Liposomal Supplements Market Size

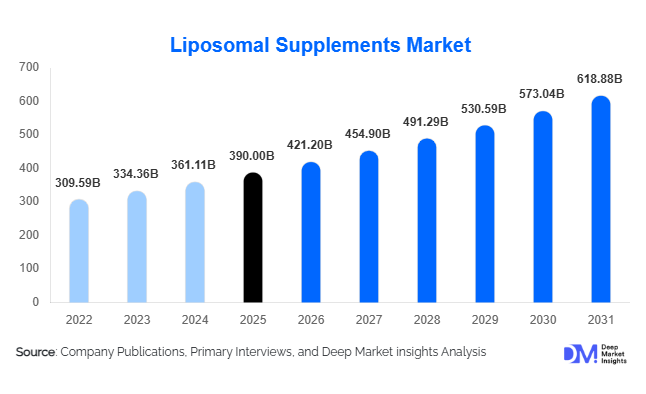

According to Deep Market Insights, the global liposomal supplements market size was valued at USD 390 million in 2025 and is projected to grow from USD 421.20 million in 2026 to reach USD 618.88 million by 2031, expanding at a CAGR of 8.0% during the forecast period (2026–2031). The liposomal supplements market growth is primarily driven by increasing consumer demand for highly bioavailable nutritional products, growing awareness regarding preventive healthcare, and advancements in liposomal delivery technologies that improve nutrient absorption and efficacy. The market is also benefiting from rising adoption of personalized nutrition, growing healthcare practitioner recommendations, and expanding direct-to-consumer supplement distribution channels.

Key Market Insights

- Liposomal vitamin C remains the largest product category, accounting for nearly 24% of global market revenue due to strong demand for immune-support supplements.

- Liquid liposomal formulations dominate the market, representing approximately 38% of total sales owing to superior absorption and ease of consumption.

- North America leads the global market, accounting for approximately 42% of total revenue, supported by high supplement consumption rates and strong consumer purchasing power.

- Asia-Pacific is the fastest-growing regional market, driven by expanding nutraceutical adoption in China, India, Japan, and Southeast Asia.

- E-commerce channels account for more than one-third of market sales, enabling manufacturers to reach consumers directly through subscription and personalized wellness programs.

- Clinical validation and healthcare practitioner adoption are becoming key competitive differentiators among premium supplement brands.

Liposomal Supplements Market Trends

Personalized Nutrition Driving Product Innovation

Personalized nutrition continues to emerge as one of the most influential trends shaping the liposomal supplements market. Consumers increasingly seek customized nutritional solutions tailored to individual health conditions, genetic profiles, fitness goals, and lifestyle requirements. Liposomal delivery systems are particularly well-suited to personalized nutrition because they can efficiently deliver targeted nutrient combinations while improving bioavailability. Companies are increasingly integrating AI-powered health assessments, microbiome testing, and customized supplement subscriptions into their product offerings. This trend is expected to strengthen customer retention rates while creating premium pricing opportunities for manufacturers.

Premiumization of Nutraceutical Products

Consumers are increasingly willing to pay premium prices for scientifically validated nutritional products that demonstrate measurable health outcomes. Liposomal formulations are benefiting from this shift because they offer superior absorption compared with conventional tablets and capsules. Brands are investing heavily in clinical studies, clean-label ingredients, non-GMO certifications, vegan formulations, and sustainable sourcing to further differentiate their offerings. Growing consumer awareness regarding nutrient bioavailability and supplement efficacy continues to accelerate demand for premium liposomal formulations across developed and emerging markets.

Liposomal Supplements Market Drivers

Growing Demand for High-Bioavailability Supplements

One of the primary drivers of market growth is increasing consumer awareness regarding nutrient absorption efficiency. Traditional supplements often experience degradation during digestion, reducing nutrient uptake. Liposomal technology addresses this challenge by encapsulating active ingredients within phospholipid vesicles that enhance absorption and cellular delivery. As consumers become more educated about supplement efficacy, demand for liposomal products continues to rise across immunity, healthy aging, cardiovascular health, and sports nutrition applications.

