Kids Smartwatch Market Size

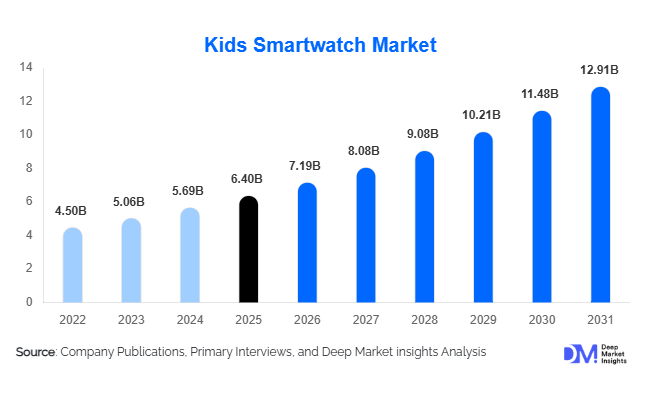

According to Deep Market Insights, the global Kids Smartwatch Market size was valued at USD 6.4 billion in 2025 and is projected to grow from USD 7.19 billion in 2026 to reach USD 12.91 billion by 2031, expanding at a CAGR of 12.4% during the forecast period (2026–2031). The market is witnessing robust growth due to rising parental concerns regarding child safety, increasing adoption of connected wearable devices, and growing demand for communication-enabled alternatives to smartphones for children. Advancements in GPS tracking, geofencing technology, real-time communication features, and health monitoring capabilities have transformed kids smartwatches from basic tracking devices into multifunctional wearable ecosystems. Growing digitalization across households, expanding 4G/5G connectivity infrastructure, and declining component costs are further accelerating market penetration globally.

Key Market Insights

- Child safety and GPS tracking applications account for the largest share of demand, with parents increasingly prioritizing real-time location monitoring and emergency communication capabilities.

- Standalone cellular-enabled smartwatches dominate the market, offering independent connectivity through LTE and eSIM technologies without requiring continuous smartphone pairing.

- Asia-Pacific leads global demand, supported by a large child population, expanding middle-class households, and strong domestic manufacturing ecosystems.

- India represents the fastest-growing country market, driven by increasing disposable incomes, rapid smartphone ecosystem adoption, and rising awareness of child safety technologies.

- Online retail channels account for the majority of global sales, benefiting from product variety, competitive pricing, and growing consumer preference for digital purchasing.

- Artificial intelligence, health monitoring, and educational integration are emerging as major innovation areas, creating opportunities for subscription-based services and ecosystem expansion.

Kids Smartwatch Market Trends

AI-Powered Child Safety Features Becoming Mainstream

Manufacturers are increasingly integrating artificial intelligence into kids smartwatches to improve child safety and parental monitoring capabilities. Modern devices are evolving beyond traditional GPS tracking by incorporating predictive location alerts, behavior-based notifications, intelligent geofencing, and anomaly detection systems. AI-enabled monitoring allows parents to receive contextual alerts based on children's movement patterns, enhancing preventive safety measures. As wearable technology ecosystems mature, manufacturers are also exploring machine learning-based emergency response systems and automated risk assessments. These innovations are expected to improve user engagement while creating recurring subscription-based revenue opportunities for vendors.

Expansion of Health and Educational Functionalities

Kids smartwatches are increasingly incorporating health tracking and educational applications, expanding their value proposition beyond safety and communication. Features such as activity monitoring, sleep tracking, step counting, and heart rate measurement are becoming standard across mid-range and premium devices. Simultaneously, educational content including language learning, interactive quizzes, and classroom communication functions are being integrated into smartwatch ecosystems. Schools and parents are increasingly viewing smartwatches as controlled digital devices that provide connectivity while minimizing distractions associated with smartphones. This trend is expected to drive adoption among educational institutions and family-oriented consumers worldwide.

Kids Smartwatch Market Drivers

Increasing Parental Focus on Child Safety

Growing concerns regarding child security remain the strongest growth driver for the kids smartwatch market. Parents increasingly seek technologies that provide real-time location visibility, emergency communication, and geofencing alerts to monitor children's activities. Smartwatches equipped with GPS tracking, SOS emergency buttons, and voice communication capabilities offer peace of mind while allowing children greater independence. As urbanization continues and dual-income households become more prevalent globally, demand for wearable child safety solutions is expected to increase substantially.

Rapid Adoption of Wearable Technology

The broader wearable technology industry has experienced significant growth over the past decade, creating favorable conditions for kids-specific wearable devices. Increased consumer familiarity with smartwatches among adults has improved acceptance of similar products for children. Technological advancements in battery life, sensor capabilities, connectivity modules, and display technologies have enhanced product performance while reducing manufacturing costs. These developments continue to support widespread adoption across both developed and emerging markets.

