Solid Perfume Market Size

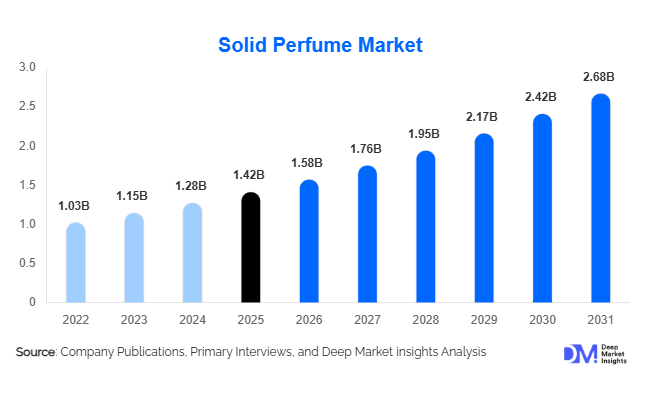

According to Deep Market Insights, the global solid perfume market size was valued at USD 1.42 billion in 2025 and is projected to grow from USD 1.58 billion in 2026 to reach USD 2.68 billion by 2031, expanding at a CAGR of 11.2% during the forecast period (2026–2031). The solid perfume market growth is being driven by rising consumer preference for portable fragrance formats, increasing demand for sustainable and refillable beauty products, and growing adoption of alcohol-free fragrance alternatives. The market is benefiting from premiumization trends across the global beauty industry, where consumers increasingly seek unique, travel-friendly, and environmentally responsible fragrance products. Solid perfumes have evolved from niche artisanal offerings into mainstream fragrance products, supported by strong growth in direct-to-consumer beauty brands, luxury fragrance houses, and wellness-focused personal care companies.

Key Market Insights

- Refillable and sustainable packaging formats are becoming a major purchasing factor, particularly among Gen Z and millennial consumers seeking eco-conscious beauty solutions.

- Premium and luxury fragrance brands are increasingly expanding solid perfume portfolios to capture demand for portable and travel-friendly fragrance products.

- Europe dominates the global solid perfume market, supported by strong fragrance consumption, luxury brand presence, and growing sustainability regulations.

- Asia-Pacific is the fastest-growing regional market, driven by rising disposable income, expanding beauty consumption, and increasing e-commerce penetration.

- Wellness-oriented fragrances incorporating aromatherapy benefits are gaining popularity, creating opportunities for product differentiation and premium pricing.

- Digital commerce and social media-driven fragrance discovery are accelerating consumer awareness and global product accessibility.

Solid Perfume Market Trends

Refillable and Sustainable Fragrance Formats Gaining Momentum

Sustainability has become one of the most influential trends shaping the solid perfume market. Consumers are increasingly seeking alternatives to traditional glass perfume bottles that generate significant packaging waste. As a result, manufacturers are introducing refillable compacts, reusable metal cases, biodegradable packaging materials, and reduced-plastic product designs. Solid perfumes naturally align with sustainability objectives due to their compact size, lower packaging requirements, and reduced transportation footprint. Luxury fragrance brands are increasingly positioning refillable solid perfumes as premium lifestyle products that combine convenience with environmental responsibility. Several companies are also implementing circular economy initiatives that encourage customers to purchase refill cartridges rather than entirely new products, supporting customer retention while reducing waste generation.

Wellness and Functional Fragrance Integration

The convergence of beauty and wellness industries is creating new growth opportunities for solid perfume manufacturers. Consumers increasingly seek products that provide emotional, psychological, and wellness benefits beyond traditional fragrance applications. In response, brands are introducing solid perfumes infused with essential oils and aromatherapy ingredients designed to support relaxation, stress relief, mood enhancement, focus, and sleep improvement. Wellness-focused fragrances are particularly gaining traction among younger consumers who prioritize holistic self-care routines. This trend is enabling manufacturers to differentiate products through functional benefits while simultaneously commanding premium pricing. The integration of wellness positioning is expected to expand the addressable consumer base and drive long-term innovation within the solid perfume category.

Solid Perfume Market Drivers

Growing Demand for Portable and Travel-Friendly Fragrance Products

One of the strongest growth drivers for the solid perfume market is increasing consumer demand for portable personal care products. Traditional liquid perfumes are often subject to airline restrictions, leakage concerns, and packaging fragility. Solid perfumes eliminate these challenges while offering convenience for consumers who travel frequently or maintain active lifestyles. Compact packaging formats enable consumers to carry fragrances easily throughout the day, supporting multiple fragrance applications and enhancing product utility. The rapid expansion of global tourism and business travel activities is further accelerating demand for portable fragrance solutions.

