Feminine Hygiene Products Market Size

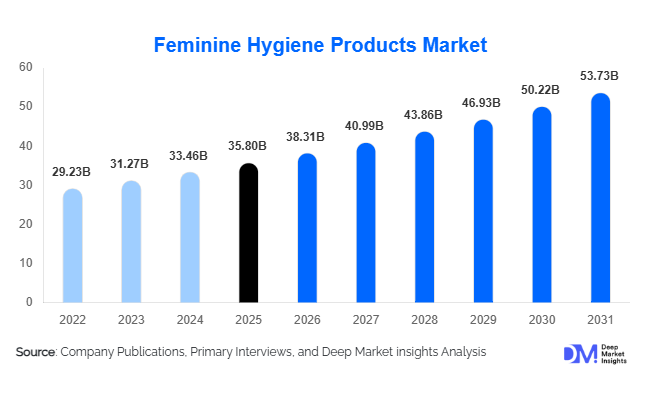

According to Deep Market Insights, the global feminine hygiene products market size was valued at USD 35.8 billion in 2025 and is projected to grow from USD 38.31 billion in 2026 to reach USD 53.73 billion by 2031, expanding at a CAGR of 7.0% during the forecast period (2026–2031). The feminine hygiene products market growth is primarily driven by increasing awareness regarding menstrual health, rising female workforce participation, growing access to personal care products in emerging economies, and the continuous introduction of premium and sustainable hygiene solutions. Government initiatives focused on menstrual equity, expanding retail penetration, and the growing adoption of reusable products such as menstrual cups and period underwear, are further contributing to market expansion. Additionally, evolving consumer preferences toward organic, biodegradable, and skin-friendly products are encouraging manufacturers to invest in innovation and premium product development.

Key Market Insights

- Sanitary pads remain the dominant product category, accounting for nearly 58% of global market revenue due to widespread affordability and accessibility.

- Reusable menstrual products are witnessing the fastest growth, supported by sustainability concerns and increasing consumer awareness regarding environmental impact.

- Asia-Pacific dominates the global market, driven by large population bases, rising disposable incomes, and expanding government-led menstrual hygiene programs.

- India represents one of the fastest-growing national markets, supported by awareness campaigns, public procurement programs, and increasing rural penetration.

- E-commerce and direct-to-consumer channels are rapidly transforming product distribution, enabling new brands to compete with established multinational manufacturers.

- Product innovation in organic cotton, biodegradable materials, and advanced absorbency technologies continues to reshape competitive dynamics across global markets.

Feminine Hygiene Products Market Trends

Sustainable and Eco-Friendly Menstrual Products Gaining Momentum

Sustainability has emerged as one of the most influential trends within the feminine hygiene products industry. Consumers are increasingly seeking alternatives to conventional disposable products due to concerns regarding plastic waste and environmental impact. Manufacturers are responding by launching biodegradable sanitary pads, organic cotton tampons, bamboo-fiber products, reusable cloth pads, menstrual cups, and period underwear. Regulatory support for sustainable consumer products, particularly across Europe and North America, is further accelerating adoption. Several brands are also introducing recyclable packaging and carbon-neutral production initiatives, helping position sustainability as a major differentiating factor within the market.

Premiumization and Wellness-Focused Product Innovation

Consumer purchasing behavior is shifting toward premium products offering enhanced comfort, skin protection, and health benefits. Products marketed as hypoallergenic, fragrance-free, dermatologist-tested, and pH-balanced are experiencing stronger demand than traditional offerings. The feminine hygiene category is increasingly intersecting with the broader women's wellness industry through intimate cleansers, menopause-related hygiene products, and vaginal care solutions. Subscription-based purchasing models and personalized product recommendations are also becoming more prevalent, particularly among younger consumers who prioritize convenience and customized experiences.

Feminine Hygiene Products Market Drivers

Growing Awareness of Menstrual Health and Hygiene

Educational campaigns conducted by governments, healthcare institutions, NGOs, and private companies have significantly improved awareness regarding menstrual hygiene management. Increased discussions surrounding menstrual health have reduced social stigma in many regions and encouraged higher product adoption rates. School-based education programs, public awareness campaigns, and digital health initiatives continue to support long-term market growth by expanding consumer understanding of hygiene practices and product benefits.

