Wood Pallet Market Size

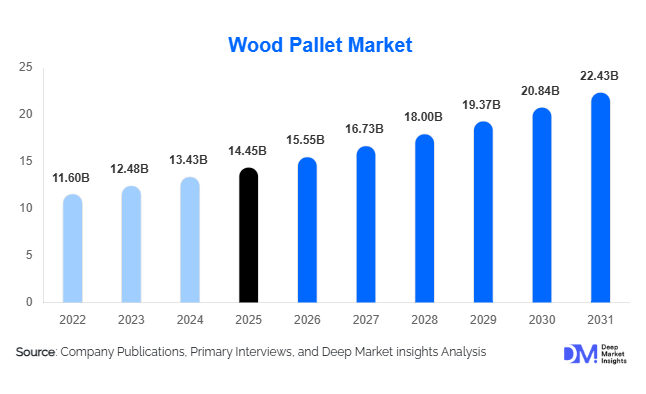

According to Deep Market Insights, the global wood pallet market size was valued at USD 14.45 billion in 2025 and is projected to grow from USD 15.08 billion in 2025 to reach USD 18.95 billion by 2031, expanding at a CAGR of 4.6% during the forecast period (2025–2031). The wood pallet market growth is primarily driven by rising global trade volumes, expanding warehousing infrastructure, increasing e-commerce fulfillment activities, and sustained demand from manufacturing and logistics industries. Wood pallets remain the preferred material handling solution globally due to their low cost, ease of repair, recyclability, and compatibility with international shipping requirements. The growing emphasis on sustainable logistics practices and circular supply chains is further supporting market expansion. Heat-treated and ISPM-15-compliant pallets are witnessing strong adoption among export-oriented industries, particularly in Asia-Pacific, North America, and Europe. Furthermore, technological advancements such as RFID-enabled tracking systems, smart pallet management platforms, and automated pallet repair facilities are enhancing operational efficiency across supply chains, contributing to long-term market growth.

Key Market Insights

- Wood pallets account for nearly 90% of global pallet shipments by volume, maintaining dominance due to affordability, repairability, and widespread availability.

- Heat-treated pallets represent over 55% of global demand, driven by international trade regulations and ISPM-15 compliance requirements.

- Asia-Pacific dominates the global wood pallet market, accounting for approximately 39% of total revenue, led by China, India, Japan, and Southeast Asian manufacturing hubs.

- North America remains a major demand center, supported by advanced logistics infrastructure, pallet pooling networks, and large-scale warehousing operations.

- Reusable and returnable pallet systems are gaining traction, helping companies reduce logistics costs and achieve sustainability targets.

- Smart pallet technologies, including RFID, IoT sensors, and digital asset tracking platforms, are transforming pallet management across global supply chains.

Wood Pallet Market Trends

Expansion of Circular Pallet Pooling Networks

One of the most significant trends shaping the wood pallet market is the rapid expansion of pallet pooling and circular logistics systems. Major retailers, FMCG companies, and logistics providers are increasingly shifting from one-way pallet purchases toward pooled and reusable pallet networks. These systems improve asset utilization, reduce transportation costs, and support sustainability initiatives by extending pallet life cycles. Large pooling operators continue to expand their depot infrastructure and recovery networks across North America, Europe, and Asia-Pacific. Companies are increasingly adopting standardized pallet fleets that can be repaired, redistributed, and reused multiple times, significantly lowering environmental impact and improving supply chain efficiency.

Digitalization and Smart Pallet Adoption

The integration of digital technologies into pallet management is becoming a major industry trend. RFID-enabled pallets, GPS tracking devices, and cloud-based asset management platforms are providing real-time visibility across supply chains. Smart pallets help reduce asset loss, improve inventory accuracy, optimize warehouse operations, and support predictive maintenance programs. Industries such as pharmaceuticals, food & beverage, automotive, and retail are increasingly adopting digital pallet solutions to enhance traceability and improve operational efficiency. As warehouse automation expands globally, demand for technologically advanced pallet systems is expected to accelerate further during the forecast period.

Wood Pallet Market Drivers

Growth in Global Trade and Logistics Activities

The continuous expansion of international trade remains a primary driver for the wood pallet market. Increasing movement of goods across manufacturing, retail, agriculture, and industrial sectors requires reliable material handling solutions. The growth of global containerized shipping, warehousing infrastructure, and distribution networks has directly increased pallet demand. Export-oriented economies such as China, India, Vietnam, Germany, and Mexico continue to generate significant demand for ISPM-15-compliant wood pallets used in international trade. Rising investments in logistics parks, industrial corridors, and transportation infrastructure are further strengthening market growth.

