Cremation Urns Market Size

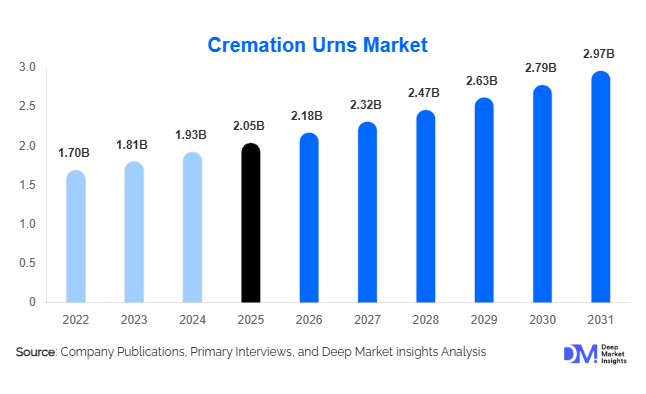

According to Deep Market Insights, the global cremation urns market size was valued at USD 2.05 billion in 2025 and is projected to grow from USD 2.18 billion in 2026 to reach USD 2.97 billion by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The cremation urns market growth is primarily driven by rising global cremation rates, increasing consumer preference for personalized memorialization products, and growing adoption of eco-friendly funeral practices. The expansion of digital memorial services, premium handcrafted urns, and online funeral product distribution channels is further strengthening market growth worldwide.

Key Market Insights

- Personalized cremation urns are witnessing strong global demand, driven by consumer preference for customized engravings, artistic memorials, and emotionally connected remembrance products.

- Biodegradable and eco-friendly urns are rapidly gaining popularity, particularly in North America and Europe, as sustainability becomes a key factor in funeral planning decisions.

- North America dominates the cremation urns market, supported by high cremation adoption rates, strong memorial spending, and advanced funeral service infrastructure.

- Asia-Pacific remains the fastest-growing regional market, fueled by urbanization, rising disposable income, and the modernization of cremation infrastructure in China and India.

- Online retail and direct-to-consumer funeral platforms are reshaping distribution channels, enabling greater product customization and global market accessibility.

- Technological integration, including laser engraving, QR-code memorial systems, AI-assisted customization, and 3D-printed urns, is transforming consumer engagement within the industry.

Cremation Urns Market Trends

Growing Adoption of Eco-Friendly Memorial Products

The cremation urns industry is increasingly shifting toward environmentally sustainable memorialization solutions. Consumers are adopting biodegradable urns made from recycled paper, bamboo, clay, salt compounds, and organic fibers that naturally decompose in soil or water. Water burial ceremonies and tree-planting memorial urns are gaining traction among environmentally conscious consumers seeking low-impact funeral alternatives. Funeral homes and memorial product companies are expanding eco-friendly product portfolios to align with changing customer preferences and evolving environmental regulations. This sustainability trend is particularly strong among younger consumers and urban populations across North America, Europe, and Japan.

Rise of Personalized and Digitally Integrated Urns

Personalization has become one of the strongest trends within the cremation urns market. Consumers increasingly seek memorial products that reflect the identity, beliefs, hobbies, and emotional legacy of the deceased. Customized engravings, photo-etched urns, handcrafted artistic designs, and culturally themed memorials are witnessing strong demand globally. Companies are also introducing QR-code-enabled urns, NFC memorial systems, and digital remembrance platforms that allow families to access online tributes, videos, and memorial archives. Artificial intelligence-assisted design customization and 3D printing technologies are further transforming premium memorialization experiences.

Cremation Urns Market Drivers

Rising Global Cremation Rates

The increasing adoption of cremation worldwide remains the primary growth driver for the cremation urns market. Rising burial costs, urban land scarcity, changing religious attitudes, and simplified funeral arrangements are encouraging families to choose cremation over traditional burial methods. Countries such as Japan, the United States, Canada, Germany, and South Korea now report cremation rates exceeding 60–90% of total deaths annually. This structural transition is creating sustained long-term demand for cremation urns, memorial accessories, and related funeral products.