Expansion of Sustainable Beauty Consumption

Consumer preferences are increasingly shifting toward environmentally responsible beauty products. Sustainability considerations now influence purchasing decisions across nearly all beauty categories, including fragrances. Solid perfumes typically require less packaging, consume fewer transportation resources, and offer refillable options that reduce environmental impact. Governments, retailers, and consumers are collectively encouraging brands to adopt sustainable product strategies. This trend is expected to remain a major growth catalyst as environmental regulations continue to tighten globally and consumer awareness of packaging waste increases.

Solid Perfume Market Restraints

Limited Consumer Awareness Relative to Traditional Perfumes

Despite growing popularity, solid perfumes continue to face awareness challenges compared with conventional spray-based fragrances. Many consumers remain unfamiliar with application methods, performance characteristics, and product benefits. Limited shelf visibility in certain retail channels further restricts consumer education and trial opportunities. Manufacturers must continue investing in marketing campaigns, influencer partnerships, and product demonstrations to accelerate category awareness and adoption rates.

Lower Fragrance Projection Compared to Spray Perfumes

Solid perfumes generally provide a more intimate fragrance experience compared to alcohol-based spray formulations. While this characteristic appeals to some consumers, others perceive it as reduced performance or longevity. Fragrance enthusiasts seeking strong scent projection may continue to favor traditional perfume formats. Manufacturers are increasingly investing in formulation innovations to improve scent retention and diffusion while maintaining the portability and convenience benefits associated with solid perfumes.

Solid Perfume Market Opportunities

Expansion Across Emerging Asian Beauty Markets

Asia-Pacific represents the most attractive growth opportunity for solid perfume manufacturers over the forecast period. Countries including China, India, Indonesia, Vietnam, Thailand, and the Philippines are witnessing rapid growth in beauty product consumption due to urbanization, rising disposable income, and expanding middle-class populations. Younger consumers in these markets demonstrate strong interest in innovative, affordable, and social-media-driven beauty products. Localized fragrance development, digital marketing strategies, and e-commerce expansion are expected to create substantial revenue opportunities for both global and regional market participants.

Functional Fragrance and Wellness-Based Product Innovation

The growing popularity of wellness products creates significant opportunities for solid perfume manufacturers to develop functional fragrance offerings. Products positioned around emotional well-being, mindfulness, sleep enhancement, relaxation, and productivity improvement are increasingly resonating with consumers. Aromatherapy-inspired formulations using essential oils and botanical extracts allow companies to differentiate products while expanding beyond traditional fragrance applications. This trend is expected to drive premium product launches and support higher average selling prices across key markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.42 Billion |

| Market Size in 2026 | USD 1.58 Billion |

| Market Size in 2031 | USD 2.68 Billion |

| CAGR | 11.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Blended and multi-fragrance solid perfumes account for approximately 54% of the global market revenue in 2025, making them the dominant product category. Consumers increasingly prefer complex fragrance compositions that provide a more sophisticated sensory experience compared with single-note fragrances. Floral-woody, floral-fruity, gourmand, and signature blend combinations are particularly popular among premium fragrance buyers. Luxury fragrance houses continue introducing layered scent profiles that replicate the complexity traditionally associated with high-end liquid perfumes. Functional and aromatherapy-based solid perfumes represent one of the fastest-growing sub-segments as consumers seek products that deliver both fragrance and wellness benefits. Single-fragrance products continue to maintain relevance within natural and artisanal fragrance categories, particularly among consumers seeking simplicity and ingredient transparency.

Ingredient Composition Insights

Synthetic ingredient-based formulations represent approximately 68% of the global solid perfume market in 2025. These products offer superior formulation consistency, fragrance stability, scalability, and cost efficiency compared with exclusively natural alternatives. Synthetic fragrance molecules enable manufacturers to recreate complex scent profiles while maintaining reliable product performance across large-scale production volumes. However, natural and botanical-based formulations are gaining traction among consumers seeking clean-label and organic beauty products. Essential oil-based solid perfumes are particularly popular in premium wellness and aromatherapy categories, while hybrid formulations combining natural and synthetic ingredients are increasingly adopted to balance performance, sustainability, and affordability.

Distribution Channel Insights

Offline retail channels account for approximately 58% of total market revenues in 2025, making them the leading distribution segment. Fragrance purchases remain highly experiential, with consumers often preferring to test products before purchasing. Specialty beauty retailers, department stores, luxury boutiques, and duty-free outlets continue to play a critical role in product discovery and customer conversion. However, online retail channels are expanding rapidly due to increased consumer confidence in digital beauty purchases. Brand-owned websites, social commerce platforms, and e-commerce marketplaces are enabling manufacturers to reach broader audiences while reducing reliance on traditional retail intermediaries. Digital fragrance discovery through influencers, content creators, and social media communities is expected to support sustained online channel growth.

