Firestarter Market Size

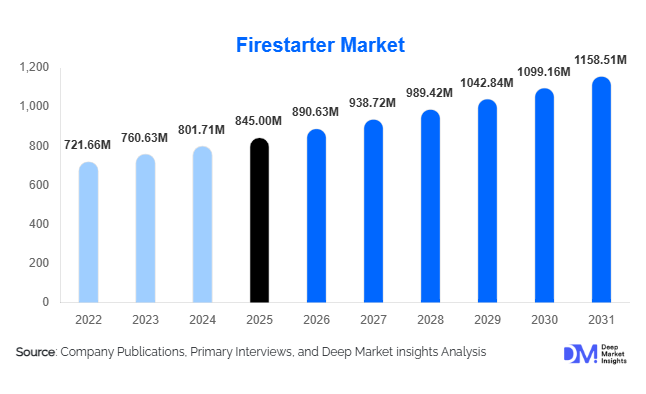

According to Deep Market Insights, the global firestarter market size was valued at USD 845 million in 2025 and is projected to grow from USD 890.63 million in 2026 to reach USD 1,158.51 million by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). The firestarter market growth is primarily driven by increasing participation in outdoor recreational activities, rising demand for residential heating solutions, expanding barbecue and grilling culture, and growing consumer preference for convenient and eco-friendly ignition products. The market continues to evolve with the introduction of sustainable biomass-based firestarters, waterproof survival firestarters, and premium ignition products designed for outdoor enthusiasts and emergency preparedness applications.

Key Market Insights

- Eco-friendly firestarters are gaining significant traction, driven by consumer demand for renewable, biodegradable, and low-emission ignition solutions.

- Outdoor recreation activities such as camping, hiking, and adventure tourism are becoming major demand generators, particularly in North America, Europe, and Asia-Pacific.

- North America dominates the global firestarter market, supported by strong fireplace usage, outdoor cooking culture, and emergency preparedness spending.

- Asia-Pacific is the fastest-growing regional market, driven by increasing disposable income, outdoor recreation adoption, and expanding e-commerce penetration.

- Residential heating remains the largest application segment, accounting for a significant share of global firestarter consumption.

- Technological advancements in firestarter materials, including weather-resistant, odorless, and biomass-derived formulations, are improving product performance and sustainability.

Firestarter Market Trends

Sustainable and Bio-Based Firestarters Witness Rapid Adoption

Environmental awareness among consumers is encouraging manufacturers to develop sustainable firestarter solutions using wood wool, biomass fibers, agricultural residues, and renewable waxes. Traditional petroleum-based products continue to dominate sales volumes; however, bio-based alternatives are experiencing faster growth rates due to tightening environmental regulations and increasing consumer preference for cleaner-burning products. Premium eco-friendly firestarters are gaining popularity across Europe and North America, where sustainability certifications and carbon reduction initiatives influence purchasing decisions. Manufacturers are also investing in recyclable packaging and responsibly sourced raw materials to strengthen their environmental credentials and appeal to environmentally conscious consumers.

Outdoor Recreation and Survival Markets Driving Product Innovation

The growth of camping, overlanding, hiking, hunting, and emergency preparedness activities is reshaping product development strategies within the firestarter market. Consumers increasingly demand compact, waterproof, wind-resistant, and long-lasting ignition products capable of performing in adverse environmental conditions. Ferrocerium rods, magnesium firestarters, and weatherproof ignition cubes are becoming mainstream among outdoor enthusiasts. Digital retail channels have accelerated product visibility, while social media content related to outdoor adventure and survival skills has increased consumer awareness of specialized firestarter products. This trend is expected to stimulate continued innovation and premiumization across the industry.

Firestarter Market Drivers

Growing Participation in Outdoor Recreation Activities

The global increase in camping, hiking, fishing, hunting, and recreational outdoor travel has significantly expanded demand for portable fire ignition products. Firestarters have become essential equipment for outdoor enthusiasts due to their convenience, reliability, and safety advantages compared to traditional ignition methods. Government investments in recreational infrastructure and the rising popularity of nature-based tourism are further contributing to market growth. As outdoor participation expands across emerging economies, firestarter manufacturers are increasingly targeting first-time campers and adventure travelers through specialized product offerings.

