Anime Figure Market Size

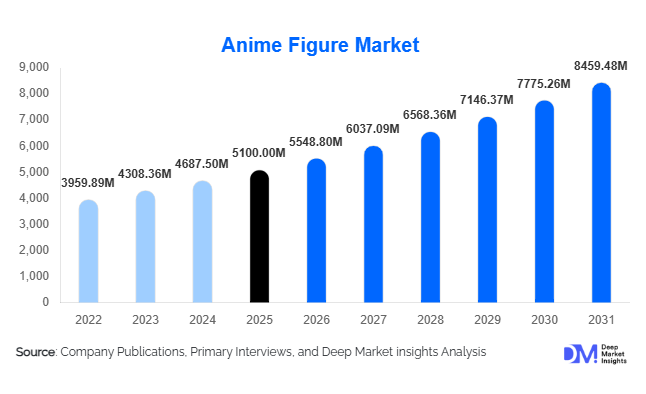

According to Deep Market Insights, the global anime figure market size was valued at USD 5,100 million in 2025 and is projected to grow from USD 5,548.80 million in 2026 to reach USD 8,459.48 million by 2031, expanding at a CAGR of 8.8% during the forecast period (2026–2031). The anime figure market growth is being driven by the globalization of anime content, increasing collector spending, rapid expansion of e-commerce channels, and growing demand for premium licensed collectibles. The increasing popularity of streaming platforms has significantly expanded anime audiences beyond Japan, creating new consumer bases across North America, Europe, Latin America, and emerging Asian markets. As anime franchises continue to generate record-breaking viewership and merchandising revenues, anime figures have evolved from niche collectibles into mainstream entertainment merchandise with strong appeal among both casual consumers and serious collectors.

Key Market Insights

- Scale figures remain the largest product category, accounting for approximately 34% of global market revenue due to superior detailing and premium collector appeal.

- Asia-Pacific dominates the global market, representing nearly 47% of worldwide revenue, supported by Japan's leadership in anime production and merchandise consumption.

- E-commerce platforms are transforming distribution channels, enabling direct global access to Japanese manufacturers and exclusive product releases.

- Premium and ultra-premium collectibles are experiencing the fastest growth, driven by rising demand for limited-edition resin statues and investment-grade collectibles.

- China is emerging as the fastest-growing national market, supported by expanding anime fandom, increasing disposable incomes, and growing collector communities.

- Direct-to-consumer sales models and digital collector ecosystems are improving manufacturer margins while strengthening customer engagement.

Anime Figure Market Trends

Premiumization of Anime Collectibles

The anime figure industry is witnessing significant premiumization as collectors increasingly seek high-end products featuring superior sculpting, detailed paint applications, authenticity certificates, and limited production runs. Manufacturers are expanding their portfolios with premium scale figures, resin statues, and convention-exclusive releases that command substantially higher average selling prices than standard collectibles. Collector demand is shifting toward display-quality products with enhanced craftsmanship and rarity. Companies are responding by introducing numbered editions, premium packaging, and franchise collaborations that create scarcity-driven demand. This trend is particularly visible among adult collectors aged 25–45 years who view premium anime figures as both lifestyle purchases and collectible assets.

Growth of Direct-to-Consumer and Digital Commerce Channels

Manufacturers are increasingly leveraging direct-to-consumer sales channels to improve profitability and strengthen customer relationships. Brand-owned e-commerce platforms, pre-order systems, membership programs, and collector subscription models are becoming common across the industry. These channels provide manufacturers with greater control over inventory planning, customer engagement, and product launches. Digital commerce has also expanded international accessibility, allowing collectors in North America, Europe, Latin America, and Southeast Asia to purchase products directly from Japanese manufacturers. Mobile applications, digital authentication systems, and online collector communities are further enhancing customer experiences while reducing dependence on traditional retail networks.

Anime Figure Market Drivers

Global Expansion of Anime Streaming Platforms

The rapid growth of anime streaming services has dramatically expanded the global anime fan base. International audiences now have immediate access to new anime releases, increasing emotional attachment to characters and franchises. This growing exposure directly supports merchandise purchases, particularly anime figures that allow fans to express fandom and build collections. Successful franchises consistently generate strong figure demand, creating recurring revenue opportunities for manufacturers.

