Bearings Market Size

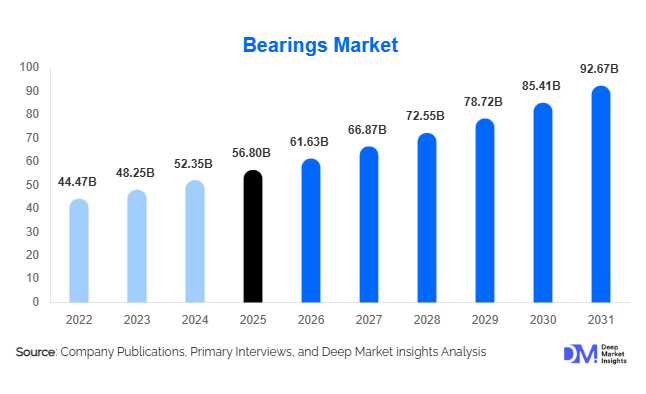

According to Deep Market Insights, the global bearings market size was valued at USD 56.8 billion in 2025 and is projected to grow from USD 61.2 billion in 2026 to reach USD 92.7 billion by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The bearings market growth is primarily driven by increasing industrial automation, expansion of electric vehicle manufacturing, rising investments in renewable energy infrastructure, and growing demand for high-performance rotating equipment across automotive, aerospace, industrial machinery, and power generation sectors. Bearings remain critical components for reducing friction, improving energy efficiency, and enhancing equipment reliability, making them indispensable across virtually all industrial applications involving rotational or linear motion.

Key Market Insights

- Industrial automation and robotics are significantly increasing demand for precision bearings, particularly in smart factories and advanced manufacturing facilities.

- Electric vehicle production is accelerating adoption of high-speed, low-friction bearing technologies, creating new growth opportunities for premium manufacturers.

- Asia-Pacific dominates the global bearings market, led by China, Japan, India, and South Korea due to strong manufacturing and automotive production bases.

- India represents one of the fastest-growing bearing markets globally, supported by industrialization, infrastructure expansion, and government manufacturing initiatives.

- Wind energy installations are emerging as a major demand driver, requiring large-diameter bearings for turbine gearboxes, main shafts, and blade pitch systems.

- Smart bearings integrated with sensors and predictive maintenance capabilities are transforming industrial asset management and improving equipment uptime.

Bearings Market Trends

Smart Bearings and Predictive Maintenance Adoption

Manufacturers and industrial operators are increasingly deploying smart bearings equipped with embedded sensors capable of monitoring vibration, temperature, rotational speed, lubrication condition, and load distribution in real time. These intelligent bearing systems support predictive maintenance strategies that reduce unplanned downtime and maintenance costs while extending equipment life. The trend is particularly prominent in mining, wind energy, aerospace, and industrial automation sectors where equipment failures can result in substantial operational losses. Integration with Industrial IoT platforms is enabling continuous condition monitoring and advanced analytics, allowing operators to transition from reactive maintenance to predictive asset management models.

Growing Adoption of Hybrid and Ceramic Bearings

Demand for hybrid and ceramic bearings is increasing across electric vehicles, aerospace systems, semiconductor manufacturing equipment, and high-speed industrial machinery. Ceramic rolling elements offer advantages such as lower weight, reduced friction, corrosion resistance, and superior performance under extreme operating conditions. As industries prioritize energy efficiency and equipment reliability, manufacturers are investing heavily in advanced material technologies. The trend is also being supported by the growing need for bearings capable of operating in cleanroom environments, high-temperature applications, and electrically insulated systems where traditional steel bearings may face performance limitations.

Bearings Market Drivers

Rapid Expansion of Industrial Automation

The increasing adoption of industrial robots, automated production lines, CNC machinery, and material handling systems is driving significant demand for precision bearings worldwide. Modern automation equipment requires highly reliable bearing systems capable of supporting continuous operation under demanding conditions. Investments in Industry 4.0 initiatives and smart manufacturing facilities are further increasing demand for high-performance bearings across developed and emerging economies. Manufacturing industries continue to prioritize operational efficiency and productivity improvements, positioning bearings as essential components in automation-driven growth.

