Cheese Grater Market Size

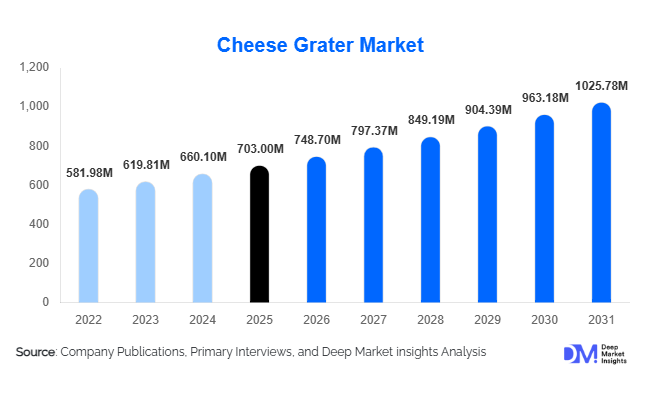

According to Deep Market Insights, the global cheese grater market size was valued at USD 703 million in 2025 and is projected to grow from USD 748.70 million in 2026 to reach USD 1,025.78 million by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The cheese grater market growth is primarily driven by rising global cheese consumption, the expansion of the foodservice and hospitality industries, and increasing consumer interest in home cooking and culinary experimentation.

Cheese graters are essential kitchen tools used across households, restaurants, and food processing environments for shredding, slicing, and zesting cheese and other food ingredients. As global culinary preferences evolve toward fresh ingredient preparation and artisanal cooking, the demand for specialized kitchen tools has increased. Consumers increasingly prefer freshly grated cheese over pre-packaged shredded varieties due to superior taste, texture, and nutritional value. This trend has contributed to steady demand for high-quality graters across developed and emerging markets.

Technological innovation in kitchenware design has also strengthened market growth. Manufacturers are introducing ergonomic handles, anti-slip bases, interchangeable blades, and dishwasher-safe materials to enhance user safety and convenience. Premium stainless steel graters and multifunctional grating systems are gaining traction among consumers seeking durable and versatile kitchen tools.

In addition, the rapid expansion of online retail platforms has enabled manufacturers to reach global consumers directly. E-commerce channels are accelerating the adoption of niche products such as rotary graters, electric graters, and professional-grade tools designed for commercial kitchens. As the foodservice sector continues to expand worldwide and culinary lifestyles evolve, the global cheese grater market is expected to maintain stable growth over the coming decade.

Key Market Insights

- Household kitchens account for the largest share of demand, driven by increasing interest in home cooking and fresh ingredient preparation.

- Stainless steel graters dominate the market due to durability, corrosion resistance, and compliance with food safety standards.

- Europe represents the largest regional market, supported by strong cheese consumption and culinary traditions that favor fresh grating.

- Asia-Pacific is the fastest-growing region, driven by rising middle-class incomes and expanding Western food consumption.

- Manual graters continue to dominate sales, although electric graters are gaining traction in commercial kitchens and foodservice environments.

- E-commerce platforms are reshaping distribution channels, enabling niche brands to compete globally and increasing product accessibility.

What are the latest trends in the cheese grater market?

Rising Demand for Multifunctional Kitchen Tools

Modern consumers increasingly prefer kitchen tools that perform multiple functions while minimizing storage space. This trend has accelerated the popularity of multifunctional cheese graters equipped with interchangeable blades capable of slicing, shredding, zesting, and grating various ingredients. Manufacturers are responding by introducing modular grater systems that allow users to switch blades depending on the food preparation task. These versatile tools appeal particularly to urban households where compact kitchen storage is essential. Additionally, multifunctional graters are popular among cooking enthusiasts who experiment with global cuisines requiring diverse food preparation techniques.

Growth of Premium Stainless-Steel Graters

Premiumization is becoming a prominent trend in the kitchenware sector. Consumers increasingly prefer durable stainless-steel graters with ergonomic designs and enhanced safety features. High-quality materials improve longevity and hygiene, making them particularly attractive for both households and professional kitchens. Premium brands are focusing on patented blade technologies that offer sharper cutting edges and smoother grating performance. In developed markets such as North America and Europe, premium graters with sleek designs and anti-slip bases are becoming standard household tools. This shift toward quality and durability has helped manufacturers command higher margins in the premium product segment.

What are the key drivers in the cheese grater market?