Rising Demand for Residential Heating Solutions

Fireplaces, wood stoves, and wood-burning heating systems remain important household heating sources across North America and Europe. Rising energy prices and increasing consumer interest in alternative heating methods continue to support firestarter demand. Modern firestarters provide cleaner ignition, reduced smoke emissions, and improved user convenience, making them preferred solutions for residential heating applications. Seasonal demand peaks during winter months continue to generate strong recurring purchases from homeowners.

Firestarter Market Restraints

Volatility in Raw Material Costs

The industry remains vulnerable to fluctuations in the prices of paraffin wax, wood fibers, biomass feedstocks, packaging materials, and transportation services. Rising raw material costs can compress manufacturer margins and increase product prices, potentially limiting demand growth among price-sensitive consumers. Smaller producers often face greater challenges in absorbing cost increases compared to larger multinational competitors.

Environmental Compliance and Regulatory Challenges

Increasing environmental regulations concerning emissions, chemical additives, and petroleum-derived materials are creating compliance challenges for manufacturers. Product reformulation, certification requirements, and testing procedures increase operating costs and may delay product launches. Companies operating across multiple regions must also comply with varying environmental standards, adding complexity to market expansion strategies.

Firestarter Market Opportunities

Expansion of Eco-Friendly Product Portfolios

The shift toward sustainable consumer products presents significant opportunities for manufacturers developing renewable and biodegradable firestarter solutions. Bio-based products manufactured using agricultural residues, wood fibers, and natural waxes can command premium pricing while addressing growing environmental concerns. Regulatory support for sustainable consumer products is expected to accelerate adoption rates across developed markets, creating long-term growth opportunities for innovative manufacturers.

Growth of Emergency Preparedness and Survival Equipment Markets

Increasing awareness of disaster preparedness, extreme weather events, and emergency readiness is creating new demand for high-performance firestarter products. Government agencies, emergency responders, military organizations, and preparedness-focused consumers increasingly require reliable ignition tools capable of functioning under difficult conditions. Waterproof, long-shelf-life, and weather-resistant firestarters are particularly well positioned to benefit from this emerging demand segment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 845 Million |

| Market Size in 2026 | USD 890.63 Million |

| Market Size in 2031 | USD 1158.51 Million |

| CAGR | 5.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Solid firestarters account for the largest share of the global firestarter market, representing approximately 58% of total revenue in 2025. Their dominance is supported by affordability, ease of transportation, user safety, and broad compatibility with fireplaces, grills, wood stoves, and campfires. Paraffin-based cubes and wax-coated wood fiber firestarters remain the most widely consumed products globally. Liquid firestarters continue to maintain demand within grilling and industrial applications, while gel firestarters are gaining popularity due to cleaner combustion and reduced odor. Ignition rod-based products such as ferrocerium and magnesium firestarters are experiencing rapid adoption among survivalists and outdoor enthusiasts. Electric firestarters, although representing a smaller market segment, are benefiting from increasing adoption in residential and commercial grilling applications due to their convenience and environmentally friendly operation.

Material Composition Insights

Petroleum-based firestarters remain the leading material category, accounting for approximately 46% of global market revenue in 2025 due to their cost-effectiveness and ignition reliability. However, wood-based and biomass-derived alternatives are rapidly gaining market share as consumers seek environmentally sustainable solutions. Wax-based formulations continue to be widely used due to their long burn times and consistent performance characteristics. Bio-based firestarters manufactured using renewable materials are emerging as one of the fastest-growing segments, particularly in Europe where sustainability regulations and eco-conscious purchasing behavior are strongest.

Application Insights

Residential heating and fireplace ignition applications account for approximately 34% of global firestarter demand, making them the largest application segment. Households continue to utilize fireplaces and wood-burning stoves for supplemental heating and recreational purposes. Outdoor recreation and camping represent the fastest-growing application category, driven by rising participation in adventure tourism and outdoor lifestyle activities. Barbecue and grilling applications remain a major source of year-round demand, particularly in North America and Latin America. Emergency preparedness and survival applications are also gaining importance as consumers increasingly invest in disaster readiness equipment and outdoor survival kits.