Rising Adult Collector Spending

The market is increasingly supported by adult consumers with significant discretionary income. Unlike traditional toy buyers, adult collectors prioritize authenticity, quality, and exclusivity, often purchasing multiple figures from favored franchises. The emergence of anime collecting as a mainstream hobby has expanded spending on premium products, including scale figures and limited-edition statues. This trend has increased average transaction values and improved industry profitability.

Anime Figure Market Restraints

Increasing Manufacturing and Logistics Costs

Production costs for anime figures continue to rise due to higher prices for PVC, ABS plastics, packaging materials, labor, and international freight services. Rising logistics costs are particularly impactful because a substantial portion of products are manufactured in Asia and distributed globally. These cost pressures often result in higher retail prices, which can limit accessibility among price-sensitive consumers and slow demand growth in emerging markets.

Licensing and Intellectual Property Complexity

The anime figure market relies heavily on licensing agreements with anime studios, publishers, and intellectual property owners. Licensing negotiations, royalty payments, product approval requirements, and regional restrictions increase operational complexity for manufacturers. Delays in approvals or licensing disputes can slow product launches and reduce profitability, particularly for smaller market participants seeking access to popular franchises.

Anime Figure Market Opportunities

Expansion Across Emerging Anime Markets

Emerging economies such as India, Brazil, Indonesia, Vietnam, Saudi Arabia, and Mexico represent significant growth opportunities for anime figure manufacturers. Anime viewership is growing rapidly in these markets through streaming platforms, while physical collectible ownership remains relatively underpenetrated. Localized pricing strategies, regional distribution networks, and direct e-commerce channels can unlock substantial future demand. The increasing popularity of anime conventions and cosplay events in these countries is further strengthening market potential.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5100 Million |

| Market Size in 2026 | USD 5548.80 Million |

| Market Size in 2031 | USD 8459.48 Million |

| CAGR | 8.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Scale Figures accounted for approximately 34% of the global anime figure market revenue in 2025, making them the largest product segment worldwide. Their market leadership is primarily driven by superior craftsmanship, accurate character representation, premium finishing quality, and strong acceptance among serious collectors. Scale figures are typically manufactured in standardized ratios such as 1/4, 1/6, 1/7, and 1/8 scales, enabling collectors to build highly curated franchise collections while maintaining display consistency. The segment also benefits from higher average selling prices, often ranging from USD 120 to more than USD 500 per unit, significantly increasing revenue contribution relative to unit sales.

The growing preference for premium collectibles among adult consumers aged 25–45 years continues to strengthen demand for scale figures. The expansion of globally successful anime franchises such as One Piece, Demon Slayer, Jujutsu Kaisen, Dragon Ball, and Attack on Titan has created sustained demand for highly detailed character recreations. Manufacturers are increasingly introducing limited-production scale figures, exclusive variants, and convention-only releases to capitalize on collector demand and scarcity-driven purchasing behavior.

Action figures remain a significant segment due to their articulated designs and interactive appeal, particularly among younger consumers and gaming enthusiasts. Static figures and prize figures continue to generate strong sales volumes because of their affordability and accessibility to first-time collectors. Meanwhile, Chibi and deformed figures, including Nendoroid-style products, are experiencing robust growth due to lower price points, broad character portfolios, and strong appeal among casual collectors. Premium resin statues are emerging as the fastest-growing category, supported by increasing demand for ultra-premium collectibles, investment-grade products, and highly limited-edition releases that offer both exclusivity and long-term value appreciation potential.

Material Insights

PVC (Polyvinyl Chloride) accounted for approximately 52% of global anime figure market revenue in 2025, maintaining its position as the dominant material segment. PVC's leadership is supported by its optimal balance of durability, flexibility, manufacturing efficiency, and cost-effectiveness. The material allows manufacturers to produce highly detailed sculpts while maintaining competitive production costs, making it suitable for both premium and mass-market product lines. Its compatibility with complex paint applications and intricate character detailing further strengthens its adoption across the industry.

PVC remains the preferred material for most scale figures, static figures, and prize figures because it enables large-scale production without compromising product quality. Additionally, advancements in molding and finishing technologies have significantly improved the ability of PVC-based figures to replicate fine details such as clothing textures, facial expressions, hair strands, and dynamic action poses.