Growing Global Cheese Consumption

One of the primary drivers of the cheese grater market is the steady rise in global cheese consumption. Cheese is widely used across cuisines including Italian, American, European, and fusion dishes. Freshly grated cheese enhances flavor and texture in foods such as pasta, pizza, salads, and baked dishes. Restaurants and households alike prefer fresh grating to maintain taste quality, driving consistent demand for cheese graters. As cheese consumption increases in emerging markets due to westernization of diets and expansion of fast-food chains, the demand for cheese graters continues to grow.

Expansion of the Foodservice Industry

The global foodservice industry is expanding rapidly, supported by the growth of quick-service restaurants, cafes, and cloud kitchens. Professional kitchens frequently require cheese graters for food preparation processes such as topping pizzas, pasta dishes, and salads. The need for consistent texture and presentation encourages restaurants to use commercial-grade graters instead of pre-processed ingredients. As hospitality industries grow across Asia-Pacific and the Middle East, institutional demand for durable and high-capacity graters is expected to increase significantly.

What are the restraints for the global market?

Availability of Pre-Shredded Cheese Products

The widespread availability of pre-shredded cheese products presents a notable challenge to the cheese grater market. Packaged shredded cheese offers convenience and time savings for consumers who prefer quick meal preparation. In busy urban environments where convenience is prioritized, some households may rely on pre-processed cheese rather than grating it manually. This trend can limit growth potential in certain consumer segments.

Price Sensitivity in Emerging Markets

In developing economies, price sensitivity remains a significant barrier for branded kitchenware manufacturers. Many consumers purchase low-cost unbranded graters that compete aggressively on price but often lack durability and safety features. This intense competition compresses profit margins for established brands attempting to expand in price-sensitive markets.

What are the key opportunities in the cheese grater industry?

Growth of Commercial Foodservice Equipment

The expansion of restaurants, pizza chains, and catering services presents significant opportunities for manufacturers of professional-grade cheese graters. Commercial kitchens require durable and efficient tools capable of handling large food preparation volumes. Manufacturers are introducing heavy-duty graters designed specifically for horeca environments, including rotary and electric variants that improve operational efficiency. As the global hospitality industry continues to expand, institutional demand is expected to generate stable long-term revenue streams.

E-Commerce Expansion and Direct-to-Consumer Sales

The rapid growth of e-commerce platforms has created new opportunities for kitchenware brands to reach global consumers. Online marketplaces enable manufacturers to showcase innovative grater designs and target niche culinary communities. Social media cooking influencers and recipe platforms further support product discovery by demonstrating the functionality of specialized kitchen tools. Direct-to-consumer sales channels also allow brands to maintain stronger control over pricing and customer relationships while reducing dependency on traditional retail distributors.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 703 Million |

| Market Size in 2026 | USD 748.70 Million |

| Market Size in 2031 | USD 1025.78 Million |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global cheese grater market is segmented into box graters, rotary graters, flat handheld graters, microplane-style graters, and electric graters. Among these, box graters dominate the market, accounting for approximately 32% of global revenue. Their leadership is primarily driven by their multifunctionality and versatility. Box graters typically feature multiple grating surfaces, allowing users to shred, slice, zest, and grate a variety of ingredients with a single tool. This versatility makes them highly practical for everyday cooking tasks in household kitchens while also supporting moderate commercial usage.The demand for box graters is further supported by their durability, affordability, and compatibility with a wide range of food preparation applications, including cheese, vegetables, chocolate, and citrus. As consumers increasingly prioritize multi-purpose kitchen tools that save storage space and reduce the need for multiple utensils, box graters continue to maintain a strong presence in both developed and emerging markets.

Rotary graters are gaining traction, particularly in commercial kitchens and foodservice establishments, due to their ability to process ingredients quickly and efficiently. These graters often feature crank-operated mechanisms that allow continuous grating with minimal physical effort, making them ideal for restaurants, pizza chains, and catering operations that require large volumes of grated cheese.Flat handheld graters and microplane-style graters are widely used for fine grating tasks such as zesting citrus fruits, shredding hard cheeses like parmesan, or grating spices such as nutmeg and garlic. Their compact design, precision blades, and ease of handling make them popular among professional chefs and culinary enthusiasts who require precision in food preparation.Electric graters represent a smaller but steadily growing segment. Increasing demand for kitchen automation and convenience in food preparation is encouraging the adoption of electric models, particularly in professional kitchens and high-income households. These devices reduce manual effort, improve efficiency, and provide consistent results, making them suitable for both large-scale food preparation and premium residential kitchens.