Consumer Age Group Insights

Millennials account for approximately 34% of the global solid perfume market revenue, making them the largest consumer segment. This demographic demonstrates strong purchasing power, high engagement with premium beauty products, and growing interest in sustainable lifestyle choices. Millennials are particularly attracted to refillable packaging, artisanal fragrance brands, and wellness-oriented beauty products. Gen Z consumers represent the fastest-growing age group due to their strong preference for portable, social-media-friendly products and environmentally conscious purchasing behavior. Older demographics, including Gen X and Baby Boomers, continue to support premium and luxury fragrance sales through brand loyalty and higher discretionary spending.

End-Use Insights

Personal use applications account for approximately 72% of total market demand in 2025, making them the dominant end-use segment. Consumers increasingly incorporate solid perfumes into daily grooming and self-care routines due to convenience and portability advantages. Travel and on-the-go fragrance applications represent the fastest-growing end-use category, benefiting from growth in tourism, business travel, and urban lifestyles. Gift purchases also contribute significantly to demand, particularly within premium and luxury product categories during holiday seasons and special occasions. Corporate gifting and promotional applications are emerging as new growth opportunities as companies seek premium, compact, and customizable personal care products for employee and client engagement programs.

Explore more data points, trends and opportunities Download Free Sample Report

Solid Perfume Market Segmentations

By Product Type

- Single-Fragrance Solid Perfume

- Blended/Multi-Fragrance Solid Perfume

- Layering Solid Perfume Products

- Functional/Aromatherapy Solid Perfumes

By Ingredient Composition

- Natural/Botanical-Based

- Synthetic Ingredient-Based

- Hybrid Formulations

By Packaging Format

- Metal Tins

- Compact Cases

- Refillable Cases

- Stick Format

- Pendant/Wearable Format

By Distribution Channel

- Specialty Beauty Stores

- Department Stores

- Perfume Boutiques

- Pharmacies & Drugstores

- Duty-Free Retail

- Brand-Owned Websites

- E-commerce Marketplaces

- Social Commerce

By End Use

- Personal Use

- Gift & Seasonal Purchases

- Travel & On-the-Go Fragrance Use

- Corporate & Promotional Gifting

Regional Insights

Europe

Europe accounted for approximately 31% of global market revenue in 2025, making it the largest regional market for solid perfumes. France remains the center of global fragrance innovation and luxury perfume manufacturing, while Germany, the United Kingdom, Italy, and Spain collectively contribute substantial demand. Sustainability initiatives, strong premium fragrance consumption, and established luxury beauty brands continue to support regional market leadership. European consumers demonstrate high adoption rates of refillable and environmentally responsible fragrance products, reinforcing long-term market growth.

North America

North America represented approximately 28% of global market revenue in 2025. The United States accounts for more than four-fifths of regional demand, driven by strong premium beauty spending, increasing adoption of clean beauty products, and growing interest in niche fragrance brands. Canada contributes additional growth through expanding consumer awareness of sustainable personal care products. Direct-to-consumer fragrance brands and e-commerce platforms continue to reshape market dynamics throughout the region.

Asia-Pacific

Asia-Pacific accounted for approximately 23% of global market revenue in 2025 and represents the fastest-growing regional market with forecast growth exceeding 13% CAGR through 2031. China remains the largest market within the region, supported by premium beauty consumption and luxury brand penetration. India is emerging as the fastest-growing country market due to expanding middle-class purchasing power and rising awareness of personal grooming products. Japan and South Korea continue driving innovation through advanced beauty trends and strong consumer spending on premium fragrances.

Latin America

Latin America accounted for approximately 5% of global market revenue in 2025. Brazil dominates regional demand due to its large beauty and personal care industry, followed by Mexico and Argentina. Increasing disposable income and growing consumer interest in premium fragrance products are gradually expanding market opportunities throughout the region.

Middle East & Africa

The Middle East & Africa region represented approximately 2% of global market revenue in 2025. The United Arab Emirates and Saudi Arabia account for the majority of demand, supported by strong cultural affinity for fragrances and increasing luxury consumption. Rising premium beauty spending and tourism-related retail expansion continue to create growth opportunities across key regional markets.

Key Players in the Solid Perfume Market

- L'Oréal Group

- Estée Lauder Companies

- LVMH

- Chanel

- Coty Inc.

- Shiseido Company

- Puig

- Diptyque

- Lush

- Aesop

- Byredo

- Le Labo

- Jo Malone London

- Glossier

- Fenty Beauty