Jatropha Biodiesel Market Size

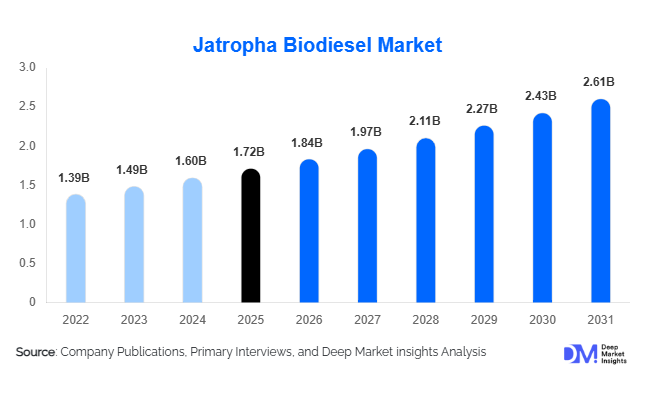

According to Deep Market Insights, the global jatropha biodiesel market size was valued at USD 1.72 billion in 2025 and is projected to grow from USD 1.84 billion in 2026 to reach USD 2.61 billion by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The market growth is primarily driven by increasing government mandates for renewable fuel blending, rising investments in non-food biofuel feedstocks, and growing demand for low-carbon transportation fuels across road transport, aviation, marine, and industrial sectors. Jatropha biodiesel has emerged as a strategically important second-generation biofuel due to its ability to be cultivated on marginal land without competing directly with food crops. The market is also benefiting from the expansion of sustainable aviation fuel (SAF) production pathways, carbon reduction targets, and energy security initiatives adopted by both developed and emerging economies.

Key Market Insights

- Jatropha biodiesel is increasingly being adopted as a sustainable non-food biofuel feedstock, helping countries achieve renewable energy and decarbonization targets.

- Sustainable aviation fuel production is creating new demand for jatropha oil feedstocks, particularly in Europe and North America.

- Asia-Pacific dominates the global market, accounting for approximately 43% of global demand in 2025, led by India, Indonesia, Thailand, and China.

- India remains the largest individual country market, supported by national biofuel policies and large-scale plantation development initiatives.

- Plantation-grown jatropha seeds account for more than half of global feedstock supply, ensuring traceability and long-term production stability.

- Hydroprocessing and biorefinery technologies are improving fuel yields and economics, enabling higher-value applications such as renewable diesel and SAF.

Jatropha Biodiesel Market Trends

Growing Integration with Sustainable Aviation Fuel Production

One of the most significant trends in the jatropha biodiesel market is the increasing use of jatropha-derived oils in sustainable aviation fuel production. Airlines and aviation fuel suppliers are under growing pressure to reduce lifecycle greenhouse gas emissions, creating demand for certified low-carbon feedstocks. Jatropha's non-food nature and favorable carbon profile make it a suitable feedstock for Hydroprocessed Esters and Fatty Acids (HEFA) pathways. Several renewable fuel producers are investing in integrated supply chains that connect jatropha cultivation with SAF production facilities. As governments introduce aviation fuel blending mandates and airlines commit to net-zero emissions targets, demand for jatropha-based SAF feedstock is expected to rise significantly over the next decade.

Expansion of Marginal Land Bioenergy Cultivation

Governments and private investors are increasingly focusing on utilizing underdeveloped and marginal land for energy crop cultivation. Jatropha is particularly attractive because it can be grown in semi-arid regions where conventional food crops are less viable. Countries across Africa, South Asia, and Latin America are expanding plantation development programs aimed at increasing domestic feedstock production while supporting rural economic development. Improved seed genetics, precision agriculture techniques, and irrigation systems are enhancing productivity and making large-scale cultivation more commercially attractive. This trend is strengthening feedstock security while reducing dependency on edible oil-based biodiesel feedstocks.

Jatropha Biodiesel Market Drivers

Expansion of Renewable Fuel Blending Mandates

Governments worldwide are strengthening renewable fuel regulations to reduce dependence on imported petroleum and lower transportation-related carbon emissions. National biodiesel blending programs in India, Indonesia, Brazil, Thailand, and several African nations are driving sustained demand for alternative feedstocks such as jatropha. As blending requirements increase, biodiesel producers are seeking non-food feedstock options that satisfy sustainability criteria without affecting food supply chains. Jatropha biodiesel is well positioned to benefit from these regulatory developments due to its favorable environmental profile and compatibility with existing diesel infrastructure.