Kids Smartwatch Market Restraints

Data Privacy and Cybersecurity Concerns

Despite strong growth prospects, concerns regarding data security and privacy remain significant challenges for the market. Kids smartwatches collect sensitive information including real-time location data, communication records, and behavioral information. Regulatory frameworks governing child data protection continue to evolve across North America, Europe, and Asia-Pacific, requiring manufacturers to invest heavily in cybersecurity infrastructure and compliance measures. Failure to adequately protect user information may negatively impact consumer trust and adoption rates.

Competition from Smartphones and Alternative Devices

As children age, many households transition directly from kids smartwatches to smartphones, limiting long-term product retention. Smartphones offer broader functionality, including social media access, internet connectivity, and entertainment features, making them attractive alternatives for older children. This transition creates challenges for smartwatch manufacturers seeking to extend product lifecycles and maintain customer engagement throughout adolescence.

Kids Smartwatch Market Opportunities

Expansion Across Emerging Economies

Emerging markets present substantial growth opportunities for kids smartwatch manufacturers. Countries such as India, Indonesia, Vietnam, Brazil, Saudi Arabia, and Mexico continue to exhibit relatively low penetration rates compared with developed markets. Rising household incomes, growing awareness of child safety technologies, expanding internet connectivity, and increasing adoption of digital devices create favorable market conditions. Manufacturers that develop affordable devices tailored to regional consumer preferences can capture significant market share in these high-growth economies.

Education and School-Based Smartwatch Adoption

Educational institutions are emerging as a promising opportunity within the kids smartwatch ecosystem. Schools increasingly seek communication solutions that allow connectivity while minimizing distractions associated with smartphones. Smartwatches equipped with attendance tracking, emergency alerts, controlled communication functions, and educational applications can support school safety initiatives and digital learning programs. Partnerships between device manufacturers, schools, and government agencies may create large-scale institutional procurement opportunities over the coming years.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.4 Billion |

| Market Size in 2026 | USD 7.19 Billion |

| Market Size in 2031 | USD 12.91 Billion |

| CAGR | 12.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Architecture Insights

Standalone kids smartwatches accounted for approximately 58% of global market revenue in 2025, making them the leading product architecture segment worldwide. The segment's dominance is primarily driven by growing parental demand for independent child connectivity and safety monitoring without providing children unrestricted access to smartphones. Standalone devices incorporate integrated LTE/4G connectivity, eSIM capabilities, GPS tracking, voice calling, messaging, geofencing, and SOS emergency functions, enabling children to remain connected even when separated from parents.

The increasing preference for digital parenting solutions has significantly strengthened demand for standalone models, particularly in North America, China, Japan, South Korea, and Western Europe. Parents increasingly view these devices as a transitional technology between traditional feature phones and smartphones. Furthermore, improvements in battery efficiency, miniaturized communication modules, and declining cellular chipset costs have enhanced affordability and performance. The growing deployment of eSIM technology by telecom operators is also simplifying activation processes and reducing hardware dependency, further accelerating adoption. As manufacturers continue integrating AI-powered safety monitoring, video calling, and health-tracking functions, standalone smartwatches are expected to maintain their leadership position throughout the forecast period.

Connectivity Technology Insights

Cellular-enabled smartwatches represented approximately 49% of total market revenue in 2025, emerging as the leading connectivity segment globally. The segment benefits from consumers' increasing preference for always-connected wearable devices that support real-time communication and location tracking independent of Wi-Fi networks. Cellular connectivity enables uninterrupted GPS tracking, emergency communication, voice calling, and parental monitoring, making it particularly valuable for school-going children and active families.

The widespread rollout of 4G LTE networks and the growing commercialization of affordable eSIM solutions have significantly enhanced the attractiveness of cellular-enabled devices. Telecom operators in major markets such as the United States, China, Germany, Japan, South Korea, and Australia increasingly offer dedicated smartwatch data plans, supporting adoption. Additionally, parents increasingly prioritize reliable connectivity during outdoor activities, school commutes, and extracurricular programs, creating sustained demand for cellular-based devices. Although Wi-Fi and Bluetooth variants remain popular within entry-level price categories, their limited functionality compared to cellular models continues to reinforce the leadership of the cellular segment. Hybrid connectivity solutions combining LTE, Wi-Fi, and Bluetooth are expected to gain momentum as manufacturers focus on improving user experience and battery optimization.