Growing Demand for Personalized Memorialization

Consumers increasingly prefer memorial products that provide emotional connection and unique personalization. Premium handcrafted urns, engraved memorials, artistic glass urns, and bespoke memorial jewelry are gaining popularity across developed economies. Families are willing to spend more on customized remembrance products that reflect personal identity and cultural traditions. The expansion of online customization tools, digital memorial platforms, and direct-to-consumer funeral product sales is further accelerating demand for premium and personalized urn solutions.

Cremation Urns Market Restraints

Intense Pricing Competition

The cremation urns market faces significant pricing pressure due to the presence of numerous regional manufacturers and expanding online marketplaces. Standardized mass-produced urns are becoming increasingly commoditized, limiting profit margins for smaller suppliers. Online retail platforms have intensified price transparency, making it difficult for manufacturers to maintain premium pricing within lower-end product categories. Competition from low-cost imports, particularly from Asian manufacturing hubs, continues to challenge established regional suppliers.

Cultural and Religious Limitations

Despite rising cremation acceptance globally, several countries and religious communities continue to favor traditional burial practices. Certain cultural and religious beliefs across Africa, the Middle East, and parts of Latin America continue to limit cremation adoption, thereby restricting urn demand. Additionally, regulatory differences related to funeral practices, transportation of cremated remains, and environmental compliance increase operational complexity for manufacturers operating across multiple countries.

Cremation Urns Market Opportunities

Expansion of Pet Memorialization Services

The rapidly growing pet aftercare industry presents substantial opportunities for cremation urn manufacturers. Rising pet ownership and increasing emotional spending on companion animals are driving demand for premium pet memorial products. Customized pet urns, engraved keepsakes, biodegradable pet memorials, and decorative home-display urns are witnessing strong growth across the United States, Japan, China, and Western Europe. Veterinary clinics and pet cremation providers are becoming important distribution channels for memorial product manufacturers.

Digital Memorialization and Smart Memorial Products

Technological innovation is creating new opportunities within the cremation urns market. Smart memorial urns equipped with QR codes, NFC technology, and digital remembrance platforms are gaining popularity among younger consumers. These systems allow families to access memorial videos, digital photo galleries, biographies, and tribute pages through connected devices. Companies investing in AI-assisted personalization, online memorial ecosystems, and digitally integrated funeral products are expected to gain competitive advantages within premium market categories.

Product Type Insights

Traditional adult urns dominate the cremation urns market, accounting for the largest share of global demand due to their broad availability, affordability, and compatibility with standard funeral services. Metal urns, particularly brass and stainless steel variants, remain highly preferred because of their durability, premium appearance, and engraving compatibility. Biodegradable urns are emerging as one of the fastest-growing product categories, supported by rising environmental awareness and growing interest in sustainable funeral practices. Keepsake urns and memorial jewelry are also gaining traction as families increasingly choose shared remembrance solutions. Pet cremation urns continue to witness strong expansion, fueled by rising global pet ownership and increasing emotional spending on companion animal aftercare.

Material Type Insights

Metal-based urns represent the leading material category within the global market, accounting for a significant share of total industry revenues. Brass, stainless steel, and aluminum urns remain popular due to their durability, corrosion resistance, and premium decorative appeal. Wooden urns are widely adopted for traditional and handcrafted memorialization purposes, especially in North America and Europe. Ceramic and glass urns are increasingly preferred within premium artistic memorial categories because of their aesthetic value and handcrafted designs. Biodegradable materials such as clay, bamboo, salt compounds, and recycled paper are witnessing strong growth as eco-friendly funeral practices gain momentum globally.

