Men's Fragrance Market Size

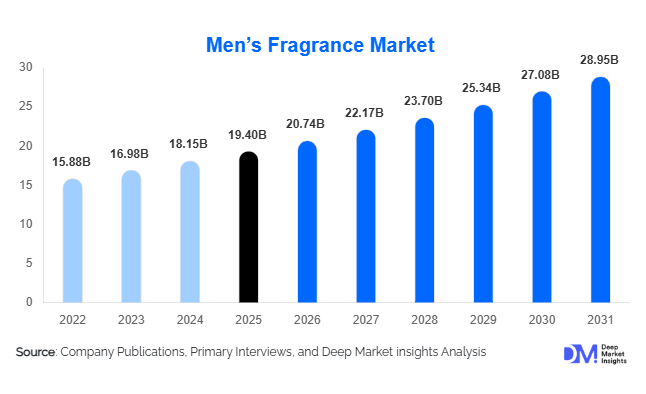

According to Deep Market Insights, the global men's fragrance market size was valued at USD 19.4 billion in 2025 and is projected to grow from USD 20.74 billion in 2026 to reach USD 28.95 billion by 2031, expanding at a CAGR of 6.9% during the forecast period (2026–2031). The market growth is primarily driven by increasing male grooming expenditure, rising demand for premium and luxury fragrances, growing influence of social media on purchasing decisions, and expanding consumer preference for personal care products that support self-expression and lifestyle positioning. Fragrance consumption among men has evolved beyond traditional colognes, with consumers increasingly purchasing multiple scents for different occasions, seasons, and social settings. The proliferation of niche fragrance brands, direct-to-consumer sales models, and digital fragrance discovery platforms is further accelerating market expansion across both developed and emerging economies.

Key Market Insights

- Premium and luxury fragrances account for more than 60% of global market revenues, driven by strong consumer preference for higher concentration formulations and exclusive scent profiles.

- Eau de Parfum (EDP) remains the largest product category, representing approximately 34% of global men's fragrance sales due to its balance of longevity and affordability.

- Europe dominates the global market, accounting for nearly 31% of total revenues, supported by strong fragrance heritage and luxury brand concentration.

- Asia-Pacific is the fastest-growing regional market, driven by rising disposable incomes, urbanization, and increasing fragrance adoption among younger consumers.

- Digital commerce is transforming fragrance discovery, with online channels accounting for a growing share of premium fragrance purchases globally.

- Oud, amber, and woody fragrance families continue to gain popularity, influenced by growing Middle Eastern fragrance preferences and luxury consumer trends.

Men's Fragrance Market Trends

Premiumization and Fragrance Wardrobe Expansion

The men's fragrance industry is witnessing a significant shift toward premiumization, with consumers increasingly moving from mass-market products to prestige and luxury fragrance offerings. Rather than owning a single signature fragrance, many consumers now curate fragrance wardrobes consisting of multiple scents tailored to specific occasions, seasons, and moods. This trend is particularly prominent among Millennials and Generation Z consumers, who view fragrances as lifestyle accessories and personal identity markers. Luxury houses and niche fragrance brands are responding by introducing limited-edition collections, artisanal ingredients, and exclusive formulations that command premium pricing while strengthening customer loyalty and repeat purchases.

Growth of Digital Fragrance Discovery and Personalization

E-commerce and social media platforms have fundamentally transformed how consumers discover and purchase fragrances. Influencer reviews, fragrance-focused content creators, and online fragrance communities have become powerful demand drivers. At the same time, brands are investing heavily in AI-powered fragrance recommendation engines, virtual consultations, and personalized scent profiling tools to improve customer engagement and conversion rates. Direct-to-consumer channels are enabling brands to collect consumer insights, customize offerings, and build stronger customer relationships while reducing dependence on traditional retail distribution networks.

Men's Fragrance Market Drivers

Rising Male Grooming and Self-Care Expenditure

The growing acceptance of men's grooming and self-care products is a major growth driver for the men's fragrance market. Consumers increasingly perceive fragrances as essential components of personal grooming routines rather than discretionary luxury purchases. This trend is supported by rising disposable incomes, greater workplace emphasis on professional appearance, and growing awareness of personal wellness and confidence enhancement. Younger demographics are entering the fragrance category earlier than previous generations, expanding the addressable consumer base and increasing purchase frequency.