Material Insights

The cheese grater market is segmented based on material into stainless steel, plastic composites, ceramic, aluminum, and hybrid materials. Stainless steel dominates the market, accounting for more than 60% of global demand, driven by its superior durability, corrosion resistance, and food safety compliance. Stainless steel blades maintain sharpness over extended periods, enabling efficient grating while meeting strict hygiene standards required in both household and commercial kitchens.The material’s ability to withstand frequent washing, exposure to moisture, and intensive use makes it the preferred choice among professional chefs and foodservice establishments. Additionally, stainless steel graters often offer enhanced structural stability and longer product life cycles, which contributes to strong consumer preference for premium kitchen tools.Plastic-bodied graters with stainless steel blades are commonly used in economy and mid-range products. These graters offer lightweight construction, ergonomic handles, and lower manufacturing costs, making them attractive to price-sensitive consumers. Many manufacturers are also incorporating food-grade, BPA-free plastics to ensure safety while maintaining affordability.

Ceramic graters are gaining popularity in niche and specialty markets due to their unique surface texture and aesthetic appeal. These graters are often used for delicate grating applications such as ginger, garlic, and citrus zest. Their non-reactive properties and distinctive design make them appealing to consumers seeking specialized culinary tools.Aluminum graters primarily serve the budget segment due to their lower production cost and lightweight characteristics. Although less durable than stainless steel alternatives, they remain widely used in entry-level products.Meanwhile, hybrid composite materials are emerging in premium kitchen tools. These products combine stainless steel blades with reinforced polymers or silicone components to improve grip comfort, durability, and aesthetic design. As consumers increasingly seek ergonomic and visually appealing kitchenware, hybrid material graters are expected to gain traction in the premium segment.

Distribution Channel Insights

The cheese grater market is distributed through offline and online retail channels. Offline retail channels currently dominate global sales, supported by the strong presence of supermarkets, hypermarkets, department stores, and kitchenware specialty stores. Consumers often prefer purchasing kitchen tools in physical stores where they can evaluate product quality, handle comfort, blade sharpness, and build durability before making a purchase.Kitchenware specialty retailers also provide expert guidance and curated product selections, which strengthens consumer confidence and drives sales of premium graters. Furthermore, large retail chains frequently offer bundled kitchen tool sets and promotional discounts that encourage in-store purchases.

However, online retail is the fastest-growing distribution channel. The rapid expansion of e-commerce platforms has significantly improved product accessibility, enabling consumers to explore a broader range of brands, product designs, and price points. Online platforms also allow niche and emerging brands to compete with established manufacturers by offering innovative designs and specialized products.Another major advantage of online retail is the availability of customer reviews, product demonstrations, and price comparison tools. These features help consumers make informed purchasing decisions while also increasing transparency in the marketplace. Additionally, the growing popularity of direct-to-consumer (DTC) sales models and digital marketing strategies is expected to further accelerate online market growth.

End-Use Insights

The cheese grater market is segmented into household consumers, foodservice & horeca establishments, and food processing industries. Household consumers represent the largest end-use segment, accounting for nearly 64% of global demand. This dominance is primarily driven by the widespread use of graters in everyday cooking activities such as preparing pasta, salads, baked dishes, and garnishes.Households often require versatile and durable kitchen tools for routine meal preparation, which ensures consistent replacement purchases over time. The increasing popularity of home cooking, culinary experimentation, and social media-driven food trends has further encouraged consumers to invest in specialized kitchen tools such as microplane graters and premium stainless-steel models.

The foodservice and horeca sector is the fastest-growing end-use segment, supported by the rapid expansion of restaurants, cafes, pizzerias, and catering services worldwide. Commercial kitchens require high-performance graters that can process large volumes of ingredients quickly while maintaining consistency and food presentation standards. As the global hospitality industry continues to expand, demand for durable and efficient grating equipment is expected to rise significantly.Food processing industries represent an emerging segment within the market. Small-scale cheese producers, artisanal food manufacturers, and specialty food processors increasingly rely on efficient grating solutions to prepare ingredients for packaged products, ready-to-eat meals, and processed foods. This trend is particularly visible among specialty cheese producers and gourmet food brands that emphasize freshly grated ingredients to enhance product quality.