Distribution Channel Insights

Funeral homes and crematoriums remain the dominant distribution channel within the cremation urns market due to their direct involvement in funeral planning and memorial product recommendations. These providers often bundle urn products within comprehensive funeral service packages, influencing purchasing decisions. However, online retail platforms are rapidly transforming the industry by enabling direct-to-consumer purchasing, real-time product customization, and global accessibility. Specialty memorial stores continue to serve premium and luxury segments focused on artistic and handcrafted memorial products. Direct-to-consumer brand websites are also gaining traction as manufacturers invest in digital marketing, customization tools, and e-commerce infrastructure.

Application Insights

Home memorialization represents the largest application segment within the cremation urns market, supported by increasing consumer preference for keeping ashes within residential memorial spaces instead of traditional cemetery interment. Columbarium storage and burial applications continue to generate steady demand, particularly in regions with organized cemetery infrastructure. Water burial ceremonies are becoming increasingly popular among environmentally conscious consumers seeking sustainable remembrance options. Religious ceremonies and cultural memorial traditions continue to influence urn selection and design preferences across different regions. Pet memorialization applications remain one of the fastest-growing segments globally, driven by premiumization within the pet aftercare industry.

End-Use Insights

Funeral homes remain the largest end-use segment in the cremation urns market due to their integrated memorial planning services and established customer relationships. Crematorium operators are increasingly expanding in-house memorial product offerings to improve profitability and customer retention. Households and families represent the fastest-growing end-use category as consumers increasingly purchase urns directly through online platforms and prefer home-based memorialization. Pet memorial service providers are also emerging as a significant customer group due to increasing pet cremation adoption and premium memorial spending. Religious institutions and memorial parks continue to support stable demand for traditional and culturally customized urn products.

| By Product Type | By Personalization Level | By Distribution Channel | By Application | By End User |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America remains the largest regional market for cremation urns, accounting for approximately 37% of global revenue in 2025. The United States dominates regional demand due to cremation rates exceeding 60%, strong funeral industry infrastructure, and high spending on personalized memorial products. Consumers increasingly prefer customized, artistic, and eco-friendly urns across the U.S. and Canada. Online funeral product sales are particularly strong in North America, where digital purchasing behavior continues to reshape the memorialization industry.

Europe

Europe represents one of the most mature cremation urns markets globally, led by Germany, the United Kingdom, France, Italy, and the Netherlands. Rising environmental awareness and limited burial space are accelerating the adoption of cremation and biodegradable memorial products across the region. European consumers increasingly prioritize sustainable funeral practices, artistic memorialization, and handcrafted urn designs. Scandinavian countries are particularly active in adopting eco-friendly urn solutions and green funeral alternatives.

Asia-Pacific

Asia-Pacific is projected to witness the fastest market growth during the forecast period, supported by rapid urbanization, increasing cremation infrastructure development, and rising middle-class spending. Japan remains one of the world’s largest cremation-based funeral markets with cremation rates above 90%. China is witnessing substantial market expansion due to government encouragement of cremation practices and urban land constraints. India is emerging as a high-growth market due to modernization of crematorium infrastructure and the increasing adoption of organized funeral services in metropolitan areas.

Latin America

Latin America is gradually expanding within the cremation urns market, particularly across Brazil and Mexico. Rising urbanization, growing middle-class income levels, and increasing acceptance of cremation are supporting market growth. However, traditional burial preferences continue to limit faster expansion across several regional markets. Premium memorial products and personalized urns are gradually gaining traction among affluent urban consumers.

Middle East & Africa

The Middle East & Africa region currently represents a relatively smaller share of the global cremation urns market due to cultural and religious preferences for traditional burial practices. However, South Africa remains the leading regional market because of its developed funeral industry infrastructure and growing urban cremation adoption. The UAE is witnessing gradual demand growth due to rising expatriate populations and the modernization of funeral services. Long-term market growth in the region is expected to remain moderate compared to other global regions.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Cremation Urns Market

- Matthews International Corporation

- Batesville Services

- Perfect Memorials

- Foreverence

- Urns Northwest

- Memorials.com

- Everlife Memorials

- Eco Urns

- Ceabis

- Northwoods Casket Company