Expansion of Luxury Beauty and Premium Consumption

The global expansion of luxury beauty consumption continues to support fragrance market growth. Affluent consumers across North America, Europe, Asia-Pacific, and the Middle East are demonstrating increased willingness to spend on premium fragrance products featuring rare ingredients, higher concentrations, and exclusive brand heritage. Luxury fragrance launches are consistently outperforming broader beauty market growth rates, while niche brands are gaining traction through differentiated positioning and craftsmanship-focused marketing strategies.

Men's Fragrance Market Restraints

Volatility in Natural Ingredient Prices

Raw material price fluctuations remain a persistent challenge for fragrance manufacturers. Key natural ingredients such as oud, sandalwood, jasmine, rose extracts, and citrus oils are highly susceptible to climatic disruptions, agricultural production variability, and geopolitical supply chain risks. These fluctuations can significantly impact production costs and compress profit margins, particularly within premium and luxury fragrance categories that rely heavily on natural ingredients.

Increasing Regulatory Compliance Requirements

Fragrance manufacturers face increasingly stringent regulations regarding ingredient disclosure, allergen restrictions, sustainability standards, and environmental compliance. Regulatory frameworks across Europe, North America, and select Asia-Pacific markets require ongoing investments in product reformulation, testing, and certification. Compliance costs continue to rise, creating challenges for smaller manufacturers and new market entrants while potentially limiting innovation speed.

Men's Fragrance Market Opportunities

Expansion of Niche and Artisanal Fragrance Segments

The niche fragrance segment represents one of the most attractive growth opportunities within the global men's fragrance industry. Consumers are increasingly seeking unique scent compositions, limited-edition releases, and artisanal craftsmanship that differentiate products from mainstream offerings. Niche fragrance brands often command significantly higher price points and margins while benefiting from strong customer loyalty. The growing popularity of fragrance collecting and scent exploration among younger demographics is expected to further support category expansion over the coming decade.

Growth Across Emerging Markets

Emerging markets across Asia-Pacific, the Middle East, and Latin America present substantial untapped growth potential. Rising urbanization, increasing disposable incomes, expanding middle-class populations, and growing awareness of global beauty trends are driving fragrance adoption. Countries such as India, China, Indonesia, Vietnam, Saudi Arabia, and the UAE are experiencing particularly strong growth rates. The increasing influence of luxury retail development and e-commerce penetration in these markets is creating favorable conditions for both established brands and new entrants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 19.4 Billion |

| Market Size in 2026 | USD 20.74 Billion |

| Market Size in 2031 | USD 28.95 Billion |

| CAGR | 6.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Concentration Insights

Eau de Parfum (EDP) dominates the men's fragrance market, accounting for approximately 34% of global revenues in 2025. Consumers favor EDP products because they provide longer-lasting scent performance than Eau de Toilette while remaining more affordable than Parfum concentrations. Premium and luxury fragrance brands continue to prioritize EDP launches due to strong consumer demand and favorable profit margins. Eau de Toilette remains widely adopted among younger consumers and first-time fragrance buyers, while niche Parfum offerings are gaining traction among affluent fragrance enthusiasts seeking enhanced longevity and exclusivity.

Pricing Tier Insights

Premium fragrances represent the largest pricing segment, contributing approximately 41% of total market revenues. Consumers increasingly seek products that offer superior quality, stronger brand recognition, and longer-lasting formulations without reaching ultra-luxury price levels. Luxury and prestige fragrances continue to expand rapidly, supported by growing disposable incomes and premiumization trends. Meanwhile, niche artisanal fragrances are emerging as one of the fastest-growing subsegments, attracting consumers interested in uniqueness, craftsmanship, and exclusive scent profiles.

Fragrance Family Insights

Woody fragrances account for nearly 22% of global men's fragrance demand and remain the most popular fragrance family worldwide. Their versatility, masculine appeal, and compatibility with luxury positioning have contributed to widespread adoption across both mature and emerging markets. Fresh aquatic and citrus-based fragrances continue to perform strongly in warmer climates and among younger demographics, while oud, amber, leather, and oriental fragrances are witnessing accelerated growth due to increasing global influence from Middle Eastern fragrance traditions.