Application Insights

Child safety and tracking applications accounted for approximately 38% of global market revenue in 2025, making them the largest application segment within the kids smartwatch market. The segment's leadership is directly linked to increasing parental concerns regarding child security, independent mobility, and emergency preparedness. Features such as GPS tracking, geofencing alerts, location history monitoring, one-touch SOS functions, safe zone notifications, and real-time parental monitoring continue to represent the primary purchasing criteria across both developed and emerging markets.

The rising number of dual-income households globally has further strengthened demand for child safety technologies, as working parents seek reliable methods to monitor children's whereabouts throughout the day. In addition, growing urbanization and increased participation in after-school activities have elevated the importance of real-time communication and location awareness. The segment is also benefiting from technological advancements including AI-powered location analytics, predictive safety alerts, and intelligent emergency response systems. While communication, fitness monitoring, educational applications, and entertainment functions continue to expand market opportunities, safety-centric use cases remain the core value proposition driving smartwatch adoption worldwide.

Price Tier Insights

Mid-range smartwatches priced between USD 50 and USD 100 accounted for approximately 45% of global demand in 2025, positioning this category as the largest price segment. The segment benefits from its ability to offer advanced safety, communication, and health-monitoring functionalities while remaining affordable for middle-income households. Most consumers perceive this price range as delivering the optimal balance between performance, durability, battery life, and feature availability.

The strong growth of middle-class populations across Asia-Pacific, Latin America, and the Middle East has further expanded the addressable market for mid-range devices. Manufacturers increasingly focus product development within this category, introducing LTE connectivity, GPS tracking, educational applications, fitness monitoring, and parental control systems without significantly increasing retail prices. Additionally, aggressive competition among Chinese and international brands has enhanced feature availability while maintaining affordability. As component costs continue to decline and economies of scale improve, the mid-range segment is expected to remain the primary volume driver of global market growth.

Distribution Channel Insights

Online retail channels accounted for approximately 57% of global market sales in 2025, making e-commerce the dominant distribution channel for kids smartwatches. The segment's leadership is driven by increasing consumer preference for digital shopping platforms that offer extensive product selection, competitive pricing, customer reviews, product comparisons, and convenient home delivery services.

The rapid expansion of e-commerce ecosystems across North America, Europe, China, India, and Southeast Asia has significantly enhanced market accessibility. Major online marketplaces provide manufacturers with direct access to consumers while reducing dependence on traditional retail networks. Digital marketing campaigns, influencer endorsements, social media advertising, and promotional discount events further support online sales growth. While offline channels continue to play an important role in product demonstrations and first-time purchases, the convenience, transparency, and pricing advantages associated with online retail continue to strengthen the segment's market leadership. Omnichannel strategies are increasingly being adopted by leading brands to improve customer engagement and maximize conversion rates.

Age Group Insights

Children aged 9–12 years represented approximately 41% of global market demand in 2025, making them the largest age-based consumer segment. This age group represents a critical developmental stage during which children gain greater independence through school attendance, extracurricular activities, social interactions, and outdoor mobility. Parents increasingly seek technologies that provide communication and safety capabilities without exposing children to the risks associated with unrestricted smartphone usage.

The segment also benefits from strong product-market alignment, as smartwatch functionality directly addresses parental concerns related to child supervision, communication, and location awareness. Manufacturers continue to tailor devices specifically for pre-teen users through age-appropriate interfaces, educational applications, gaming features, and enhanced parental controls. Although younger children contribute significantly to demand, and older teenagers increasingly transition toward smartphones, the 9–12 age category remains the most attractive target demographic for smartwatch manufacturers globally.

Explore more data points, trends and opportunities Download Free Sample Report

Kids Smartwatch Market Segmentations

By Product Architecture

- Standalone Kids Smartwatch

- Companion/Integrated Kids Smartwatch

By Connectivity Technology

- Cellular (4G/5G/LTE/eSIM)

- Wi-Fi Enabled

- Bluetooth Enabled

- Hybrid Connectivity

By Application

- Child Safety & Tracking

- Communication

- Health & Fitness Monitoring

- Educational & Learning Functions

- Entertainment & Gaming Functions

By Distribution Channel

- Online Retail

- Consumer Electronics Stores

- Specialty Kids Stores

- Hypermarkets & Supermarkets

- Telecom Carrier Stores

By End User

- Individual Households

- Educational Institutions

- Childcare Centers

- Child Safety Programs & Government Initiatives

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 34.5% of global market revenue in 2025, making it the largest regional market for kids smartwatches. Regional growth is primarily supported by large child populations, rising disposable incomes, expanding middle-class households, and strong domestic electronics manufacturing ecosystems. China remains the dominant country market, accounting for nearly half of regional demand, driven by widespread adoption of child safety technologies, advanced telecommunications infrastructure, and the strong presence of domestic manufacturers. Chinese consumers have demonstrated high acceptance of GPS-enabled child monitoring devices, making the country one of the earliest adopters of kids smartwatches globally.