Rising Female Workforce Participation and Urbanization

Increasing female employment rates across both developed and emerging economies are contributing to higher demand for convenient and reliable hygiene products. Working women increasingly prefer premium products that provide greater comfort, absorbency, and protection throughout the day. Urbanization further supports market growth by improving access to modern retail infrastructure, healthcare services, and product availability. Growing disposable incomes are also encouraging consumers to trade up from basic hygiene products to premium offerings.

Feminine Hygiene Products Market Restraints

Cultural Barriers and Menstrual Stigma in Developing Regions

Despite significant progress in awareness, menstruation remains a socially sensitive topic in several emerging economies. Cultural taboos, misinformation, and limited access to education continue to restrict product adoption among certain populations. These challenges are particularly evident in rural regions where awareness levels remain comparatively low, limiting market penetration opportunities for manufacturers.

Raw Material Cost Volatility and Pricing Pressure

Manufacturers continue to face challenges associated with fluctuating prices for cotton, wood pulp, superabsorbent polymers, packaging materials, and transportation services. Rising production costs often translate into higher retail prices, which can negatively impact affordability and product accessibility, particularly in price-sensitive markets. Maintaining profitability while ensuring affordability remains a key challenge across the industry.

Feminine Hygiene Products Market Opportunities

Expansion of Sustainable and Reusable Product Categories

The growing demand for environmentally responsible products presents significant opportunities for manufacturers investing in reusable and biodegradable solutions. Menstrual cups, reusable pads, menstrual discs, and period underwear are gaining popularity among environmentally conscious consumers. As governments increasingly support sustainability initiatives and waste reduction policies, manufacturers have opportunities to expand premium eco-friendly product portfolios while improving margins through differentiated offerings.

Government-Led Menstrual Health Programs and Emerging Market Penetration

Emerging economies represent substantial untapped growth potential due to relatively low per-capita product usage compared with developed markets. Government-funded menstrual health initiatives, public procurement programs, and NGO partnerships are improving access to feminine hygiene products among underserved populations. Countries such as India, Indonesia, Nigeria, Bangladesh, and Kenya are expected to generate significant future demand as awareness levels improve and product accessibility expands. Manufacturers that establish localized distribution networks and affordable product portfolios are likely to benefit most from these opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 35.8 Billion |

| Market Size in 2026 | USD 38.31 Billion |

| Market Size in 2031 | USD 53.73 Billion |

| CAGR | 7.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Sanitary pads dominate the feminine hygiene products market, accounting for approximately 58% of total global revenue in 2025. Their widespread availability, affordability, and familiarity among consumers contribute to their leadership position across both developed and emerging markets. Tampons continue to maintain strong demand in North America and Europe, where consumer acceptance is well established. Menstrual cups and menstrual discs are among the fastest-growing categories due to their long-term cost benefits and sustainability advantages. Period underwear is also experiencing robust growth as consumers seek reusable alternatives that combine comfort, convenience, and environmental responsibility. Intimate washes, feminine wipes, and pH-balanced cleansing products are expanding beyond menstrual applications, contributing to broader growth within the feminine wellness segment.

Nature Insights

Disposable products account for approximately 86% of global market revenue and continue to dominate due to convenience, widespread distribution, and established consumer habits. Disposable sanitary pads and tampons remain the most commonly used products worldwide. However, reusable products are experiencing significantly faster growth rates driven by environmental awareness, rising consumer education, and the increasing popularity of sustainable lifestyle choices. Menstrual cups and reusable period underwear are particularly gaining traction among younger consumers seeking long-term value and waste reduction benefits.

Distribution Channel Insights

Supermarkets and hypermarkets represent the largest distribution channel, accounting for nearly 37% of market revenue. Consumers continue to prefer these retail formats due to product variety, competitive pricing, and convenient purchasing experiences. Pharmacies and drug stores remain important channels, particularly for premium and health-focused products. E-commerce is emerging as the fastest-growing channel, supported by subscription services, direct-to-consumer business models, and expanding digital commerce infrastructure. Online platforms enable consumers to access broader product selections, personalized recommendations, and discreet purchasing options, making them increasingly attractive across multiple demographic groups.

