Lip Gloss Market Size

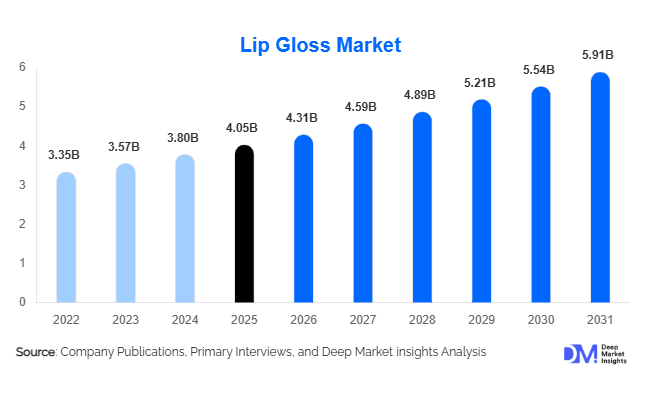

According to Deep Market Insights, the global lip gloss market size was valued at USD 4.05 billion in 2025 and is projected to grow from USD 4.31 billion in 2026 to reach USD 5.91 billion by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). Market growth is being driven by increasing consumer preference for glossy and natural makeup looks, rising demand for multifunctional cosmetic products, growing popularity of clean beauty formulations, and the rapid expansion of digital beauty retail channels. The resurgence of Y2K-inspired beauty trends, coupled with strong social media influence and celebrity-backed product launches, has significantly revitalized demand for lip gloss products across both developed and emerging markets.

Key Market Insights

- Traditional lip gloss products account for approximately 32% of global market revenue, supported by broad consumer acceptance and affordability.

- High-shine formulations dominate the finish segment with nearly 48% market share, reflecting growing preference for hydrated and natural makeup aesthetics.

- E-commerce has emerged as the fastest-growing distribution channel, accounting for nearly 29% of global sales in 2025.

- North America remains the largest regional market, contributing approximately 31% of global demand, led by the United States.

- Asia-Pacific is the fastest-growing regional market, supported by rising beauty expenditure in China, India, South Korea, and Southeast Asia.

- Hybrid skincare-makeup innovations, including peptide-infused, hyaluronic acid-based, and lip oil-gloss formulations, are reshaping product development strategies.

Lip Gloss Market Trends

Rise of Skincare-Infused Lip Gloss Formulations

The cosmetics industry is witnessing an increasing convergence between skincare and makeup categories. Modern lip gloss products are no longer positioned solely as color cosmetics but are increasingly formulated with active ingredients such as hyaluronic acid, peptides, collagen boosters, ceramides, antioxidants, and botanical oils. Consumers are actively seeking products that deliver hydration, lip repair, anti-aging benefits, and enhanced lip volume while simultaneously providing shine and color. This trend is particularly evident among premium and prestige beauty brands that are positioning lip gloss products as multifunctional beauty solutions. As a result, product differentiation is increasingly centered on ingredient innovation rather than cosmetic appearance alone.

Growth of Clean Beauty and Sustainable Packaging

Consumer demand for ingredient transparency and environmentally responsible products continues to influence purchasing decisions across the global lip gloss market. Vegan, cruelty-free, organic, and clean-label formulations are gaining substantial traction, particularly in North America and Europe. Simultaneously, beauty manufacturers are investing in recyclable materials, refillable packaging systems, and biodegradable applicators to align with sustainability objectives. Consumers increasingly view sustainability credentials as a key factor when evaluating cosmetic purchases, encouraging brands to incorporate environmental stewardship into product development and marketing strategies.

Lip Gloss Market Drivers

Social Media and Influencer-Led Product Adoption

Social media platforms including TikTok, Instagram, YouTube, and emerging beauty-focused content channels have transformed cosmetic purchasing behavior worldwide. Viral beauty trends, influencer endorsements, product reviews, and celebrity collaborations are accelerating product discovery and purchase conversion rates. Lip gloss products frequently achieve rapid market penetration through short-form video content, creating strong demand among younger consumers. The ability of social media to generate immediate product visibility continues to be one of the strongest growth drivers for the lip gloss industry.