Growth of Electric Vehicle Manufacturing

The global transition toward electric mobility is creating substantial opportunities for bearing manufacturers. Electric vehicles require specialized bearings capable of operating at higher rotational speeds while minimizing friction and noise. Components such as e-axles, electric motors, transmissions, and battery cooling systems increasingly utilize advanced bearing technologies. As governments worldwide implement emission reduction policies and automakers expand EV production capacity, bearing suppliers are experiencing growing demand for products specifically designed for electrified powertrains and lightweight vehicle architectures.

Bearings Market Restraints

Volatility in Raw Material Prices

Bearings manufacturing depends heavily on high-grade steel, specialty alloys, and advanced ceramics. Price fluctuations in steel and energy markets can significantly impact production costs and profit margins. Since many suppliers operate under long-term contracts with OEMs, passing increased costs directly to customers can be challenging. Persistent volatility in raw material markets remains a major concern for manufacturers seeking to maintain profitability while remaining competitive.

Counterfeit Bearings and Intense Pricing Pressure

The proliferation of counterfeit bearings across aftermarket channels continues to present a significant challenge for established manufacturers. Counterfeit products often fail to meet quality and performance standards, potentially damaging customer confidence and brand reputation. Additionally, increasing competition from low-cost regional suppliers, particularly in developing markets, has intensified pricing pressure throughout the industry. Manufacturers must continuously invest in product authentication technologies and quality assurance measures to differentiate their offerings.

Bearings Market Opportunities

Renewable Energy Infrastructure Expansion

The rapid growth of renewable energy projects, particularly wind power installations, is creating substantial opportunities for bearing manufacturers. Modern wind turbines require large-diameter spherical roller bearings, cylindrical roller bearings, and specialized pitch and yaw bearings capable of operating under extreme loads and environmental conditions. Government-led decarbonization initiatives across Europe, North America, China, and India are expected to drive significant long-term demand for renewable energy-grade bearings. Manufacturers with expertise in high-capacity and high-reliability bearing solutions are well positioned to benefit from this transition.

Smart Factory and Digital Manufacturing Investments

The emergence of digitally connected manufacturing facilities presents opportunities for suppliers offering intelligent bearing solutions. Smart factories increasingly require sensor-enabled bearings that integrate with predictive maintenance systems and industrial analytics platforms. Companies capable of combining hardware expertise with digital monitoring capabilities can generate recurring revenue streams through software subscriptions, maintenance services, and asset performance optimization solutions. This trend is expected to create significant value beyond traditional bearing sales.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 56.8 Billion |

| Market Size in 2026 | USD 61.63 Billion |

| Market Size in 2031 | USD 92.67 Billion |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Ball bearings represent the largest product segment, accounting for approximately 34% of the global bearings market in 2025. Deep groove ball bearings remain particularly dominant due to their versatility, cost-effectiveness, and widespread usage across automotive systems, electric motors, industrial machinery, and consumer appliances. Roller bearings constitute the second-largest category, benefiting from strong demand in heavy industrial applications such as mining, construction equipment, wind turbines, and rail transportation. Specialized bearings, including magnetic, ceramic, and sensor-integrated bearings, are experiencing the fastest growth due to increasing demand from advanced manufacturing, aerospace, semiconductor equipment, and electric vehicle applications. These premium products command higher margins and are becoming increasingly important contributors to overall industry revenue.

Material Insights

Steel bearings continue to dominate the market, accounting for approximately 68% of global demand due to their strength, durability, and cost advantages. Stainless steel bearings maintain strong demand in food processing, pharmaceutical, marine, and chemical processing industries where corrosion resistance is critical. Hybrid bearings combining steel races with ceramic rolling elements are gaining traction in electric vehicles and aerospace applications due to superior performance characteristics. Fully ceramic bearings, while representing a smaller share of the market, are witnessing increased adoption in high-speed, high-temperature, and electrically sensitive environments where conventional materials face limitations.

