Gaming Accessories Market Size

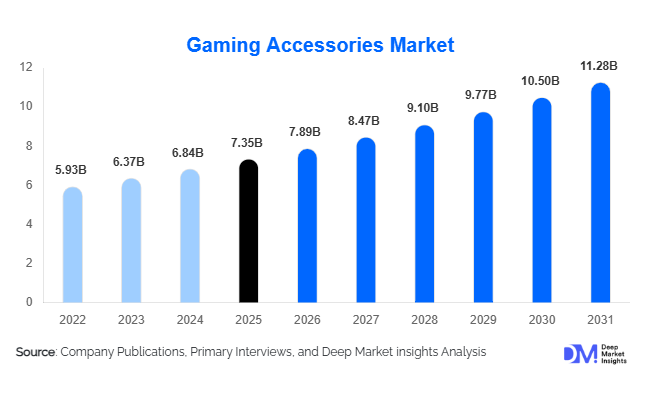

According to Deep Market Insights, the global gaming accessories market size was valued at USD 7.35 billion in 2025 and is projected to grow from USD 7.89 billion in 2026 to reach USD 11.28 billion by 2031, expanding at a CAGR of 7.4% during the forecast period (2026–2031). The gaming accessories market growth is primarily driven by the rapid expansion of esports, increasing gaming participation across PC, console, and mobile platforms, and growing consumer demand for immersive gaming experiences enabled by high-performance peripherals. Continuous innovation in wireless connectivity, haptic feedback, RGB customization, and AI-powered gaming technologies is further supporting market expansion. Rising disposable incomes in emerging economies and the increasing popularity of content creation and game streaming are creating new revenue streams for manufacturers, strengthening long-term demand for gaming accessories worldwide.

Key Market Insights

- Wireless gaming accessories account for more than 57% of total market revenue, driven by improvements in latency performance, battery life, and multi-device compatibility.

- Gaming controllers remain the largest product category, contributing approximately 24% of global market revenue due to sustained demand from console and mobile gaming ecosystems.

- North America dominates the global gaming accessories market, accounting for nearly 38% of total revenue, supported by strong consumer spending and mature esports infrastructure.

- Asia-Pacific is the fastest-growing regional market, fueled by expanding gamer populations in China, India, Indonesia, South Korea, and Southeast Asia.

- Gaming streamers and content creators are emerging as high-value consumers, increasing demand for microphones, webcams, capture cards, and professional streaming equipment.

- Artificial intelligence and smart personalization technologies are increasingly being integrated into gaming peripherals to improve performance optimization, audio quality, and user experience.

Gaming Accessories Market Trends

Wireless Ecosystems Becoming the Industry Standard

The gaming accessories market is experiencing a major shift toward wireless technologies. Consumers increasingly prefer wireless gaming mice, keyboards, headsets, and controllers due to improved battery efficiency and ultra-low latency connectivity. Manufacturers are investing heavily in proprietary wireless technologies capable of delivering near-wired performance levels, eliminating historical concerns around responsiveness and reliability. Multi-device compatibility is also becoming a key purchasing criterion, enabling users to seamlessly switch between PC, console, mobile, and cloud gaming platforms. As a result, wireless accessories continue to gain market share across both mainstream and premium gaming segments.

Gaming and Content Creation Ecosystems Converging

The rapid growth of streaming platforms and gaming content creation is creating demand beyond traditional gaming peripherals. Professional and aspiring content creators increasingly require webcams, microphones, lighting systems, stream controllers, and capture cards alongside gaming hardware. Manufacturers are responding by developing integrated ecosystems that support both gaming and content production workflows. This convergence is expanding the addressable market for gaming accessory vendors and creating opportunities for premium product bundles designed specifically for streamers and esports personalities. The trend is particularly strong among younger demographics who view gaming and content creation as complementary activities.

Gaming Accessories Market Drivers

Expansion of the Global Gaming Population

The growing number of active gamers worldwide remains one of the strongest growth drivers for the gaming accessories market. Increasing internet penetration, smartphone accessibility, cloud gaming adoption, and affordable gaming hardware have significantly expanded the gamer base across both developed and emerging economies. Gaming has evolved into mainstream entertainment, encouraging consumers to invest in performance-enhancing accessories that improve gameplay quality and competitiveness. This expanding user base continues to generate demand across entry-level, mid-range, and premium accessory categories.

