Toothfish Market Size

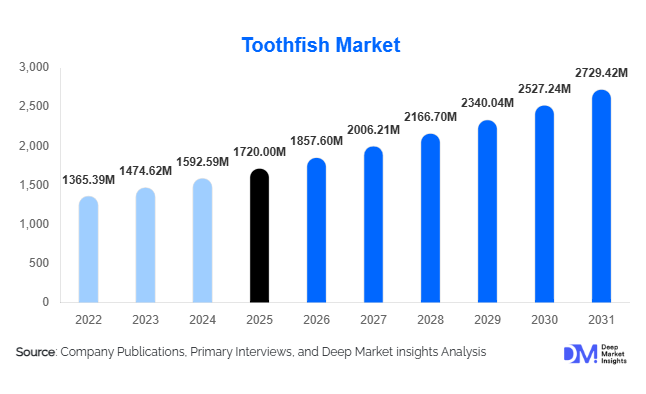

According to Deep Market Insights, the global toothfish market size was valued at USD 1,720 million in 2025 and is projected to grow from USD 1,857.60 million in 2026 to reach USD 2,729.42 million by 2031, expanding at a CAGR of 8.0% during the forecast period (2026–2031). The toothfish market growth is primarily driven by rising demand for premium seafood, increasing global consumption of high-value protein sources, and the expansion of luxury dining and hospitality industries across developed and emerging economies.

Key Market Insights

- Premium seafood consumption is rising globally, with toothfish gaining popularity in fine dining due to its rich flavor and texture.

- Strict fishing regulations and quotas are maintaining supply discipline, supporting price stability and premium positioning.

- North America dominates the market, driven by strong demand from upscale restaurants and high-income consumers.

- Asia-Pacific is the fastest-growing region, fueled by rising disposable incomes and expanding luxury food culture.

- Frozen and value-added formats are gaining traction, enabling wider global distribution and retail penetration.

- Technological advancements in cold chain logistics are improving product quality and extending shelf life for exports.

What are the latest trends in the toothfish market?

Shift Toward Sustainable and Certified Seafood

The toothfish market is witnessing a strong shift toward sustainability, with certifications such as MSC becoming critical for market access, particularly in North America and Europe. Buyers are increasingly prioritizing traceability, ethical sourcing, and compliance with international fishing standards. Companies are investing in digital traceability tools, including blockchain, to ensure transparency across the supply chain. This trend is also influencing purchasing decisions in retail and foodservice sectors, where sustainability credentials are becoming a competitive differentiator. As environmental concerns grow, suppliers adhering to regulated fishing quotas and conservation practices are better positioned to command premium prices and secure long-term contracts with global buyers.

Expansion of Value-Added and Retail-Oriented Products

Traditionally dominated by whole fish and fillets sold to foodservice providers, the market is now expanding into value-added segments such as smoked, marinated, and ready-to-cook toothfish products. These formats cater to premium retail consumers seeking convenience without compromising quality. Advances in packaging technologies, including vacuum sealing and modified atmosphere packaging (MAP), are enhancing shelf life and enabling wider distribution. Retail chains and online seafood platforms are increasingly incorporating toothfish into their premium product portfolios, broadening the consumer base beyond restaurants and luxury hotels.

What are the key drivers in the toothfish market?

Rising Demand for Premium Seafood

The growing global appetite for high-quality seafood is a major driver for the toothfish market. Consumers in developed regions are increasingly willing to pay a premium for superior taste, nutritional value, and exclusivity. Toothfish, marketed as Chilean sea bass, is widely recognized for its buttery texture and versatility, making it a staple in gourmet cuisine. The expansion of luxury dining establishments and high-end hospitality services is further accelerating demand.

Supply Regulation Supporting Price Stability

Strict regulatory frameworks governing toothfish fishing, particularly in Antarctic regions, have created a controlled supply environment. Organizations such as CCAMLR enforce quotas to ensure sustainability, limiting overfishing and maintaining ecological balance. This supply constraint enhances product scarcity, which in turn supports higher price realization and stable profit margins for producers and exporters.