Rising Demand for Energy Security and Domestic Fuel Production

Volatility in crude oil markets and geopolitical uncertainties have intensified efforts to diversify energy sources. Jatropha biodiesel provides countries with an opportunity to strengthen domestic fuel production while reducing exposure to international energy market disruptions. Emerging economies with suitable climatic conditions are increasingly supporting domestic cultivation programs to improve energy independence. This trend is particularly visible across Asia-Pacific and Africa, where governments view biofuels as strategic assets for long-term energy security and rural development.

Jatropha Biodiesel Market Restraints

Feedstock Availability and Yield Challenges

Despite its potential, the commercial expansion of jatropha biodiesel remains constrained by feedstock availability. Several early plantation projects underperformed due to lower-than-expected yields, inadequate agronomic practices, and inconsistent seed quality. These challenges continue to limit large-scale commercialization and create supply uncertainties for biodiesel producers. Improving cultivation techniques and developing high-yield seed varieties remain critical for addressing this constraint.

Higher Production Costs Compared to Conventional Diesel

Jatropha biodiesel production often involves higher cultivation, harvesting, and processing costs compared to conventional fossil diesel. Economic viability frequently depends on government incentives, carbon credit programs, and renewable fuel mandates. Fluctuations in labor costs, logistics expenses, and processing economics can impact profitability, particularly in regions where supportive policy frameworks are limited. Reducing production costs through technology adoption and economies of scale remains a major industry priority.

Jatropha Biodiesel Market Opportunities

Renewable Diesel and Carbon Credit Integration

The growing renewable diesel market presents substantial opportunities for jatropha biodiesel producers. Renewable diesel facilities increasingly require low-carbon feedstocks capable of meeting strict sustainability standards. Jatropha-derived oils can qualify for various carbon reduction programs and generate additional revenues through carbon credits. Producers that establish certified sustainable supply chains can improve profitability while attracting institutional investment into renewable fuel infrastructure.

Rural Development and Bioenergy Plantation Programs

Large-scale plantation initiatives across India, Africa, and Southeast Asia provide a significant growth opportunity for the industry. Governments are increasingly supporting bioenergy crop cultivation as part of broader rural development strategies aimed at generating employment, improving farmer incomes, and enhancing energy security. Public-private partnerships focused on plantation development, seed improvement, and processing infrastructure are expected to accelerate market growth while strengthening feedstock supply chains.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.72 Billion |

| Market Size in 2026 | USD 1.84 Billion |

| Market Size in 2031 | USD 2.61 Billion |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Pure Jatropha Biodiesel (B100) dominated the global jatropha biodiesel market in 2025, accounting for approximately 38% of total market revenue. The segment's leadership is primarily attributed to its role as the foundational product used for downstream biodiesel blending, industrial fuel substitution, and renewable energy applications. B100 serves as the primary feedstock for the production of lower biodiesel blends and is widely utilized in industrial boilers, captive power generation facilities, and transportation fleets operating under renewable fuel mandates. The segment has particularly benefited from increasing government support for biodiesel blending programs across Asia-Pacific and Latin America, where domestic biodiesel production is viewed as a strategic tool for enhancing energy security and reducing dependence on imported petroleum products.

The growing adoption of B5, B10, and B20 biodiesel blends continues to support demand for pure jatropha biodiesel, as refiners and fuel distributors require substantial volumes of B100 for blending operations. Additionally, advancements in fuel quality standards and engine compatibility have improved the commercial viability of biodiesel utilization across transportation and industrial sectors.

While B100 remains the largest segment, Hydrotreated Renewable Diesel (HDRD) and Jatropha-Based Sustainable Aviation Fuel (SAF) are emerging as the fastest-growing product categories. These fuels command premium pricing due to their lower carbon intensity, superior fuel characteristics, and compatibility with existing transportation infrastructure. Increasing investments in aviation decarbonization, coupled with expanding renewable diesel production capacity in North America and Europe, are expected to accelerate demand for jatropha-derived feedstocks in these high-value applications.

Feedstock Source Insights

Plantation-Grown Jatropha Seeds represented the largest feedstock source segment in 2025, contributing approximately 52% of total global feedstock supply. The segment's dominance stems from its ability to provide consistent oil yields, quality control, traceability, and long-term supply reliability. Large-scale commercial plantations in India, Indonesia, Mozambique, Tanzania, and other emerging biofuel-producing nations have become increasingly important for ensuring feedstock availability amid growing biodiesel demand.

The primary growth driver for plantation-grown feedstock is the increasing preference among biodiesel producers and renewable fuel refiners for certified and traceable raw materials that comply with sustainability standards. Dedicated plantations enable producers to optimize harvesting cycles, improve oil recovery rates, and implement advanced agronomic practices that enhance overall productivity. Investments in drought-resistant seed varieties, precision agriculture technologies, and improved irrigation systems are further improving plantation economics.