Premiumization of Beauty Products

Consumers are increasingly willing to spend on premium beauty products offering superior ingredients, innovative formulations, and luxury branding. Premium lip gloss products featuring advanced hydration technologies, long-wear performance, and sophisticated packaging are gaining market share across North America, Europe, Japan, and South Korea. This trend has enabled manufacturers to improve margins while supporting overall market value growth.

Growing Demand for Multifunctional Cosmetics

The increasing preference for products that combine cosmetic and therapeutic benefits is creating strong demand for multifunctional lip glosses. Consumers are seeking products that provide hydration, shine, UV protection, lip repair, and anti-aging properties within a single formulation. This trend aligns with broader beauty industry movements toward convenience, efficiency, and skincare integration.

Lip Gloss Market Restraints

Intense Market Competition and Brand Fragmentation

The lip gloss market is highly competitive, characterized by the presence of multinational cosmetic companies, independent beauty brands, celebrity-owned brands, and private-label manufacturers. This competitive intensity increases customer acquisition costs and places significant pressure on product differentiation, pricing strategies, and marketing expenditures. Frequent product launches further intensify competition across all price segments.

Raw Material Cost Volatility

Manufacturers remain exposed to fluctuations in the prices of oils, pigments, polymers, specialty chemicals, and sustainable packaging materials. Rising ingredient costs can impact profitability and create challenges in maintaining competitive pricing structures, particularly within mass-market product categories. Supply chain disruptions and inflationary pressures continue to pose risks for global beauty manufacturers.

Lip Gloss Market Opportunities

Expansion of Clean Beauty and Vegan Cosmetics

The accelerating shift toward clean beauty products presents substantial opportunities for both established participants and new market entrants. Consumers increasingly prefer formulations free from parabens, sulfates, phthalates, and synthetic additives. Brands offering vegan, cruelty-free, organic, and environmentally sustainable products are well positioned to capture premium market segments and strengthen customer loyalty. Regulatory support for safer cosmetic ingredients further supports long-term growth prospects in this segment.

Emerging Market Growth Across Asia-Pacific and Middle East

Rapid urbanization, increasing disposable incomes, and expanding beauty-conscious populations are creating significant growth opportunities across emerging economies such as India, China, Indonesia, Vietnam, Saudi Arabia, and the UAE. Demand for both premium and affordable cosmetic products continues to increase as modern retail infrastructure and e-commerce penetration expand. Companies investing in localized product development and region-specific marketing strategies are expected to benefit from these high-growth markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.05 Billion |

| Market Size in 2026 | USD 4.31 Billion |

| Market Size in 2031 | USD 5.91 Billion |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Traditional lip gloss remains the largest product category, accounting for approximately 32% of global market revenue in 2025. These products continue to benefit from broad consumer familiarity, widespread retail availability, and competitive pricing. Tinted lip glosses represent the second-largest segment, driven by demand for products that combine subtle color enhancement with hydration benefits. Lip oil-gloss hybrids are among the fastest-growing categories, reflecting consumer interest in skincare-infused beauty products. Lip plumping glosses have also experienced strong growth due to rising demand for non-invasive beauty enhancement solutions. Organic and vegan formulations continue gaining traction, particularly within premium and luxury product segments.

Finish Type Insights

High-shine lip gloss products dominate the market with approximately 48% share of global revenue, reflecting current beauty trends favoring luminous and hydrated appearances. Satin finish products continue attracting consumers seeking balanced shine and comfort for everyday wear. Glitter and shimmer glosses maintain popularity among younger demographics and special occasion users, while metallic finishes represent a niche category benefiting from fashion and social media-driven trends. Pearl finish products are increasingly incorporated into prestige beauty portfolios targeting mature consumers seeking sophisticated aesthetic effects.

