Lipstick Market Size

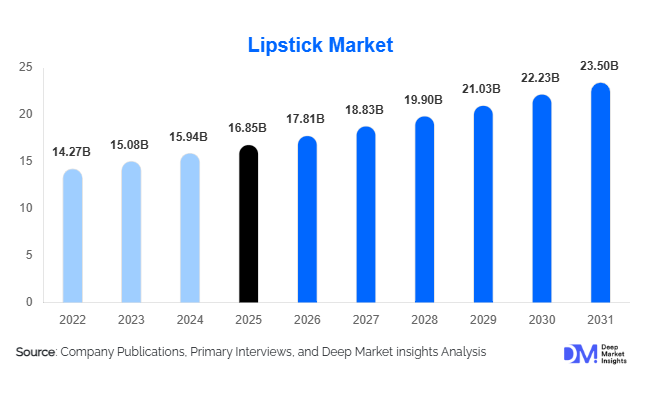

According to Deep Market Insights, the global lipstick market size was valued at USD 16.85 billion in 2025 and is projected to grow from USD 17.81 billion in 2026 to reach USD 23.50 billion by 2031, expanding at a CAGR of 5.7% during the forecast period (2026–2031). The lipstick market growth is primarily driven by increasing consumer spending on personal care products, rising demand for premium and long-wear cosmetic formulations, growing influence of social media beauty trends, and continuous product innovation across luxury and mass-market segments. The market continues to benefit from the expansion of e-commerce channels, increasing adoption of clean beauty products, and the emergence of multifunctional lip products that combine color cosmetics with skincare benefits.

Key Market Insights

- Matte and long-wear lipstick formulations continue to dominate global demand, supported by consumer preference for transfer-proof and durable cosmetic products.

- Clean beauty and vegan lipsticks are gaining significant market traction, particularly across North America and Europe, where ingredient transparency has become a key purchasing factor.

- Asia-Pacific leads global lipstick consumption, driven by expanding middle-class populations, increasing beauty awareness, and strong growth in China, India, Japan, and South Korea.

- E-commerce has emerged as the fastest-growing distribution channel, supported by influencer marketing, virtual try-on technologies, and direct-to-consumer brand strategies.

- Premium and luxury lipstick categories continue to outperform mass-market products in value growth, driven by premiumization trends and rising disposable incomes.

- Artificial intelligence, augmented reality, and personalized beauty technologies are increasingly reshaping product discovery, shade matching, and customer engagement.

Lipstick Market Trends

Clean Beauty and Sustainable Formulations Reshaping Product Development

Consumer awareness regarding product ingredients and environmental sustainability is transforming lipstick product development globally. Manufacturers are increasingly introducing vegan, cruelty-free, organic, and paraben-free formulations to address changing consumer preferences. Sustainable packaging innovations such as refillable lipstick cartridges, recyclable aluminum casings, and biodegradable packaging materials are gaining popularity among premium beauty brands. Companies are also investing in ethically sourced pigments, plant-based oils, and naturally derived waxes to strengthen their sustainability credentials. These developments are particularly influential in North America and Europe, where environmentally conscious purchasing behavior continues to accelerate.

Technology-Driven Personalization Driving Consumer Engagement

Digital technologies are becoming central to the lipstick purchasing journey. Brands are increasingly deploying AI-powered shade recommendation engines, virtual try-on tools, and augmented reality applications to enhance customer experiences. Consumers can now visualize lipstick shades on their facial features before purchasing, significantly improving conversion rates and reducing product returns. Personalized product recommendations based on skin tone, purchasing history, and beauty preferences are becoming commonplace. Social commerce integration and influencer-driven digital campaigns are further strengthening consumer engagement and supporting rapid product discovery among younger demographics.

Lipstick Market Drivers

Growing Consumer Spending on Beauty and Personal Care Products

Rising disposable incomes and increasing emphasis on personal grooming are major factors supporting lipstick market growth. Consumers across developed and emerging economies are allocating a greater proportion of discretionary spending toward beauty products. Premium cosmetic products are benefiting particularly from rising purchasing power among urban consumers, while younger demographics continue to drive purchase frequency through trend-driven consumption patterns.