Explore more data points, trends and opportunities Download Free Sample Report

Cheese Grater Market Segmentations

By Product Type

- Box Graters

- Rotary Graters

- Flat / Handheld Graters

- Microplane / Zester Graters

- Electric Cheese Graters

- Multi-Functional Grater Systems

By Material Type

- Stainless Steel

- Plastic Body with Steel Blades

- Ceramic Graters

- Aluminum Graters

- Composite & Hybrid Materials

By Operation Mode

- Manual Graters

- Electric / Automatic Graters

By Distribution Channel

- Online Retail

- Supermarkets & Hypermarkets

- Kitchenware Specialty Stores

- Department Stores

- Institutional & Horeca Supply

By End User

- Household Consumers

- Foodservice & Horeca

- Food Processing Industry

- Commercial Catering Services

Regional Insights

North America

North America represents one of the largest markets for cheese graters, supported by high per-capita cheese consumption and well-established kitchenware retail networks. The United States dominates regional demand due to widespread adoption of Western cuisine and high consumer spending on premium kitchen tools. Canada also contributes significantly to market growth through strong household demand and an expanding restaurant industry.Several key factors drive market growth across North America. The region has one of the highest levels of cheese consumption globally, which naturally increases the demand for efficient grating tools. The strong presence of organized retail chains and specialty kitchenware stores further supports product accessibility and consumer awareness. Additionally, the rising popularity of home cooking, influenced by culinary television programs and online cooking content, is encouraging consumers to invest in high-quality kitchen accessories.

Europe

Europe accounts for the largest share of the global cheese grater market, representing approximately 31% of total revenue in 2025. Countries such as Italy, Germany, France, and the United Kingdom are major contributors due to strong culinary traditions that emphasize freshly grated cheese. Italian cuisine in particular relies heavily on freshly grated parmesan and other hard cheeses, creating sustained demand for high-quality graters.Regional market growth is further supported by Europe's well-developed kitchenware manufacturing sector and consumer preference for durable stainless-steel tools. The strong presence of premium kitchen brands and artisanal cookware manufacturers also encourages innovation in grater design and materials. Additionally, increasing consumer interest in gourmet cooking and traditional recipes continues to support steady demand for specialized kitchen tools across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the cheese grater market, driven by increasing disposable incomes and expanding adoption of Western cuisines. China, India, Japan, and South Korea are experiencing rising demand for kitchen accessories as middle-class households invest in modern cooking equipment.The rapid expansion of international restaurant chains, pizza outlets, and bakery franchises across major urban centers is also contributing to increased commercial demand for cheese graters. Additionally, the growth of e-commerce platforms in the region has improved access to international kitchenware brands and specialty culinary tools. Rising urbanization, changing dietary preferences, and the increasing influence of global food trends are expected to further accelerate market growth in Asia-Pacific.

Latin America

Latin America is witnessing steady growth in cheese grater demand, particularly in Brazil and Mexico. Expanding supermarket chains and rising consumption of processed and fusion foods are supporting sales of kitchen preparation tools.Another major driver in the region is the growing restaurant and hospitality industry in large metropolitan areas. Urban consumers are increasingly adopting international cuisines that frequently require grated cheese as a key ingredient. Additionally, improvements in retail infrastructure and the expansion of modern trade channels are making kitchenware products more accessible to consumers across the region.

Middle East & Africa

The Middle East and Africa region is experiencing moderate growth in the cheese grater market, supported by the expansion of hospitality industries and tourism-driven foodservice sectors. Countries such as the United Arab Emirates and Saudi Arabia are seeing rising demand from restaurants and hotels that require efficient food preparation tools.Growing urbanization, increasing disposable incomes, and greater exposure to international cuisines are also encouraging household adoption of specialized kitchen tools. Furthermore, the rapid expansion of modern retail formats, including shopping malls and hypermarkets, is improving product availability and supporting the growth of the kitchenware market across the region.

Key Players in the Cheese Grater Market

- OXO International

- Microplane (Grace Manufacturing)

- Zyliss

- Cuisinart

- KitchenAid

- WMF Group

- Zwilling J.A. Henckels

- Joseph Joseph Ltd.

- Brabantia

- Tescoma

- Fackelmann GmbH

- Gefu GmbH

- Norpro Inc.

- Leifheit AG

- Victorinox