Distribution Channel Insights

Offline retail channels account for approximately 67% of global firestarter sales, supported by strong distribution through hardware stores, home improvement centers, supermarkets, and outdoor specialty retailers. Consumers frequently purchase firestarters as part of larger shopping trips involving grilling supplies, heating products, and camping equipment. Online retail continues to gain market share through e-commerce platforms, direct-to-consumer websites, and outdoor gear marketplaces. Digital channels are particularly important for premium and specialty firestarter brands targeting outdoor enthusiasts and preparedness-focused consumers. Social media marketing, product demonstrations, and influencer partnerships are increasingly influencing purchasing decisions across online channels.

End User Insights

Households remain the largest end-user segment, accounting for approximately 61% of global firestarter consumption in 2025. Residential users rely on firestarters for fireplaces, wood stoves, outdoor fire pits, and charcoal grilling applications. Outdoor enthusiasts represent the fastest-growing end-user category due to increasing participation in camping, hiking, and overlanding activities. Commercial hospitality operators, including resorts, campgrounds, and restaurants, continue to generate stable demand for premium ignition products. Military organizations, emergency response agencies, and industrial users represent smaller but strategically important segments that require high-performance ignition solutions for specialized applications.

Explore more data points, trends and opportunities Download Free Sample Report

Firestarter Market Segmentations

By Product Type

- Solid Firestarters

- Liquid Firestarters

- Gel Firestarters

- Ignition Rod-Based Firestarters

- Electric Firestarters

By Material Composition

- Petroleum-Based

- Wood-Based Natural Materials

- Biomass & Agricultural Residue-Based

- Wax-Based

- Bio-Based Renewable Materials

By Application

- Residential Heating & Fireplace Ignition

- Outdoor Recreation & Camping

- BBQ & Grilling

- Emergency Preparedness & Survival

- Hospitality & Commercial Food Service

- Industrial Combustion Initiation

By Distribution Channel

- Offline Retail

- Online Retail

By End User

- Households

- Outdoor Enthusiasts

- Commercial Hospitality Operators

- Military & Emergency Agencies

- Industrial Users

Regional Insights

North America

North America accounted for approximately 37% of the global firestarter market in 2025, making it the largest regional market. The United States alone represented nearly 31% of global demand due to widespread fireplace ownership, outdoor grilling culture, and strong participation in camping and recreational activities. Canada contributes significantly through residential heating demand and outdoor recreation spending. Growing preparedness awareness and premium outdoor lifestyle trends continue to support market expansion across the region.

Europe

Europe represented approximately 31% of global market revenue in 2025. Germany, the United Kingdom, France, Sweden, Norway, and the Netherlands are among the region’s largest markets. Demand is supported by residential wood heating, environmental awareness, and growing adoption of sustainable firestarter products. Europe leads the global transition toward bio-based ignition solutions, with consumers increasingly prioritizing low-emission and renewable-material products.

Asia-Pacific

Asia-Pacific accounted for approximately 18% of global market revenue in 2025 and represents the fastest-growing regional market. China, India, Japan, South Korea, and Australia are driving demand growth through increasing participation in outdoor recreation activities and expanding middle-class consumer spending. Rising e-commerce penetration and growing interest in camping culture are further accelerating market development. India is expected to be the fastest-growing country globally, supported by increasing adventure tourism and outdoor leisure participation.

Latin America

Latin America accounted for approximately 8% of global market demand in 2025. Brazil, Mexico, Argentina, and Chile represent the largest markets in the region. Barbecue culture, outdoor cooking traditions, and growing recreational activities continue to support demand for firestarter products. Economic development and expanding retail infrastructure are expected to contribute to steady long-term growth.

Middle East & Africa

The Middle East and Africa represented approximately 6% of global market revenue in 2025. South Africa, Saudi Arabia, the United Arab Emirates, and Turkey are among the key demand centers. Tourism-related hospitality applications, outdoor entertainment activities, and increasing interest in camping and recreational experiences are supporting market growth. The region is also witnessing increased demand for premium outdoor products among higher-income consumer groups.

Key Players in the Firestarter Market

- Swedish Match

- BIC

- SHS Group

- Flame Group

- Duraflame

- Jiffy Products

- Greenfire

- Rutland Products

- Fatwood Firestarter

- Lightning Nuggets

- Diamond Brands

- Weber

- Char-Broil

- Looft

- Ember Products