E-Commerce and Warehouse Expansion

The rapid growth of e-commerce has significantly increased pallet utilization across fulfillment centers and distribution warehouses. Large retailers and third-party logistics providers rely heavily on palletized material handling systems to manage inventory efficiently. The rise of automated warehouses has increased demand for standardized pallet designs capable of supporting robotic systems and automated storage solutions. Expanding online retail activities in North America, Europe, China, India, and Southeast Asia continue to create long-term growth opportunities for wood pallet manufacturers.

Wood Pallet Market Restraints

Volatility in Lumber and Timber Prices

The wood pallet industry remains highly dependent on the availability and pricing of lumber. Fluctuations in timber prices caused by supply chain disruptions, forestry regulations, labor shortages, and transportation costs can significantly impact manufacturer profitability. Rising raw material costs often create pricing pressure across the value chain, making cost management a key challenge for market participants.

Increasing Competition from Plastic and Composite Pallets

Plastic pallets continue gaining adoption in industries that require superior hygiene, moisture resistance, and long operational life. Pharmaceutical, food processing, and healthcare sectors increasingly evaluate plastic alternatives due to stricter cleanliness standards. Although wood pallets maintain a cost advantage, growing adoption of alternative pallet materials may constrain growth in certain high-value applications.

Wood Pallet Market Opportunities

Growth of Export-Oriented Manufacturing Hubs

Rapid industrialization across Asia-Pacific, Latin America, and Eastern Europe is creating substantial opportunities for wood pallet manufacturers. Countries such as India, Vietnam, Indonesia, Poland, and Mexico continue attracting foreign manufacturing investments due to favorable labor costs and export competitiveness. These industries require large volumes of export-grade pallets for international shipments. Manufacturers capable of supplying heat-treated and ISPM-15-certified pallets are expected to benefit significantly from this trend.

Expansion of Smart Pallet Solutions

The increasing adoption of digital supply chain management systems presents substantial opportunities for value-added pallet solutions. Smart pallets equipped with RFID tags, IoT sensors, and real-time monitoring capabilities enable improved tracking, inventory visibility, and asset utilization. As logistics operators seek greater operational efficiency, pallet manufacturers offering integrated technology solutions can command premium pricing and strengthen customer relationships.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14.45 Billion |

| Market Size in 2026 | USD 15.55 Billion |

| Market Size in 2031 | USD 22.43 Billion |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Design Type Insights

Block wood pallets dominated the global wood pallet market, accounting for approximately 68% of total revenue in 2025. Their leadership position is primarily driven by superior structural strength, four-way forklift accessibility, higher load-bearing capacity, and compatibility with increasingly automated warehousing and distribution systems. As logistics operators and manufacturers continue investing in warehouse automation, robotic material handling, and high-throughput distribution centers, demand for block pallets has accelerated globally. These pallets offer greater durability and operational efficiency than traditional stringer pallets, making them the preferred choice across logistics, food & beverage, FMCG, retail, and export-oriented industries.

The rapid expansion of global trade and pallet pooling programs has further strengthened adoption of block pallets due to their longer service life and ease of repair. In Europe, EPAL-standard block pallets remain the industry benchmark for cross-border logistics operations, while North American retailers are increasingly adopting block pallet systems to improve supply chain standardization.

Stringer pallets continue to maintain a significant market presence, particularly across North America, owing to their lower manufacturing costs and widespread compatibility with conventional warehousing infrastructure. Meanwhile, demand for custom industrial pallets is steadily increasing across automotive, aerospace, machinery, defense, and heavy equipment sectors where specialized load dimensions, weight capacities, and transportation requirements necessitate customized pallet solutions. Growing investments in industrial manufacturing and heavy engineering projects are expected to create additional opportunities for customized pallet designs during the forecast period.

Wood Species Insights

Softwood pallets accounted for nearly 60% of global market revenue in 2025, making them the leading wood species segment. Their dominance is supported by abundant raw material availability, lower production costs, lighter weight characteristics, and faster replenishment cycles compared to hardwood species. Pine remains the most widely utilized softwood globally due to its favorable strength-to-weight ratio, ease of processing, and extensive availability across major timber-producing regions including North America, Scandinavia, and Asia-Pacific.

The growing emphasis on cost optimization among pallet manufacturers and end-users continues to support softwood adoption. Softwood pallets are particularly preferred in logistics, retail distribution, agriculture, food processing, and export packaging applications where weight reduction can contribute to lower transportation costs. Additionally, sustainable forestry practices and certified timber sourcing programs have strengthened the environmental appeal of softwood-based pallet production.