Advancements in Cold Chain and Logistics

Technological improvements in freezing, storage, and transportation are significantly boosting the global reach of toothfish. Techniques such as individually quick freezing (IQF) and advanced cold storage systems ensure that product quality is preserved during long-distance shipping. This has enabled exporters to tap into new markets, particularly in Asia-Pacific and the Middle East, where demand for premium seafood is rapidly increasing.

What are the restraints for the global market?

Limited Supply Due to Fishing Quotas

The toothfish market faces inherent supply limitations due to strict fishing quotas and geographic concentration of fishing zones. These constraints restrict volume growth and create dependency on a limited number of regions, making the market vulnerable to regulatory changes and environmental factors.

High Pricing Limiting Mass Adoption

Toothfish remains a premium product with high pricing compared to other seafood categories. This restricts its consumption primarily to high-income consumers and luxury foodservice segments. Price sensitivity in emerging markets poses a challenge for broader market expansion.

What are the key opportunities in the toothfish industry?

Emerging Demand from Asia and the Middle East

Rapid economic growth and rising affluence in countries such as China, South Korea, and the UAE are creating new opportunities for toothfish exporters. The expansion of luxury dining and hospitality sectors in these regions is driving demand for premium seafood. Increasing exposure to international cuisines and fine dining trends is further boosting consumption, making these markets key growth drivers for the industry.

Traceability and Premium Branding

As consumers become more conscious about sustainability, companies that invest in transparent supply chains and certified sourcing can differentiate themselves. Traceability systems not only ensure compliance with regulations but also enhance brand value. Premium branding based on sustainability and quality assurance allows companies to command higher margins and build long-term customer loyalty.

Innovation in Value-Added Products

The development of ready-to-cook and ready-to-eat toothfish products presents significant growth potential. These innovations cater to changing consumer lifestyles, particularly in urban markets where convenience is a key factor. By diversifying product offerings, companies can expand their reach into retail channels and attract new customer segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1720 Million |

| Market Size in 2026 | USD 1857.60 Million |

| Market Size in 2031 | USD 2729.42 Million |

| CAGR | 8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Species Type Insights

The global toothfish market is overwhelmingly dominated by Patagonian toothfish, which accounts for approximately 78% of the total market share in 2025. This dominance is not merely a function of supply availability but is deeply rooted in strong global branding, particularly its commercial identity as Chilean sea bass. Over the years, Patagonian toothfish has built a premium perception among consumers and chefs, becoming synonymous with high-end seafood dining across North America, Europe, and parts of Asia-Pacific. Its firm texture, mild flavor, and versatility in gourmet cuisine have positioned it as a staple in fine dining menus, thereby reinforcing its market leadership.The leading segment driver for Patagonian toothfish lies in its established global supply chain networks and consistent demand from premium foodservice operators. Unlike Antarctic toothfish, which faces stricter catch limitations due to environmental concerns and regulatory frameworks, Patagonian toothfish benefits from relatively stable harvesting quotas and more developed fisheries management systems. This ensures a steady supply that aligns with the needs of international markets. Furthermore, increasing consumer awareness of sustainable sourcing, supported by certifications such as MSC (Marine Stewardship Council), has enhanced the credibility and acceptance of Patagonian toothfish products. While Antarctic toothfish occupies a niche segment due to its limited availability and higher price point, its contribution remains comparatively small. Going forward, the dominance of Patagonian toothfish is expected to persist, supported by strong brand equity, expanding distribution channels, and continuous demand from affluent consumer segments.