Contract farming programs are emerging as an important secondary sourcing model, particularly in Asia and Africa, where governments are encouraging farmer participation in bioenergy value chains. Meanwhile, community-based sourcing and residual oil recovery remain relevant in regions with fragmented cultivation landscapes, providing supplemental feedstock volumes while supporting rural economic development.

Application Insights

Road Transportation remained the leading application segment in 2025, accounting for approximately 35% of global jatropha biodiesel demand. The segment's leadership is primarily driven by government biodiesel blending mandates, rising demand for cleaner transportation fuels, and increasing efforts to reduce greenhouse gas emissions from commercial vehicle fleets. Heavy-duty trucks, public transportation buses, logistics fleets, and municipal vehicles continue to represent the largest consumers of biodiesel blends globally.

The transportation sector benefits from existing diesel infrastructure, allowing biodiesel blends to be adopted with minimal modifications to engines and fuel distribution networks. Rising diesel prices and increasing regulatory pressure to lower transportation emissions are further accelerating biodiesel adoption across both developed and developing economies.

Beyond road transportation, agricultural machinery remains a significant application area, particularly across emerging economies where biodiesel supports rural energy independence and farm mechanization initiatives. Marine fuel applications are also gaining momentum as shipping companies seek compliance with stricter emissions regulations. However, the most dynamic growth is expected from aviation fuel applications, where airlines and fuel suppliers are increasingly investing in sustainable aviation fuel pathways derived from non-food feedstocks such as jatropha.

Distribution Channel Insights

Direct Industrial Supply Contracts accounted for approximately 41% of global jatropha biodiesel distribution in 2025, making it the largest distribution channel. The segment's dominance is largely driven by long-term procurement agreements between biodiesel producers and large fuel consumers, including transportation companies, industrial manufacturers, utilities, and renewable fuel refiners.

The primary growth driver for this segment is supply security. Industrial buyers increasingly prefer direct contracts to ensure uninterrupted fuel availability, predictable pricing structures, and compliance with sustainability certification requirements. Long-term agreements also allow producers to secure stable revenue streams while enabling buyers to meet internal carbon reduction targets and regulatory obligations.

Government procurement programs continue to represent a substantial channel in countries implementing mandatory biodiesel blending programs. Meanwhile, oil marketing companies and fuel retailers are investing in blending infrastructure and renewable fuel distribution networks to expand biodiesel availability. The growing adoption of digital commodity trading platforms and blockchain-based sustainability certification systems is further enhancing supply chain transparency and operational efficiency across the distribution ecosystem.

End-Use Industry Insights

Transportation remained the largest end-use industry in the global jatropha biodiesel market, accounting for approximately 44% of total market demand in 2025. The segment's dominance is directly linked to expanding biodiesel blending mandates, fleet decarbonization initiatives, and rising corporate sustainability commitments. Commercial transportation operators are increasingly incorporating biodiesel into their fuel portfolios to reduce emissions while maintaining operational efficiency.

The segment is further supported by growing investments in public transportation electrification alternatives, low-carbon fuel infrastructure, and renewable energy integration. In developing economies, biodiesel adoption within transportation is also driven by efforts to reduce fuel import dependence and strengthen domestic energy security.

Agriculture remains a growing end-use industry, supported by increased use of biodiesel-powered tractors, irrigation pumps, and harvesting equipment. Industrial manufacturing and power generation sectors continue adopting biodiesel as a lower-carbon alternative to conventional fossil fuels, particularly in regions with stringent emissions regulations. The aviation industry is expected to emerge as the fastest-growing end-use sector through 2031, driven by sustainable aviation fuel mandates, airline net-zero commitments, and expanding investment in renewable aviation fuel infrastructure.

Explore more data points, trends and opportunities Download Free Sample Report

Jatropha Biodiesel Market Segmentations

By Product Type

- Pure Jatropha Biodiesel (B100)

- Jatropha Biodiesel Blends (B5, B10, B20, B30 and Above)

- Hydrotreated Jatropha Renewable Diesel (HDRD)

- Jatropha-Based Sustainable Aviation Fuel (SAF)

By Feedstock Source

- Plantation-Grown Jatropha Seeds

- Contract Farming Jatropha Feedstock

- Community/Aggregator-Sourced Jatropha Feedstock

- Waste and Residual Jatropha Oil Feedstock

By Production Technology

- Conventional Transesterification

- Enzymatic Biodiesel Production

- Hydroprocessing Technology

- Integrated Biorefinery Processing

By Blend Category

- Low Blend Fuel (Up to B10)

- Medium Blend Fuel (B11–B30)