Growth of Esports and Competitive Gaming

The global esports ecosystem has become a major catalyst for gaming accessories demand. Professional gaming tournaments, collegiate esports programs, and online competitions have increased awareness of specialized peripherals such as mechanical keyboards, high-DPI gaming mice, and low-latency headsets. Professional players and influencers often shape consumer purchasing decisions, encouraging enthusiasts to invest in tournament-grade equipment. The commercialization of esports through sponsorships, media rights, and franchise leagues is expected to further stimulate premium accessory sales over the forecast period.

Gaming Accessories Market Restraints

Market Saturation in Developed Economies

Several developed markets, particularly in North America and Western Europe, have already achieved high penetration rates for gaming accessories. As a result, manufacturers increasingly rely on replacement demand rather than new customer acquisition. This creates pricing pressure and intensifies competition among established brands seeking to differentiate through incremental technological improvements. Mature markets also exhibit longer replacement cycles, particularly for premium peripherals with extended product lifespans.

Price Sensitivity in Emerging Markets

Despite strong growth potential across Asia-Pacific, Latin America, and Africa, affordability remains a significant challenge. Premium gaming accessories often carry pricing structures that exceed the purchasing power of average consumers in emerging economies. Import duties, currency fluctuations, and limited local manufacturing capabilities can further elevate retail prices. Manufacturers must balance performance innovation with affordability to effectively capture market opportunities in high-growth regions.

Gaming Accessories Market Opportunities

AI-Enabled Smart Gaming Accessories

Artificial intelligence is creating substantial opportunities for product differentiation within the gaming accessories market. AI-powered technologies are increasingly being used to optimize audio performance, personalize sensitivity settings, enhance communication quality, and automate performance adjustments. Manufacturers capable of integrating machine learning algorithms and software ecosystems into their peripherals can command premium pricing while building stronger customer loyalty. AI-driven gaming experiences are expected to become a key competitive differentiator over the next decade.

Expansion of Esports Infrastructure in Emerging Markets

Governments, educational institutions, and private investors are increasingly supporting esports infrastructure development across emerging markets. Countries such as India, Saudi Arabia, Brazil, Indonesia, and the United Arab Emirates are investing in gaming arenas, esports leagues, and digital entertainment ecosystems. These developments are creating demand for professional-grade gaming accessories while expanding opportunities for international and regional manufacturers. Growing participation in organized competitive gaming is expected to accelerate premium peripheral adoption among both amateur and professional players.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7.35 Billion |

| Market Size in 2026 | USD 7.89 Billion |

| Market Size in 2031 | USD 11.28 Billion |

| CAGR | 7.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Gaming controllers accounted for approximately 24% of the global gaming accessories market in 2025, making them the largest product segment. The segment's leadership is primarily driven by the continued expansion of console gaming ecosystems led by PlayStation, Xbox, and Nintendo platforms, alongside growing adoption of mobile gaming controllers for competitive smartphone gaming. Frequent product refresh cycles, increasing demand for customizable controllers, and the integration of advanced features such as adaptive triggers, haptic feedback, motion sensing, and programmable buttons continue to stimulate replacement purchases. The growing popularity of esports and competitive gaming has further accelerated demand for professional-grade controllers that provide enhanced precision and responsiveness.

Gaming headsets represent the second-largest category, supported by the growing importance of multiplayer gaming, voice communication, and team-based esports competitions. The increasing adoption of immersive 3D audio technologies and noise-canceling features is driving premium headset sales. Mechanical gaming keyboards and high-performance gaming mice continue to benefit from the rapid expansion of PC gaming and esports participation, particularly among FPS, MOBA, and MMORPG players who prioritize responsiveness and customization.

Gaming chairs, streaming accessories, and VR peripherals are among the fastest-growing product categories, driven by consumers increasingly investing in complete gaming setups. The growth of content creation, professional streaming, and virtual reality gaming is encouraging purchases beyond traditional peripherals, creating opportunities for manufacturers to develop integrated gaming ecosystems rather than standalone products.

Connectivity Insights

Wireless gaming accessories dominated the market with approximately 57% revenue share in 2025, making them the leading connectivity segment globally. The primary driver behind wireless leadership is the significant improvement in low-latency wireless technologies, enabling performance levels that closely match wired alternatives. Advances in battery efficiency, fast charging capabilities, wireless charging docks, and multi-device pairing have substantially improved user convenience without compromising gaming performance. The rise of hybrid gaming environments, where consumers frequently switch between PCs, consoles, mobile devices, and cloud gaming platforms, has further accelerated wireless adoption. Premium gamers increasingly value cable-free gaming setups that improve aesthetics and mobility while maintaining competitive performance.