Expansion of Preventive Healthcare Spending

The global shift toward preventive healthcare has significantly increased demand for advanced nutritional products. Rising prevalence of chronic diseases, aging populations, and heightened health consciousness are encouraging consumers to invest in nutritional supplements designed to maintain long-term wellness. Liposomal products are increasingly positioned as premium preventive healthcare solutions due to their enhanced delivery mechanisms and perceived effectiveness. Healthcare providers and wellness practitioners are also recommending these products more frequently, further supporting market expansion.

Liposomal Supplements Market Restraints

High Production and Formulation Costs

Liposomal supplements require specialized manufacturing equipment, high-quality phospholipid ingredients, and advanced formulation expertise. These factors significantly increase production costs compared to conventional dietary supplements. The resulting premium pricing can limit consumer adoption in cost-sensitive markets and create challenges for manufacturers seeking mass-market penetration.

Regulatory Complexity Across Regions

The global nutraceutical industry operates under diverse regulatory frameworks governing health claims, labeling requirements, and product approvals. Manufacturers must invest significantly in compliance and clinical validation activities to support product claims. Variations in regulations between North America, Europe, Asia-Pacific, and other regions can complicate international expansion strategies and increase operational costs.

Liposomal Supplements Market Opportunities

Expansion into Emerging Asia-Pacific Markets

Asia-Pacific presents substantial growth opportunities due to increasing healthcare expenditures, rising disposable incomes, and expanding awareness regarding preventive nutrition. Countries such as China, India, Indonesia, Vietnam, and Thailand remain significantly underpenetrated compared to North America and Europe. Manufacturers investing in local partnerships, regional production capabilities, and targeted educational campaigns can capitalize on strong long-term growth potential.

Healthcare Practitioner and Clinical Channel Growth

Functional medicine clinics, wellness centers, anti-aging practices, and integrative healthcare providers are increasingly incorporating liposomal supplements into patient treatment protocols. Products supported by clinical research and physician education initiatives are expected to gain significant market share. This channel offers premium pricing opportunities while strengthening brand credibility and consumer trust.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 390 Billion |

| Market Size in 2026 | USD 421.20 Billion |

| Market Size in 2031 | USD 618.88 Billion |

| CAGR | 8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Active Ingredient Type Insights

Liposomal vitamin C remains the largest segment, accounting for approximately 24% of global market revenue in 2025. Strong consumer awareness regarding immune health, antioxidant protection, and wellness maintenance continues to support segment leadership. Liposomal glutathione and liposomal vitamin D are among the fastest-growing categories due to increasing interest in detoxification, healthy aging, and bone health applications. Coenzyme Q10, curcumin, omega-3 fatty acids, and specialized antioxidant blends are also gaining traction as consumers seek clinically supported formulations with superior absorption profiles.

Product Format Insights

Liquid liposomal supplements dominate the market with approximately 38% share of global revenue. Consumers prefer liquid formulations because they offer rapid absorption, dosage flexibility, and improved convenience. Capsules and softgels represent the second-largest category, particularly among consumers seeking portability and ease of use. Powder formulations, stick packs, oral sprays, and gummies are gaining popularity due to product innovation and increasing demand for convenient nutritional formats. Manufacturers continue introducing novel delivery systems to improve stability, shelf life, and consumer acceptance.

Health Benefit Insights

Immune health applications account for nearly 29% of total market demand, supported by sustained consumer focus on disease prevention and wellness optimization. Healthy aging, cardiovascular health, cognitive performance, and sports recovery are emerging as key growth segments. Increasing interest in stress management, sleep support, skin health, and detoxification solutions is also driving diversification within the market. As consumers adopt holistic wellness strategies, multifunctional formulations combining multiple health benefits are expected to gain popularity.

Distribution Channel Insights

E-commerce platforms account for approximately 34% of global liposomal supplement sales, making them the leading distribution channel. Direct-to-consumer business models, subscription programs, influencer marketing, and personalized product recommendations have strengthened online sales growth. Pharmacies and specialty nutrition stores continue to play important roles, particularly for premium and practitioner-recommended products. Healthcare practitioner channels are expanding rapidly as functional medicine and integrative healthcare providers increasingly recommend liposomal formulations to patients.