ABS plastic continues to play an important supporting role, particularly in articulated figures and structural components requiring greater rigidity and mechanical strength. Resin-based materials are gaining market share within premium and collector-focused categories because they enable larger-scale production, superior detailing, and enhanced visual aesthetics. The increasing popularity of investment-grade collectibles has accelerated resin adoption among leading manufacturers. Furthermore, hybrid material construction incorporating PVC, ABS, metal reinforcement, magnetic components, and premium surface coatings is becoming increasingly common as manufacturers seek to improve product durability, realism, and collector value.

Distribution Channel Insights

E-commerce platforms represent the largest and fastest-growing distribution channel in the anime figure market, accounting for an estimated 45–50% of global sales. The segment's leadership is driven by the globalization of anime fandom, increasing cross-border trade, and growing consumer preference for online purchasing. Digital platforms provide collectors with access to extensive product catalogs, transparent pricing, international shipping options, pre-order programs, and exclusive product releases that are often unavailable through traditional retail channels.

The rapid growth of anime communities across North America, Europe, Southeast Asia, and Latin America has significantly increased reliance on online retail channels. Dedicated anime merchandise platforms, global marketplaces, and specialty hobby websites have become critical purchasing destinations for collectors seeking limited-edition products and franchise-specific merchandise. The increasing availability of international payment systems and improved global logistics networks has further strengthened online purchasing activity.

Brand-owned direct-to-consumer platforms are gaining market share as manufacturers seek greater control over customer engagement, pricing strategies, and product launches. Direct sales channels also enable companies to collect valuable consumer data and improve demand forecasting. Specialty hobby stores remain highly relevant among enthusiast collectors who prefer physical product inspection, expert guidance, and in-store exclusives. Additionally, anime conventions, collector expos, and fan events continue to serve as influential distribution channels for limited-edition releases and direct fan engagement. The expansion of secondary resale marketplaces is also creating new revenue opportunities as collectors increasingly trade rare and discontinued products.

Collector Type Insights

Enthusiast collectors account for the largest share of anime figure purchases globally, representing an estimated 45% of total market revenue. The segment's dominance is driven by strong franchise loyalty, repeat purchasing behavior, and willingness to invest in premium collectibles. Enthusiast collectors typically maintain long-term collections and actively participate in anime communities, online forums, conventions, and pre-order programs. Their purchasing decisions are influenced by product authenticity, character popularity, production quality, and exclusivity.

The growing mainstream acceptance of anime culture has expanded the enthusiast collector base beyond Japan into North America, Europe, China, and Southeast Asia. Many collectors now view anime figures as lifestyle products and display pieces rather than traditional toys, contributing to increased spending on premium and limited-edition releases.

Casual collectors contribute significant unit sales through entry-level and mid-range product categories, particularly among consumers entering the hobby through mainstream anime franchises. Premium investors represent the fastest-growing collector category, focusing on limited-production figures, convention exclusives, and high-end resin statues with appreciation potential. Meanwhile, institutional collectors, including museums, exhibitions, anime attractions, and cultural centers, represent a niche but expanding segment driven by increasing global recognition of anime as a significant cultural and artistic medium.

End-Use Insights

Individual consumers accounted for approximately 68% of global anime figure market revenue in 2025, making them the dominant end-use segment. Growth is primarily supported by rising anime viewership, expanding collector communities, increasing disposable income among younger demographics, and growing participation in fandom-driven purchasing behavior. The widespread adoption of streaming platforms has significantly increased global anime consumption, directly supporting merchandise demand.

Individual consumers continue to drive demand across both mass-market and premium categories, with purchasing activity increasingly concentrated among adults aged 18–45 years. Social media platforms, collector forums, influencer marketing, and online fan communities have become important catalysts for product discovery and purchasing decisions.

Corporate buyers represent a rapidly growing end-use segment, utilizing anime figures for promotional campaigns, retail merchandising, gaming partnerships, brand collaborations, and entertainment marketing activities. The growing integration of anime intellectual property into gaming, advertising, and consumer products is creating new commercial demand. Additionally, theme parks, anime attractions, entertainment venues, and cultural exhibitions are increasingly incorporating anime collectibles into visitor experiences and retail operations. Export-driven demand remains a critical industry growth factor, with Japan continuing to function as the primary global supplier of licensed anime figures while international consumer markets account for an increasing share of total industry revenue.