Influence of Social Media and Beauty Influencers

Social media platforms have become powerful drivers of lipstick demand globally. Beauty influencers, celebrities, and content creators regularly introduce new product launches, application techniques, and seasonal trends, significantly influencing consumer purchasing decisions. Platforms such as Instagram, TikTok, YouTube, and regional beauty communities have reduced barriers to product discovery while accelerating global adoption of emerging lipstick trends.

Lipstick Market Restraints

Intense Market Competition and Product Saturation

The lipstick market remains highly competitive, with numerous multinational corporations, independent beauty brands, and celebrity-led cosmetic companies competing across multiple price points. Product saturation increases marketing expenditures and customer acquisition costs while making brand differentiation increasingly difficult. Frequent product launches and changing fashion trends further intensify competitive pressures.

Volatility in Raw Material and Packaging Costs

Manufacturers face ongoing challenges associated with fluctuations in the prices of pigments, oils, waxes, specialty ingredients, and packaging materials. Rising transportation costs and increasing demand for sustainable packaging solutions can impact profitability, particularly for smaller manufacturers. Cost pressures may also affect product pricing strategies and limit adoption of premium sustainable materials.

Lipstick Market Opportunities

Expansion of Clean Beauty and Vegan Cosmetics

The global clean beauty movement presents significant opportunities for lipstick manufacturers. Demand for ingredient transparency, cruelty-free testing practices, and environmentally responsible production methods continues to grow. Companies investing in certified organic, vegan, and sustainable lipstick lines are positioned to capture premium pricing opportunities and strengthen brand loyalty among environmentally conscious consumers. The clean beauty segment is expected to outperform conventional cosmetics growth rates throughout the forecast period.

Emerging Market Growth Across Asia, Middle East, and Latin America

Rapid urbanization, increasing disposable incomes, and expanding beauty awareness are creating substantial growth opportunities across emerging economies. Countries such as India, Indonesia, Vietnam, Saudi Arabia, Brazil, and Mexico are experiencing rising cosmetics penetration rates. Growing female workforce participation, social media adoption, and expanding retail infrastructure are supporting lipstick demand among first-time and aspirational consumers. These markets are expected to contribute significantly to future industry expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 16.85 Billion |

| Market Size in 2026 | USD 17.81 Billion |

| Market Size in 2031 | USD 23.50 Billion |

| CAGR | 5.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Format Insights

Bullet or stick lipsticks remain the largest product category, accounting for approximately 42% of global market revenue in 2025. Their dominance is attributed to consumer familiarity, portability, ease of application, and broad availability across retail channels. Liquid lipsticks represent the fastest-growing product format due to increasing demand for transfer-proof and long-lasting formulations. Lip crayons and lip stains continue to gain popularity among younger consumers seeking convenience and multifunctional usage. Hybrid lipstick-balm products are emerging as an important growth category by combining cosmetic appeal with lip care benefits.

Finish Type Insights

Matte lipsticks accounted for nearly 31% of global lipstick market revenue in 2025, making them the largest finish category. Consumer preference for long-lasting wear, minimal transfer, and modern aesthetics continues to drive demand. Satin and cream finishes remain popular among consumers seeking hydration and comfort, while glossy formulations are experiencing renewed growth due to changing beauty trends. Metallic and velvet finishes are increasingly adopted within premium and fashion-driven product portfolios, particularly among younger demographics influenced by social media beauty trends.

Distribution Channel Insights

Offline retail channels continue to dominate lipstick sales, accounting for approximately 63% of global revenue in 2025. Specialty beauty stores, department stores, supermarkets, and pharmacies remain important distribution points due to consumers' preference for physical product evaluation before purchase. However, e-commerce represents the fastest-growing channel, supported by virtual try-on technologies, influencer marketing campaigns, and direct-to-consumer sales strategies. Beauty subscription services and social commerce platforms are also emerging as important customer acquisition channels for both established and independent brands.

Consumer Age Group Insights

Consumers aged 20–34 years represent the largest age demographic within the lipstick market, accounting for approximately 38% of global demand. This segment exhibits high engagement with beauty trends, social media content, and premium cosmetic products. Consumers aged 35–49 years remain a major revenue contributor due to higher disposable incomes and strong brand loyalty. Teen consumers increasingly influence trend adoption, while mature consumers continue to support premium lipstick categories focused on hydration, anti-aging benefits, and comfort-oriented formulations.

