lower than those of North America and Europe, growing concerns regarding organized crime, border security, narcotics trafficking, and civil unrest are creating sustained demand for tactical protective equipment and law enforcement gear.

Brazil remains the largest regional market due to military modernization efforts, border monitoring initiatives, and public security investments. Mexico continues to expand procurement of tactical equipment for law enforcement agencies and specialized security units combating organized crime. Colombia's long-standing focus on counterinsurgency and security operations supports demand for advanced tactical apparel, communication systems, and ballistic protection equipment. Increasing government investments in homeland security modernization and public safety programs are expected to support steady market expansion across Latin America over the forecast period.

Middle East & Africa

The Middle East & Africa represented approximately 8% of global tactical gear market demand in 2026. Saudi Arabia, the United Arab Emirates, Israel, South Africa, and Qatar are among the region's largest consumers of tactical equipment. Demand is primarily driven by defense modernization programs, counterterrorism operations, border security requirements, and investments aimed at enhancing military readiness.

Saudi Arabia and the UAE continue to invest heavily in advanced military equipment and soldier protection technologies as part of broader defense transformation initiatives. Israel remains a leading adopter of advanced tactical gear due to its strong focus on force protection, battlefield innovation, and operational readiness. In Africa, South Africa serves as a key market supported by military modernization efforts and law enforcement requirements. The region is also witnessing increased investment in homeland security infrastructure, critical asset protection, and special operations capabilities. Growing procurement of lightweight armor systems, tactical communication devices, and integrated soldier solutions is expected to support long-term market growth across both Middle Eastern and African countries.

Key Players in the Tactical Gear Market

- 3M Company

- Honeywell International Inc.

- BAE Systems plc

- Safariland LLC

- DuPont de Nemours, Inc.

- Point Blank Enterprises

- Avon Protection plc

- Elbit Systems Ltd.

- ArmorSource LLC

- Revision Military

- TYR Tactical

- Crye Precision

- Condor Outdoor Products

- Survitec Group

- Arc'teryx Equipment