Explore more data points, trends and opportunities Download Free Sample Report

Anime Figure Market Segmentations

- Individual Consumers

- Corporate Buyers

- Event Organizers

- Entertainment Venues

- Theme Parks & Attractions

- Museums & Cultural Exhibitions

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 47% of global anime figure market revenue in 2025, making it the largest regional market worldwide. The region benefits from the presence of major anime intellectual property owners, leading manufacturers, established collector ecosystems, and deeply embedded anime culture. Japan remains the industry's largest individual market and serves as the global hub for anime content creation, licensing, figure design, and manufacturing innovation.

Regional growth is being driven by increasing collector spending, expanding anime consumption, and strong merchandise demand across China, South Korea, Taiwan, Thailand, Indonesia, Vietnam, and the Philippines. China represents the fastest-growing national market globally, supported by rising disposable incomes, expanding middle-class consumer spending, strong e-commerce infrastructure, and increasing acceptance of Japanese entertainment content. Southeast Asian markets are benefiting from growing youth populations, improving purchasing power, and expanding access to international anime streaming platforms. The region also benefits from proximity to major manufacturing centers, enabling faster product availability and more competitive pricing.

North America

North America accounted for approximately 26% of global anime figure market revenue in 2025, making it the second-largest regional market. The United States contributes nearly 80% of regional demand and represents the largest anime figure market outside Asia. Market growth is driven by strong anime convention culture, widespread adoption of streaming platforms, increasing collector spending, and expanding acceptance of anime as mainstream entertainment.

Major events such as Anime Expo, Otakon, Anime NYC, and numerous regional conventions have strengthened collector engagement and merchandise purchasing activity. The region also benefits from advanced e-commerce infrastructure, high disposable income levels, and strong demand for premium collectibles. Canada continues to demonstrate steady growth supported by expanding collector communities and increasing availability of licensed merchandise through both online and specialty retail channels.

Europe

Europe represented approximately 18% of global anime figure market revenue in 2025. Growth is supported by increasing consumer interest in Japanese pop culture, rising anime streaming penetration, and expanding distribution networks across major European countries. France remains one of the largest anime consumer markets outside Asia, supported by a long-established manga and anime culture. Germany leads demand for premium collectibles due to strong purchasing power and an established hobby collectibles market.

The United Kingdom, Italy, Spain, and the Netherlands are also experiencing growing collector activity driven by expanding anime communities and increased participation in fan conventions. The region's mature e-commerce ecosystem, efficient import infrastructure, and growing acceptance of Japanese entertainment content continue to support market expansion. Europe is expected to remain one of the fastest-growing import markets for premium anime collectibles during the forecast period.

Latin America

Latin America is emerging as a high-potential growth region, led primarily by Brazil and Mexico, which collectively account for the majority of regional demand. Long-standing popularity of anime franchises such as Dragon Ball, Naruto, Saint Seiya, and One Piece has created a strong cultural foundation for anime merchandise consumption. Growth is increasingly supported by expanding e-commerce platforms, improved access to imported products, and rising participation in anime conventions and cosplay events.

Economic development, increasing internet penetration, and growing youth demographics are helping expand the regional collector base. Improvements in cross-border logistics and international shipping networks are also enhancing product availability, enabling collectors greater access to officially licensed merchandise. As disposable incomes continue to rise, demand for mid-range and premium collectibles is expected to increase significantly.

Middle East & Africa

The Middle East & Africa accounted for approximately 4% of global anime figure market revenue in 2025 but represents one of the fastest-emerging growth regions. Saudi Arabia and the United Arab Emirates are leading regional demand due to rising disposable incomes, growing youth populations, government investments in entertainment industries, and increasing popularity of anime and gaming culture.

National initiatives aimed at expanding entertainment ecosystems, including large-scale gaming festivals, anime conventions, and cultural events, are helping create new demand for licensed merchandise. The UAE serves as a major regional distribution and retail hub, facilitating access to international anime products. South Africa remains the most developed collector market within Africa, supported by established hobby communities and growing online retail penetration. Continued investments in entertainment infrastructure and youth-focused consumer industries are expected to support long-term regional market growth.

Key Players in the Anime Figure Market

- Bandai Namco Holdings

- Good Smile Company

- Kotobukiya

- Aniplex

- Max Factory

- Alter

- MegaHouse

- Kadokawa

- FREEing

- Phat Company

- Prime 1 Studio

- eStream

- Myethos

- Hobby Max

- Tsume Art