End-User Insights

Individual consumers account for approximately 85% of global lipstick consumption, making them the dominant end-user segment. Professional makeup artists and beauty salons represent a growing commercial segment supported by increasing demand for bridal makeup, fashion events, entertainment productions, and social media content creation. The professional beauty services sector is expected to witness above-average growth due to rising beauty service spending and expanding salon infrastructure across emerging markets. The entertainment and fashion industries continue to create incremental demand for premium and high-performance lipstick products.

Explore more data points, trends and opportunities Download Free Sample Report

Lipstick Market Segmentations

By Product Format

- Bullet/Stick Lipstick

- Liquid Lipstick

- Lip Crayon/Pencil Lipstick

- Lip Palette Lipstick

- Lip Stain/Tint Lipstick

- Hybrid Lipstick-Balm Products

By Finish Type

- Matte

- Satin

- Cream

- Glossy

- Shimmer/Frost

- Metallic

- Velvet/Blurred Finish

By Ingredient Composition

- Conventional/Synthetic

- Natural & Botanical

- Organic Certified

- Vegan

- Clean Beauty Formulations

By Price Tier

- Economy/Mass Market

- Mid-Premium

- Premium

- Luxury Prestige

By Distribution Channel

- Hypermarkets & Supermarkets

- Specialty Beauty Stores

- Department Stores

- Brand-Owned Retail Stores

- Pharmacies & Drug Stores

- E-Commerce Marketplaces

- Direct-to-Consumer Websites

- Social Commerce Platforms

Regional Insights

North America

North America accounted for approximately 26.4% of global lipstick market revenue in 2025. The United States represents the region's largest market, driven by premium beauty consumption, strong brand presence, and high per-capita spending on cosmetics. Canada continues to benefit from increasing demand for sustainable and clean beauty products, while Mexico is experiencing steady growth supported by rising beauty awareness and expanding retail distribution networks. Premiumization and digital beauty technologies remain key drivers throughout the region.

Europe

Europe represents approximately 24% of global lipstick demand, led by France, Germany, the United Kingdom, Italy, and Spain. The region benefits from a mature cosmetics industry, strong luxury beauty heritage, and growing demand for sustainable formulations. European consumers demonstrate high preference for premium, organic, and ethically sourced beauty products. France remains a major production and export hub for luxury cosmetics, while Germany and the United Kingdom continue to drive innovation in clean beauty and digital commerce.

Asia-Pacific

Asia-Pacific is the largest regional market, accounting for approximately 31.6% of global lipstick revenue in 2025. China remains the largest contributor, supported by rapid urbanization, increasing premium beauty adoption, and strong e-commerce penetration. India is among the fastest-growing markets globally, benefiting from rising disposable incomes, expanding middle-class populations, and increasing beauty consciousness. Japan and South Korea continue to influence global beauty trends through product innovation, advanced formulations, and sophisticated skincare-integrated cosmetics.

Latin America

Latin America contributes approximately 10% of global lipstick market revenues, with Brazil representing the region's largest market. Growing beauty consciousness, expanding middle-class populations, and increasing digital retail adoption support demand growth. Mexico and Argentina continue to strengthen regional consumption through improving retail infrastructure and rising premium cosmetics penetration.

Middle East & Africa

The Middle East & Africa region accounted for approximately 6.6% of global lipstick market revenue in 2025. Saudi Arabia and the United Arab Emirates are leading markets due to high spending on luxury cosmetics and premium beauty products. South Africa remains the largest African market, while increasing urbanization and beauty product accessibility are supporting growth across several emerging economies. Luxury beauty brands continue to expand their regional presence through dedicated retail stores and premium shopping destinations.

Key Players in the Lipstick Market

- L'Oréal SA

- Estée Lauder Companies Inc.

- Coty Inc.

- Shiseido Co., Ltd.

- Chanel

- Christian Dior

- Revlon Inc.

- Amorepacific Corporation

- Unilever PLC

- Kao Corporation

- Mary Kay Inc.

- Oriflame Holding AG

- Natura & Co

- e.l.f. Beauty Inc.

- Huda Beauty