India represents the fastest-growing country market, supported by rapid smartphone ecosystem expansion, improving internet penetration, growing urbanization, and increasing parental awareness regarding child safety. Government initiatives supporting electronics manufacturing and digital connectivity are further contributing to market expansion. Meanwhile, Japan and South Korea continue to drive demand for premium smartwatches equipped with advanced health monitoring, AI-enabled features, and integrated communication capabilities. The combination of favorable demographics, manufacturing leadership, and digital transformation initiatives is expected to sustain Asia-Pacific's market leadership throughout the forecast period.

North America

North America accounted for approximately 32% of global market revenue in 2025, making it the second-largest regional market. The United States dominates regional demand due to high consumer purchasing power, advanced wireless infrastructure, widespread wearable technology adoption, and strong parental emphasis on child safety. The region has one of the highest penetrations of connected devices globally, creating favorable conditions for smartwatch adoption among children.

Growing concerns regarding school safety, increasing participation in extracurricular activities, and the prevalence of dual-income households continue to drive demand for location-tracking and communication-enabled devices. The United States also benefits from strong telecom operator participation, with dedicated smartwatch connectivity plans improving accessibility and functionality. Canada contributes steadily growing demand supported by high digital literacy, increasing adoption of connected wearables, and strong e-commerce penetration. Premium product adoption remains particularly strong throughout North America, resulting in higher average selling prices compared with many other regions.

Europe

Europe remains a significant market for kids smartwatches, led by Germany, the United Kingdom, France, Italy, and Spain. Regional growth is driven by rising consumer awareness regarding child safety, increasing wearable technology adoption, and strong regulatory emphasis on child data protection. European consumers place considerable importance on product quality, privacy compliance, and cybersecurity standards, encouraging manufacturers to develop secure and feature-rich devices.

Germany represents the largest market within the region due to strong purchasing power, advanced telecommunications infrastructure, and widespread technology adoption. The United Kingdom benefits from growing parental investment in connected child safety devices, while France and Italy continue to experience rising demand driven by urbanization and digital lifestyle trends. Additionally, the region's mature e-commerce ecosystem and increasing adoption of LTE-enabled wearables are supporting market growth. Regulatory frameworks such as GDPR have also encouraged higher standards of data security, improving consumer confidence in connected child monitoring devices.

Latin America

Latin America is emerging as a promising growth market, with Brazil and Mexico accounting for the majority of regional demand. Market growth is being supported by increasing internet penetration, expanding smartphone ecosystems, improving affordability of wearable devices, and growing awareness of child safety technologies. Rising urbanization and increasing participation of women in the workforce are further driving demand for child monitoring and communication solutions.

Brazil remains the largest regional market due to its sizable population base and expanding middle class, while Mexico benefits from increasing digitalization and cross-border technology adoption trends. The availability of affordable smartwatch models from Asian manufacturers has significantly improved accessibility across the region. As connectivity infrastructure continues to improve and disposable incomes increase, Latin America is expected to witness strong adoption growth over the forecast period.

Middle East & Africa

The Middle East and Africa region is gradually emerging as an attractive market for kids smartwatches. Growth is being driven by rising household incomes, expanding digital infrastructure, increasing smartphone penetration, and government-led digital transformation initiatives. Saudi Arabia and the United Arab Emirates account for the majority of regional demand due to their high consumer spending capacity and strong adoption of connected technologies.

Government programs supporting smart city development, digital education initiatives, and advanced telecommunications infrastructure are creating favorable conditions for smartwatch adoption. In Africa, South Africa remains the largest market due to its comparatively developed retail and telecommunications ecosystem. Increasing awareness of child safety technologies, combined with improving internet access and smartphone adoption rates, is expected to support long-term market expansion throughout the region. As affordability improves and connectivity infrastructure expands, the Middle East and Africa are likely to emerge as one of the most promising future growth regions for the kids smartwatch market.

Key Players in the Kids Smartwatch Market

- Huawei Technologies

- Xiaomi Corporation

- imoo

- 360 Smart Life

- Garmin Ltd.

- VTech Holdings

- TickTalk

- COSMO Technologies

- Doki Technologies

- Oaxis

- LG Electronics

- TCL Communication

- Omate

- Amazfit

- Kurio