Distribution Channel Insights

E-commerce platforms account for nearly 29% of global lip gloss sales and represent the fastest-growing distribution channel. Online retailing enables brands to leverage influencer marketing, direct-to-consumer strategies, subscription beauty services, and personalized shopping experiences. Specialty beauty retailers continue to hold substantial market share due to product variety and expert consultation services. Drugstores and pharmacies remain important channels for mass-market products, while department stores continue supporting premium and luxury cosmetic brands. Travel retail and duty-free channels are also recovering steadily, particularly in Asia-Pacific and Middle Eastern markets.

Consumer Group Insights

Young adults aged 20–35 years represent the largest consumer segment, accounting for approximately 44% of global demand. This demographic exhibits high engagement with beauty trends, social media content, and premium cosmetic products. Teenagers constitute a significant growth segment due to increasing exposure to beauty influencers and digital marketing campaigns. Consumers aged 36–50 years demonstrate strong demand for premium formulations emphasizing hydration and anti-aging benefits. Meanwhile, mature consumers above 50 years are increasingly adopting treatment-focused lip gloss products formulated with skincare ingredients that support lip health and comfort.

Explore more data points, trends and opportunities Download Free Sample Report

Lip Gloss Market Segmentations

By Product Type

- Traditional Lip Gloss

- Tinted Lip Gloss

- Clear Lip Gloss

- Lip Plumping Gloss

- Shimmer/Glitter Lip Gloss

- Hydrating/Treatment Lip Gloss

- Long-Wear Lip Gloss

- Lip Oil-Gloss Hybrid

- Vegan/Clean Label Lip Gloss

- Organic/Natural Lip Gloss

By Finish Type

- High Shine/Glossy

- Satin Finish

- Glitter Finish

- Metallic Finish

- Pearl Finish

By Distribution Channel

- Supermarkets & Hypermarkets

- Drugstores & Pharmacies

- Specialty Beauty Stores

- Department Stores

- Brand-Owned Stores

- E-Commerce Platforms

- Direct-to-Consumer (DTC)

- Travel Retail/Duty-Free

By Consumer Group

- Teenagers (13–19 Years)

- Young Adults (20–35 Years)

- Adults (36–50 Years)

- Mature Consumers (Above 50 Years)

Regional Insights

North America

North America accounted for approximately 31% of global market revenue in 2025, making it the largest regional market. The United States alone contributed nearly 25% of global demand due to high per-capita cosmetic spending, strong social media influence, and widespread adoption of premium beauty products. Canada also represents a mature market characterized by growing demand for clean beauty and sustainable cosmetic formulations.

Europe

Europe contributed approximately 27% of global market demand, supported by strong beauty industries in France, Germany, the United Kingdom, and Italy. Consumers in the region increasingly prioritize ingredient transparency, sustainability, and premium cosmetic experiences. France remains a leading manufacturing and export hub for prestige beauty products, while Germany represents one of the largest cosmetic consumption markets in Europe.

Asia-Pacific

Asia-Pacific accounted for approximately 29% of global revenue and represents the fastest-growing regional market with an estimated CAGR exceeding 8%. China remains the largest market within the region, followed by Japan, South Korea, and India. Rising disposable incomes, rapid urbanization, increasing beauty awareness, and strong e-commerce penetration continue driving market expansion. South Korea remains particularly influential due to its leadership in cosmetic innovation and beauty trend development.

Latin America

Brazil dominates regional demand within Latin America, supported by one of the world's largest beauty and personal care industries. Mexico and Argentina also contribute significantly to market growth as consumers increasingly adopt premium beauty products and online purchasing channels. Growing middle-class populations continue supporting cosmetic consumption across the region.

Middle East & Africa

The Middle East and Africa region continues to experience steady growth driven by luxury beauty demand in the UAE, Saudi Arabia, and Qatar. Consumers in these markets demonstrate strong preference for premium international cosmetic brands. South Africa remains the largest market in Africa, supported by a growing beauty retail sector and increasing consumer awareness of personal care products.