Consumer Group Insights

Adults represent the largest consumer group, accounting for approximately 55% of total market demand. This segment benefits from strong purchasing power, growing preventive healthcare awareness, and increasing adoption of nutritional supplementation. Athletes and fitness enthusiasts represent one of the fastest-growing groups, driven by demand for enhanced nutrient delivery and recovery support. The geriatric population is also contributing significantly to market growth as older consumers seek solutions that support healthy aging, cognitive function, and cardiovascular wellness.

Explore more data points, trends and opportunities Download Free Sample Report

Liposomal Supplements Market Segmentations

By Active Ingredient Type

- Liposomal Vitamin C

- Liposomal Vitamin D

- Liposomal Vitamin B Complex

- Liposomal Vitamin B12

- Liposomal Multivitamins

- Liposomal Minerals

- Liposomal Glutathione

- Liposomal Curcumin

- Liposomal Coenzyme Q10 (CoQ10)

- Liposomal Omega-3 & Essential Fatty Acids

- Liposomal Probiotics & Gut Health Ingredients

- Liposomal Herbal/Botanical Extracts

- Liposomal Amino Acids

- Liposomal Antioxidant Blends

- Other Liposomal Nutraceutical Ingredients

By Product Format

- Liquid Liposomal Supplements

- Softgel Liposomal Supplements

- Capsule Liposomal Supplements

- Powder Liposomal Supplements

- Sachets & Stick Packs

- Gummies & Chewables

- Oral Sprays

- Other Delivery Formats

By Health Benefit/Application

- Immune Health

- Energy & Metabolism

- Cognitive Health & Brain Function

- Cardiovascular Health

- Bone & Joint Health

- Digestive & Gut Health

- Healthy Aging & Longevity

- Sports Nutrition & Recovery

- Detoxification & Liver Health

- Skin, Hair & Beauty

- Women's Health

- Men's Health

- Sleep & Stress Management

- General Wellness & Preventive Nutrition

By Distribution Channel

- Pharmacies & Drug Stores

- Health & Nutrition Specialty Stores

- Supermarkets & Hypermarkets

- Direct-to-Consumer (DTC)

- E-Commerce Platforms

- Practitioner/Healthcare Professional Channels

By Consumer Group

- Children

- Adolescents

- Adults

- Geriatric Population

- Athletes & Fitness Enthusiasts

- Pregnant & Lactating Women

Regional Insights

North America

North America accounts for approximately 42% of global market revenue, making it the largest regional market. The United States contributes nearly 30% of worldwide demand due to high supplement consumption rates, advanced healthcare infrastructure, and strong consumer awareness regarding premium nutritional products. Canada continues to experience steady growth driven by increasing adoption of preventive healthcare solutions and functional wellness products.

Europe

Europe represents approximately 30% of global market revenue, led by Germany, the United Kingdom, France, Italy, and Spain. Demand is supported by aging populations, strong preventive healthcare cultures, and increasing preference for scientifically validated nutritional products. European consumers demonstrate strong interest in clean-label, sustainable, and clinically supported supplement formulations.

Asia-Pacific

Asia-Pacific accounts for approximately 23% of global demand and is the fastest-growing regional market. China, Japan, India, South Korea, and Australia are driving growth through expanding healthcare awareness, rising disposable incomes, and increasing acceptance of nutraceutical products. India and China are expected to generate particularly strong demand growth due to expanding middle-class populations and rapidly developing e-commerce ecosystems.

Latin America

Brazil remains the largest market in Latin America, followed by Mexico, Argentina, and Chile. Rising health consciousness and increasing availability of premium nutritional products are supporting market development across the region. Local distributors and international brands are expanding their presence to capitalize on growing consumer demand.

Middle East & Africa

The Middle East and Africa region is experiencing gradual growth led by the United Arab Emirates, Saudi Arabia, and South Africa. Increasing healthcare spending, wellness-focused lifestyles, and demand for premium imported supplements are supporting regional market expansion. The UAE is emerging as a key regional hub for nutraceutical imports and distribution.

Key Players in the Liposomal Supplements Market

- LivOn Labs

- Quicksilver Scientific

- Purality Health

- NOW Foods

- Pure Encapsulations

- YourZooki

- Altrient

- Solaray

- AFT Pharmaceuticals

- Lipolife

- Lipo Naturals

- Codeage

- Seeking Health

- MaryRuth Organics

- Designs for Health