Although wired accessories continue to maintain strong demand among professional esports players due to their reputation for maximum reliability and uninterrupted connectivity, their market share is gradually declining as wireless technologies mature. Hybrid accessories capable of operating in both wired and wireless modes are also gaining popularity among consumers seeking flexibility across multiple gaming environments.

Platform Insights

PC gaming accounted for approximately 42% of global gaming accessories demand in 2025, making it the leading platform segment. PC gamers typically purchase a wider range of peripherals compared to console users, including gaming mice, mechanical keyboards, high-refresh-rate monitors, headsets, streaming equipment, RGB accessories, and ergonomic gaming furniture. This broader accessory ecosystem contributes significantly to higher spending per user. The continued growth of esports tournaments, online multiplayer gaming, and content creation has strengthened PC gaming's dominance. The platform's superior customization capabilities and compatibility with professional-grade peripherals further support accessory adoption. Additionally, gaming influencers and streamers predominantly use PC-based setups, influencing consumer purchasing decisions worldwide.

Console gaming remains a major contributor to accessory demand, supported by growing sales of next-generation consoles and increasing purchases of controllers, charging stations, racing wheels, and gaming headsets. Meanwhile, mobile gaming accessories are experiencing the fastest volume growth due to rising smartphone gaming participation, particularly across Asia-Pacific and Latin America. Cloud gaming is emerging as a future growth catalyst by encouraging demand for platform-agnostic accessories that function seamlessly across multiple devices.

End User Insights

Enthusiast gamers accounted for approximately 37% of global gaming accessories revenue in 2025, making them the largest end-user segment. This group's leadership is driven by higher spending behavior, frequent hardware upgrades, and strong interest in premium gaming experiences. Enthusiast gamers are more likely to invest in multiple peripherals simultaneously, including keyboards, mice, controllers, headsets, gaming chairs, and streaming equipment, resulting in significantly higher average revenue per user compared to casual gamers. Casual gamers continue to represent the largest consumer base by volume; however, their purchasing decisions remain highly price-sensitive and focused on essential accessories. In contrast, enthusiast gamers prioritize performance, customization, aesthetics, and compatibility with emerging gaming technologies.

Professional esports athletes and gaming content creators represent the fastest-growing end-user segments. The increasing commercialization of esports and the rapid expansion of streaming platforms are driving demand for premium accessories featuring low-latency connectivity, advanced customization software, professional audio quality, and content production capabilities. Additionally, gaming cafés and esports arenas continue to generate commercial demand through large-scale procurement and periodic equipment upgrades.

Distribution Channel Insights

Online retail channels accounted for approximately 63% of global gaming accessories sales in 2025, making them the dominant distribution channel. The segment's leadership is primarily driven by wider product availability, competitive pricing, access to international brands, and increasing consumer preference for digital purchasing experiences. Online platforms also provide detailed product comparisons, customer reviews, gaming influencer recommendations, and exclusive promotional offers that significantly influence purchasing decisions. The rapid growth of direct-to-consumer (DTC) business models has enabled manufacturers to strengthen customer relationships while improving profit margins. Leading gaming brands increasingly leverage proprietary online stores to launch exclusive products, software subscriptions, and loyalty programs.

Offline retail channels continue to maintain relevance, particularly for premium products where consumers prefer physical demonstrations before purchase. Electronics retailers and gaming specialty stores remain important touchpoints for high-value purchases, while omnichannel retail strategies are becoming increasingly common as manufacturers seek to integrate digital convenience with in-store experiences.

Explore more data points, trends and opportunities Download Free Sample Report

Gaming Accessories Market Segmentations

By Product Type

- Gaming Controllers

- Gaming Headsets & Audio Accessories

- Gaming Keyboards

- Gaming Mice

- Gaming Mousepads & Surfaces

- Gaming Chairs

- Gaming Monitors & Display Accessories

- Virtual Reality (VR) & AR Gaming Accessories

- Streaming & Content Creation Accessories

- Gaming Storage & Connectivity Accessories

By Connectivity

- Wired Accessories

- Wireless Accessories

- Hybrid Connectivity Accessories

By Gaming Platform

- PC Gaming

- Console Gaming

- Mobile Gaming

- Cloud Gaming Platforms

By End User

- Casual Gamers

- Enthusiast Gamers

- Professional Esports Players

- Gaming Streamers & Content Creators

- Gaming Cafés & Esports Arenas

By Distribution Channel

- Online Retail

- Electronics Stores

- Gaming Specialty Stores

- Hypermarkets & Supermarkets

- Direct-to-Consumer (Brand Websites)