Distribution Channel Insights

Specialty beauty and fragrance stores maintain the largest market share, accounting for approximately 28% of global sales. Consumers continue to value in-store product testing, fragrance consultation services, and experiential retail environments when purchasing premium products. However, e-commerce is rapidly gaining share as digital fragrance discovery tools, influencer marketing, and direct-to-consumer platforms improve online conversion rates. Travel retail and duty-free channels remain important for luxury fragrance purchases, particularly among international travelers seeking premium brands and exclusive product offerings.

Consumer Age Group Insights

Consumers aged 20–34 years represent the largest customer segment, contributing approximately 46% of global fragrance demand. This demographic exhibits high engagement with social media, influencer recommendations, and online fragrance communities, resulting in elevated purchasing frequency and experimentation with multiple fragrance brands. Consumers aged 35–54 years remain significant contributors to premium and luxury sales due to higher disposable incomes, while teenage consumers increasingly enter the category through celebrity-endorsed and entry-level premium fragrance products.

Explore more data points, trends and opportunities Download Free Sample Report

Men’s Fragrance Market Segmentations

By Product Concentration

- Parfum / Extrait de parfum

- Eau de parfum (EDP)

- Eau de toilette (EDT)

- Eau de cologne (EDC)

- Aftershave Fragrances

- Fragrance Mists & Body Sprays

By Pricing Tier

- Mass Market Fragrances

- Premium Fragrances

- Luxury / Prestige Fragrances

- Niche / Ultra-Luxury Fragrances

By Fragrance Family

- Woody

- Fresh / Aquatic

- Citrus

- Oriental / Amber

- Spicy

- Aromatic Fougère

- Leather & Tobacco

- Gourmand

- Floral

By Distribution Channel

- Specialty Beauty & Fragrance Stores

- Department Stores

- Brand-Owned Retail Stores

- Online Retail / E-commerce / DTC

- Hypermarkets & Supermarkets

- Travel Retail / Duty-Free

- Pharmacies & Drugstores

Regional Insights

North America

North America accounts for approximately 27% of global men's fragrance revenues, with the United States representing the overwhelming majority of regional demand. Premiumization, luxury beauty spending, and strong e-commerce penetration continue to support market growth. Consumers increasingly purchase fragrances through direct-to-consumer channels and specialty retailers, while celebrity-endorsed products and social media influence remain significant purchasing drivers.

Europe

Europe remains the largest regional market, contributing approximately 31% of global revenues. France serves as the global center of fragrance innovation and production, while Germany, the United Kingdom, Italy, and Spain represent major consumption markets. Strong luxury brand heritage, established consumer preferences, and premium fragrance adoption continue to support regional leadership. Europe also remains a major exporter of fragrance products to global markets.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is expected to record CAGR growth approaching 9% through 2031. China, Japan, South Korea, India, and Southeast Asian countries are driving demand through rising disposable incomes and growing interest in personal grooming. India represents one of the fastest-growing national markets globally, supported by expanding middle-class consumption and increasing adoption of premium fragrance products.

Latin America

Brazil dominates fragrance consumption across Latin America, followed by Mexico and Argentina. Growing urbanization, rising beauty spending, and increased penetration of premium personal care products are supporting market expansion. International brands continue to strengthen their presence through retail partnerships and digital distribution channels.

Middle East & Africa

The Middle East remains one of the world's most fragrance-intensive regions, led by Saudi Arabia and the UAE. Oud-based and oriental fragrance families dominate consumer preferences, while luxury fragrance spending remains among the highest globally on a per-capita basis. Africa represents a smaller but steadily growing opportunity, supported by expanding urban populations and improving retail infrastructure across key markets.

Key Players in the Men's Fragrance Market

- L'Oréal

- LVMH

- Coty

- Puig

- Estée Lauder Companies

- Chanel

- Shiseido

- Inter Parfums

- Hermès

- Kering Beauté

- Prada Beauty

- Dolce & Gabbana Beauty

- Amorepacific

- Revlon

- Procter & Gamble