Hardwood pallets account for approximately 40% of market revenue and remain critical in applications requiring enhanced durability, impact resistance, and load-bearing performance. Industries such as automotive manufacturing, metals processing, chemicals, construction materials, and heavy industrial equipment frequently utilize hardwood pallets due to their ability to withstand demanding operating conditions and repeated handling cycles. As industrial production expands globally, demand for high-strength hardwood pallet solutions is expected to remain stable.

Treatment Type Insights

Heat-treated pallets represent the leading treatment segment, accounting for approximately 55% of global market demand in 2025. Their market leadership is directly linked to growing international trade volumes and mandatory compliance with International Standards for Phytosanitary Measures (ISPM-15). Heat treatment eliminates pests and biological contaminants without the use of chemicals, making these pallets suitable for cross-border transportation and export shipments.

The continued expansion of global manufacturing supply chains and export-oriented industries in China, India, Vietnam, Mexico, and Eastern Europe has significantly increased demand for heat-treated pallets. Exporters increasingly prioritize internationally compliant pallet solutions to avoid customs delays, shipment rejections, and regulatory penalties. As global trade networks become more interconnected, heat-treated pallets are expected to maintain their dominant market position.

Kiln-dried pallets are witnessing growing adoption due to their moisture reduction capabilities, improved dimensional stability, and lower risk of fungal growth during storage and transportation. These pallets are particularly preferred in food processing, pharmaceuticals, electronics, and high-value manufacturing applications. Untreated pallets continue to serve domestic logistics operations where international phytosanitary requirements do not apply, offering a cost-effective solution for local transportation and warehousing needs.

End-Use Industry Insights

Logistics and transportation remained the largest end-use industry, accounting for approximately 31% of global wood pallet market revenue in 2025. The segment's leadership is driven by the continuous expansion of warehousing infrastructure, freight transportation networks, third-party logistics services, and international trade activities. Virtually every supply chain relies on palletized handling systems for efficient storage, transportation, and inventory management, making logistics the largest consumer of wood pallets globally.

The rapid growth of e-commerce fulfillment centers, distribution hubs, and cold-chain logistics facilities has further accelerated pallet demand across developed and emerging economies. Increasing investments in automated warehouses and high-volume distribution networks are driving demand for standardized pallet systems compatible with robotic handling equipment.

Food and beverage industries represent another major demand center due to extensive requirements for product storage, transportation, export packaging, and retail distribution. Retail and e-commerce applications are emerging as the fastest-growing end-use segment, supported by double-digit growth in online retail activity across Asia-Pacific, North America, and Europe. Meanwhile, pharmaceutical, automotive, agriculture, chemicals, and electronics industries continue to generate strong pallet demand as global supply chains become increasingly integrated, export-oriented, and reliant on efficient material handling infrastructure.

Usage Model Insights

Returnable and reusable pallet systems accounted for approximately 46% of global market revenue in 2025, making them the leading usage model segment. Their growing adoption is driven by increasing corporate focus on sustainability, circular economy initiatives, and long-term logistics cost optimization. Large manufacturers, retailers, and logistics providers are increasingly shifting away from single-use pallet systems toward reusable fleets that reduce material consumption, waste generation, and replacement costs.

The expansion of pallet pooling services has significantly strengthened demand for reusable pallet systems. Pooling operators enable companies to access pallet assets without large upfront capital investments while improving asset utilization rates across supply chains. This model has gained significant traction across FMCG, food & beverage, consumer goods, and retail industries where pallet circulation volumes are high.

One-way pallets continue to maintain substantial demand in export-oriented applications where pallet retrieval is economically impractical. However, growing environmental regulations and sustainability targets are encouraging organizations to transition toward reusable and pooled pallet systems. Rental and pooling services are expected to remain among the fastest-growing segments as companies increasingly prioritize operational flexibility, asset efficiency, and carbon footprint reduction.