Distribution Channel Insights

OEM sales account for approximately 61% of global bearings market revenue, driven by strong demand from automotive manufacturers, industrial machinery producers, aerospace OEMs, and renewable energy equipment manufacturers. Original equipment manufacturers prioritize long-term supplier relationships, quality consistency, and technical support, making this channel highly valuable for bearing suppliers. The aftermarket segment continues to represent a substantial revenue opportunity due to replacement demand generated by equipment maintenance cycles. Digital procurement platforms and industrial e-commerce channels are increasingly transforming aftermarket purchasing behavior, improving accessibility and inventory visibility for customers worldwide.

End-Use Industry Insights

Automotive remains the largest end-use industry, contributing approximately 29% of global bearings demand in 2025. Passenger vehicles, commercial vehicles, and electric vehicles collectively require extensive bearing systems throughout engines, transmissions, wheel hubs, and drivetrains. Industrial machinery represents the second-largest application segment, supported by automation investments and manufacturing expansion. Wind energy is emerging as one of the fastest-growing end-use sectors, driven by increasing renewable energy installations globally. Semiconductor manufacturing equipment, robotics, aerospace systems, and medical devices are also becoming increasingly important consumers of high-precision bearing technologies as demand for advanced manufacturing capabilities continues to expand.

Explore more data points, trends and opportunities Download Free Sample Report

Bearings Market Segmentations

By Product Type

- Ball Bearings

- Roller Bearings

- Plain Bearings

- Specialized Bearings

By Material

- Steel Bearings

- Stainless Steel Bearings

- Hybrid Bearings

- Ceramic Bearings

- Polymer/Composite Bearings

- Bronze & Specialty Alloy Bearings

By Load Type

- Radial Bearings

- Axial (Thrust) Bearings

- Combined Load Bearings

By Motion Type

- Rotary Bearings

- Linear Bearings

By Distribution Channel

- OEM Sales

- Aftermarket Sales

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 45% of the global bearings market in 2025, making it the largest regional market. China remains the dominant consumer and producer of bearings globally, supported by its extensive automotive, industrial machinery, renewable energy, and manufacturing sectors. Japan continues to lead in premium and precision bearing technologies, while India is emerging as one of the fastest-growing markets due to rapid industrialization, infrastructure development, and manufacturing expansion initiatives such as Make in India. South Korea and Southeast Asian economies are also contributing significantly to regional growth through investments in electronics manufacturing and industrial automation.

Europe

Europe accounted for approximately 26% of global market demand, driven by strong industrial and automotive sectors in Germany, France, Italy, and the United Kingdom. Germany remains the largest European market due to its advanced manufacturing ecosystem and leadership in automotive engineering. Renewable energy investments, particularly offshore wind projects across Northern Europe, are generating substantial demand for large industrial bearings. The region also maintains a strong position in aerospace and precision engineering applications.

North America

North America represented approximately 21% of global bearings demand in 2025. The United States remains the largest regional market, supported by aerospace, defense, industrial automation, mining, and energy industries. Growing investments in semiconductor manufacturing, electric vehicle production, and industrial reshoring initiatives are creating new opportunities for bearing suppliers. Canada contributes significantly through mining and energy applications, while Mexico benefits from its expanding automotive manufacturing sector.

Latin America

Brazil remains the leading bearings market in Latin America, supported by mining, agriculture, automotive production, and industrial machinery demand. Mexico also contributes significantly through export-oriented manufacturing activities. Infrastructure development and industrial modernization projects are expected to support steady regional growth throughout the forecast period.

Middle East & Africa

The Middle East and Africa region is witnessing increasing bearings demand from oil and gas operations, mining projects, industrial development, and infrastructure investments. Saudi Arabia and the UAE are leading regional demand due to diversification initiatives and industrial expansion programs. South Africa continues to represent a key market because of its extensive mining sector and heavy industrial base.

Key Players in the Bearings Market

- SKF

- Schaeffler AG

- NSK Ltd.

- NTN Corporation

- The Timken Company

- JTEKT Corporation

- Nachi-Fujikoshi Corporation

- MinebeaMitsumi Inc.

- RBC Bearings Incorporated

- C&U Group

- ZWZ Bearing

- LYC Bearing Corporation

- THK Co., Ltd.

- Harbin Bearing Group

- NBC Bearings