Consumer Age Group Insights

Women aged 20–34 years represent the largest consumer segment, accounting for approximately 41% of total market demand. This demographic exhibits high product consumption frequency and demonstrates strong willingness to adopt premium, organic, and innovative products. Teenagers remain a critical consumer segment due to first-time product adoption and increasing menstrual health education initiatives. Women aged 35–49 years contribute substantial demand through recurring product usage and higher purchasing power. The mature women segment, particularly women aged 50 years and above, is increasingly driving demand for menopause-related hygiene products and intimate wellness solutions.

End-Use Insights

Individual consumers account for nearly 88% of total market demand, making them the dominant end-use segment globally. Monthly recurring product consumption and growing awareness regarding feminine health continue to support strong retail demand. Hospitals and maternity centers represent an important institutional segment due to postpartum care requirements and specialized hygiene needs. Educational institutions and government-led distribution programs are expanding rapidly, particularly in emerging economies where menstrual health initiatives are receiving increased policy support. Corporate wellness programs are also emerging as a new application area as employers incorporate feminine hygiene products into workplace health and employee well-being programs.

Explore more data points, trends and opportunities Download Free Sample Report

Feminine Hygiene Products Market Segmentations

By Product Type

- Sanitary Pads/Napkins

- Tampons

- Menstrual Cups

- Period Underwear

- Menstrual Discs

- Panty Liners

- Feminine Wipes

- Intimate Washes & Cleansers

- Intimate Sprays & Deodorants

- Feminine Health & Therapeutic Products

By Nature

- Disposable Products

- Reusable Products

By Distribution Channel

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

- Convenience Stores

- Specialty Health & Beauty Stores

- E-Commerce Platforms

- Direct-to-Consumer (DTC)

- Institutional Procurement

By Consumer Age Group

- Teenagers (10–19 Years)

- Young Adults (20–34 Years)

- Adults (35–49 Years)

- Mature Women (50+ Years)

By End User

- Individual Consumers

- Hospitals & Maternity Centers

- Educational Institutions

- Government & NGO Programs

- Corporate Workplace Wellness Programs

Regional Insights

North America

North America accounts for approximately 26% of the global feminine hygiene products market, led primarily by the United States, which contributes nearly 22% of worldwide demand. High product penetration rates, premium product adoption, and strong consumer awareness support regional leadership. Demand for organic cotton products, reusable menstrual products, and direct-to-consumer brands continues to grow across both the United States and Canada.

Europe

Europe represents approximately 24% of global market revenue and remains one of the most mature feminine hygiene markets worldwide. Germany, the United Kingdom, France, Italy, and Spain account for the majority of regional demand. Consumer preference for sustainable products and strong regulatory emphasis on environmental responsibility are driving adoption of biodegradable and reusable alternatives. Premium products continue to perform particularly well across Western Europe.

Asia-Pacific

Asia-Pacific dominates the global feminine hygiene products market with approximately 39% market share. China, India, Japan, Indonesia, South Korea, and Southeast Asian countries collectively contribute substantial demand due to large female populations and rising incomes. India is among the fastest-growing markets globally, supported by government awareness programs, increasing urbanization, and expanding product accessibility in rural areas. Japan remains a leading premium market characterized by product innovation and advanced hygiene technologies.

Latin America

Latin America accounts for approximately 6% of global demand, with Brazil, Mexico, and Argentina serving as the region's largest markets. Rising urbanization, improving retail infrastructure, and increasing consumer awareness continue to support market expansion. Product affordability remains a key consideration across several Latin American countries, creating opportunities for value-oriented manufacturers.

Middle East & Africa

The Middle East and Africa region represents approximately 5% of global market revenue. Saudi Arabia, the UAE, South Africa, Nigeria, Egypt, and Kenya are among the largest contributors to regional demand. Government initiatives aimed at improving menstrual health access, expanding healthcare infrastructure, and increasing educational awareness are supporting market development. Several African countries are expected to experience above-average growth rates as product accessibility continues to improve.

Key Players in the Feminine Hygiene Products Market

- Procter & Gamble

- Kimberly-Clark Corporation

- Essity AB

- Unicharm Corporation

- Edgewell Personal Care

- Hengan International Group

- Ontex Group

- Kao Corporation

- Johnson & Johnson

- First Quality Enterprises

- TZMO SA

- Natracare

- Rael

- Cora

- The Honest Company