Regional Insights

North America

North America accounted for approximately 38% of global gaming accessories revenue in 2025, making it the largest regional market. The United States alone contributes nearly 31% of global demand, supported by one of the world's highest gaming expenditures per capita, mature gaming infrastructure, and a highly developed esports ecosystem. Strong consumer purchasing power enables widespread adoption of premium gaming peripherals, including high-end wireless headsets, mechanical keyboards, and professional-grade gaming controllers.

Regional growth is being driven by expanding creator economies, increasing livestreaming activity, and strong adoption of subscription-based gaming services. The continued popularity of competitive gaming, coupled with widespread broadband penetration and advanced digital infrastructure, supports demand for premium gaming setups. Canada is also experiencing steady growth due to rising participation in PC gaming, esports, and content creation.

Europe

Europe accounted for approximately 22% of global gaming accessories revenue in 2025. Germany remains the largest market within the region due to its strong PC gaming culture, established esports ecosystem, and high consumer spending on gaming hardware. The United Kingdom, France, Italy, and Spain collectively contribute substantial demand for both gaming and content creation accessories.

Regional growth is supported by increasing esports participation, expanding creator economies, and growing consumer preference for premium gaming peripherals. European consumers are increasingly adopting wireless technologies and environmentally sustainable products, encouraging manufacturers to introduce eco-friendly materials and energy-efficient devices. High broadband penetration and strong digital infrastructure continue to facilitate online gaming and esports participation throughout the region.

Asia-Pacific

Asia-Pacific accounted for approximately 30% of global gaming accessories revenue in 2025 and represents the fastest-growing regional market. China remains the largest country market, contributing approximately 16% of global demand due to its massive gamer population, strong domestic manufacturing capabilities, and mature esports industry. The country's extensive gaming ecosystem supports demand across virtually all accessory categories.

India is emerging as one of the fastest-growing gaming accessories markets globally, driven by rapid smartphone gaming adoption, increasing esports participation, affordable internet access, and rising disposable incomes. Japan and South Korea continue to drive premium accessory demand through strong console gaming cultures, advanced gaming technologies, and highly competitive esports ecosystems.

Southeast Asian countries including Indonesia, Vietnam, Thailand, and the Philippines are becoming significant growth engines due to expanding digital populations, growing gaming communities, and increasing penetration of affordable gaming hardware. The region's large youth demographic and strong mobile gaming culture are expected to sustain above-average growth throughout the forecast period.

Latin America

Latin America accounted for approximately 6% of global gaming accessories revenue in 2025. Brazil represents the largest regional market, followed by Mexico and Argentina. The region's growth is being driven by increasing internet penetration, expanding esports communities, and a rapidly growing young gamer population.

The rising popularity of mobile gaming and affordable PC gaming setups has increased demand for entry-level and mid-range gaming accessories. Improvements in digital payment systems, e-commerce infrastructure, and cross-border retail accessibility are further supporting market expansion. While economic volatility and affordability constraints remain challenges, growing gaming engagement continues to drive long-term demand across major urban centers.

Middle East & Africa

The Middle East & Africa accounted for approximately 4% of global gaming accessories revenue in 2025 but represents one of the most promising emerging markets. Saudi Arabia and the United Arab Emirates are leading regional growth through substantial investments in gaming infrastructure, esports tournaments, gaming festivals, and digital entertainment initiatives. Government-backed programs aimed at developing gaming ecosystems are accelerating market expansion.

Saudi Arabia's strategic investments in gaming and esports under broader economic diversification initiatives are creating significant opportunities for gaming accessory manufacturers. The UAE benefits from strong consumer purchasing power, a growing gaming community, and increasing adoption of premium gaming technologies. Within Africa, South Africa remains the largest market due to rising PC gaming participation, improving internet connectivity, and growing consumer awareness of premium gaming peripherals. The continued expansion of digital infrastructure across the region is expected to support future market growth.

Key Players in the Gaming Accessories Market

- Logitech

- Razer

- Corsair

- SteelSeries

- Turtle Beach

- ASUS ROG

- HyperX

- Microsoft Xbox

- Sony PlayStation

- Thrustmaster

- Lenovo Legion

- Acer Predator

- Cooler Master

- Alienware (Dell)

- MSI