- High Blend Fuel (Above B30)

- Neat Biodiesel (B100)

By Application

- Road Transportation Fuel

- Agriculture Machinery Fuel

- Industrial Energy & Boiler Fuel

- Marine Fuel Applications

- Power Generation

- Aviation Fuel Feedstock

By Distribution Channel

- Direct Industrial Supply Contracts

- Oil Marketing Companies (OMCs)

- Government Procurement Programs

- Fuel Retail Networks

Regional Insights

Asia-Pacific

Asia-Pacific dominated the global jatropha biodiesel market with approximately 43% market share in 2025 and is expected to remain the fastest-growing regional market throughout the forecast period. The region's leadership is driven by strong government support for biofuel development, extensive agricultural resources, rising energy demand, and increasing concerns regarding energy security. India remains the largest country market, accounting for nearly 18% of global demand, supported by national biofuel policies, large-scale plantation programs, and initiatives aimed at reducing crude oil import dependence.

Indonesia and Thailand continue expanding biodiesel blending programs and renewable fuel infrastructure, while China is increasing investments in low-carbon fuel technologies as part of broader carbon neutrality objectives. The Philippines and Malaysia are also exploring non-food feedstock cultivation to diversify biofuel production. Rapid industrialization, growing transportation fuel consumption, and supportive regulatory frameworks are expected to remain key drivers of regional growth.

Europe

Europe accounted for approximately 28% of global market revenue in 2025, making it the second-largest regional market. The region's growth is primarily driven by stringent carbon reduction targets, Renewable Energy Directive (RED) requirements, and aggressive sustainable aviation fuel adoption policies. Germany, France, the Netherlands, Spain, and Italy remain the leading markets due to strong commitments toward transportation decarbonization and renewable fuel utilization.

A major driver for regional demand is the rapid expansion of renewable diesel and sustainable aviation fuel production capacity. European refiners increasingly seek certified low-carbon feedstocks, creating substantial import opportunities for jatropha-derived oils. Rising carbon pricing mechanisms, net-zero targets, and growing investments in advanced biofuels continue to support long-term market expansion across the region.

North America

North America represented approximately 14% of global demand in 2025, led by the United States and Canada. The region's growth is largely supported by renewable fuel standards, Low Carbon Fuel Standard (LCFS) programs, federal clean energy incentives, and increasing investments in renewable diesel infrastructure.

The United States continues to drive demand through expanding renewable fuel production capacity and growing adoption of low-carbon transportation fuels. Strong investments in sustainable aviation fuel production, corporate sustainability initiatives, and favorable carbon credit programs are creating new opportunities for jatropha-derived feedstocks. Canada is also accelerating demand through clean fuel regulations and commitments to reduce transportation emissions.

Latin America

Latin America accounted for approximately 6% of global market demand in 2025, with Brazil serving as the region's dominant producer and consumer. The region benefits from extensive agricultural expertise, favorable climatic conditions, and a long-established biofuel industry. Brazil's biodiesel blending mandates and renewable energy policies continue to support market expansion.

Argentina and Colombia are increasingly investing in biodiesel diversification initiatives to strengthen domestic energy security and reduce fossil fuel dependency. Rising transportation fuel demand, supportive agricultural policies, and expanding export opportunities for renewable fuels are expected to contribute to sustained regional growth over the forecast period.

Middle East & Africa

The Middle East & Africa region accounted for approximately 9% of global market revenue in 2025 and is emerging as an important feedstock production hub. Africa possesses significant cultivation potential due to the availability of marginal land, favorable climatic conditions, and increasing government support for bioenergy development. Kenya, Mozambique, Tanzania, Ghana, and South Africa are among the most promising markets for commercial jatropha cultivation.

The key driver for growth across Africa is the ability of jatropha cultivation to support rural economic development while contributing to energy security objectives. Several governments are promoting biofuel crops as a means of generating employment and reducing reliance on imported fuels. In the Middle East, countries such as the UAE and Saudi Arabia are investing in renewable fuel technologies as part of broader economic diversification and sustainability strategies. Growing investments in sustainable aviation fuel, renewable diesel production, and carbon reduction initiatives are expected to accelerate regional demand in the coming years.

Key Players in the Jatropha Biodiesel Market

- Neste Oyj

- Archer Daniels Midland (ADM)

- Cargill Incorporated

- Renewable Energy Group

- Wilmar International

- Verbio SE

- Bunge Global

- Louis Dreyfus Company

- Eni Sustainable Mobility

- SG Biofuels

- JOil (S) Pte Ltd

- Emami Agrotech

- Petrobras Biocombustível

- FutureFuel Corp.

- Münzer Bioindustrie GmbH