Explore more data points, trends and opportunities Download Free Sample Report

Wood Pallet Market Segmentations

By Design Type

- Block Wood Pallets

- Stringer Wood Pallets

- Engineered/Molded Wood Pallets

- Custom Industrial Wood Pallets

By Wood Species

- Softwood Pallets

- Hardwood Pallets

By Treatment Type

- Heat-Treated Pallets

- Kiln-Dried Pallets

- Chemically Treated Pallets

- Untreated Pallets

By Usage Model

- One-Way/Expendable Pallets

- Returnable/Recyclable Pallets

- Rental/Pooled Pallets

By Load Capacity

- Light-Duty Pallets

- Medium-Duty Pallets

- Heavy-Duty Pallets

By End-Use Industry

- Logistics & Transportation

- Food & Beverage

- Retail & E-Commerce

- Manufacturing

- Automotive

- Chemicals & Petrochemicals

- Pharmaceuticals & Healthcare

- Agriculture & Forestry

- Construction Materials

- Consumer Goods & FMCG

- Electronics & Electricals

Regional Insights

Asia-Pacific

Asia-Pacific led the global wood pallet market with approximately 39% of total revenue in 2025 and is expected to remain the fastest-growing regional market throughout the forecast period. The region's dominance is supported by its position as the world's largest manufacturing and export hub. China alone accounts for nearly 18% of global demand, driven by extensive manufacturing output, export activities, and large-scale logistics infrastructure. India contributes approximately 6% of global demand and is benefiting from initiatives such as Make in India, dedicated freight corridors, industrial corridor developments, and rapid warehouse construction.

Additional growth drivers include rising foreign direct investment (FDI) in manufacturing, expanding e-commerce ecosystems, increasing containerized trade volumes, and growing export-oriented production across Vietnam, Indonesia, Thailand, Malaysia, and South Korea. The ongoing diversification of global supply chains away from single-country sourcing strategies is creating substantial demand for export-grade heat-treated pallets throughout the region.

North America

North America accounted for approximately 27% of global market revenue in 2025, with the United States representing nearly 23% of worldwide demand. Regional growth is primarily driven by advanced warehousing infrastructure, strong domestic consumption, robust retail distribution networks, and widespread adoption of pallet pooling systems. The United States remains one of the largest pallet-consuming markets globally due to extensive logistics operations supporting e-commerce, food distribution, manufacturing, and consumer goods sectors.

Growth is further supported by increasing warehouse automation investments, rising demand for sustainable packaging solutions, and continued expansion of third-party logistics providers. Mexico is emerging as a particularly important growth market due to nearshoring trends, automotive manufacturing investments, and increasing exports to the United States. Canada benefits from strong forestry resources, manufacturing activity, and cross-border trade integration.

Europe

Europe accounted for approximately 25% of global market revenue in 2025 and remains one of the most standardized and mature pallet markets worldwide. Germany leads regional demand with nearly 7% of global consumption, supported by its strong industrial manufacturing base, export-oriented economy, and advanced logistics infrastructure. France, the United Kingdom, Italy, Spain, Poland, and the Netherlands also represent major consumption centers.

Regional growth is supported by extensive adoption of EPAL-standard pallets, strong cross-border trade activity, circular economy initiatives, and stringent sustainability regulations. The increasing emphasis on reusable packaging systems and carbon reduction targets has accelerated investment in pallet repair, recycling, and pooling networks throughout Europe. Growth in e-commerce logistics and pharmaceutical supply chains is further contributing to pallet demand across the region.

Latin America

Latin America represented approximately 5% of global market demand in 2025, led primarily by Brazil and Mexico. The region's growth is closely linked to agricultural exports, food processing industries, forestry products, and expanding manufacturing activities. Brazil remains the largest market due to its significant agricultural export sector, including soybeans, coffee, sugar, meat products, and processed foods that require palletized transportation and storage.

Mexico continues to benefit from rising industrial investments, export manufacturing growth, and integration with North American supply chains. Additional growth drivers include increasing warehouse development, modernization of logistics infrastructure, and government initiatives supporting industrial competitiveness. Export-oriented industries are expected to remain the primary catalyst for future pallet demand throughout the region.

Middle East & Africa

The Middle East & Africa accounted for approximately 4% of global market revenue in 2025 but is emerging as a strategically important growth market. Saudi Arabia, the United Arab Emirates, and South Africa represent the largest regional markets due to ongoing industrial diversification programs, logistics hub development, and major infrastructure investments.

Key growth drivers include Saudi Arabia's Vision 2031 initiative, expansion of free trade zones across the Gulf region, increasing port capacities, growth in food imports, and rising investments in manufacturing and warehousing infrastructure. The UAE continues strengthening its position as a global logistics gateway connecting Asia, Europe, and Africa. Meanwhile, South Africa remains an important market due to mining, manufacturing, agriculture, and export logistics activities. Continued industrialization and infrastructure development are expected to support long-term pallet demand across the region.

Key Players in the Wood Pallet Market

- Brambles Limited (CHEP)

- PECO Pallet

- PalletOne

- Kamps Inc.

- Loscam

- UFP Industries

- Millwood Inc.

- Kronus

- Treyer Paletten

- Falkenhahn AG

- John Rock

- Mid Cork Pallets & Packaging

- Nefab Group

- SAS Group

- Hazelhill Timber Products