Product Form Insights

Frozen fillets represent the leading product form in the global toothfish market, accounting for around 42% of the overall market share. This segment’s leadership is driven by its unmatched logistical advantages, particularly in the context of international seafood trade. Frozen fillets offer extended shelf life, reduced spoilage risk, and greater flexibility in storage and transportation, making them highly suitable for export-oriented markets. As toothfish is predominantly harvested in remote Southern Ocean regions, freezing at sea and subsequent cold chain logistics are essential to maintaining product quality until it reaches end consumers.The primary driver for the dominance of frozen fillets is the increasing globalization of seafood supply chains combined with rising demand from international foodservice operators. Restaurants, hotels, and catering services prefer frozen fillets due to their consistency in portion size, ease of preparation, and year-round availability. Additionally, advancements in freezing technologies, such as flash freezing and vacuum sealing, have significantly improved the preservation of texture and flavor, narrowing the quality gap between fresh and frozen products.While whole fish and fresh fillets continue to serve niche markets, particularly in upscale restaurants that prioritize freshness and presentation, their limited shelf life and higher transportation costs restrict their widespread adoption. Meanwhile, value-added products, including marinated, smoked, and ready-to-cook variants, are gaining traction in retail channels. These products cater to evolving consumer preferences for convenience and premium at-home dining experiences. As retail penetration increases and consumer lifestyles shift towards convenience-driven consumption, the value-added segment is expected to witness accelerated growth, although frozen fillets will likely retain their dominant position due to their foundational role in global trade.

Processing Type Insights

The toothfish market is unique in that it is almost entirely dependent on wild-caught production, with this segment accounting for nearly 100% of the market. Unlike many other seafood categories where aquaculture has become a significant contributor, toothfish farming remains commercially unviable due to biological, environmental, and economic challenges. This reliance on wild capture reinforces the exclusivity and premium positioning of toothfish in the global seafood market.The leading driver for this segment is the inherent limitation in aquaculture feasibility, which ensures that supply remains tightly controlled and aligned with sustainable fishing quotas. Regulatory bodies such as the Commission for the Conservation of Antarctic Marine Living Resources (CCAMLR) play a critical role in managing toothfish fisheries, implementing strict catch limits, monitoring systems, and traceability requirements. These measures not only protect marine ecosystems but also enhance the market value of toothfish by ensuring its status as a sustainably sourced product.The wild-caught nature of toothfish also contributes to its high price point, as harvesting operations are conducted in challenging and remote oceanic environments, leading to elevated operational costs. However, this exclusivity is a key factor driving demand among premium consumers and high-end foodservice establishments. Sustainability certifications and traceability initiatives further strengthen consumer confidence, particularly in regions where ethical sourcing is a major purchasing criterion. As a result, the wild-caught segment is expected to maintain its absolute dominance, with sustainability and regulatory compliance acting as both constraints and value drivers.

Distribution Channel Insights

Direct B2B distribution channels dominate the toothfish market, accounting for approximately 55% of the total market share. This dominance is primarily driven by the strong and consistent demand from foodservice operators, including fine dining restaurants, luxury hotels, and catering services. These establishments require reliable supply chains, consistent product quality, and bulk purchasing capabilities, all of which are effectively facilitated through direct B2B relationships between suppliers, distributors, and end-users.The key driver for this segment is the entrenched demand from the global hospitality industry, which relies heavily on premium seafood offerings to enhance menu appeal and customer experience. Toothfish, with its high culinary value, is a preferred choice for chefs aiming to deliver upscale dining experiences. As a result, suppliers prioritize direct partnerships with foodservice clients to ensure timely delivery and maintain quality standards.Seafood distributors and wholesalers also play a crucial intermediary role, particularly in bridging the gap between remote fishing operations and urban consumption centers. Their expertise in cold chain logistics, inventory management, and regulatory compliance is essential for maintaining product integrity throughout the supply chain. Meanwhile, retail channels are gradually expanding, supported by the growth of premium supermarkets, specialty seafood stores, and online platforms. The rise of e-commerce in the seafood sector has further enabled consumers to access high-quality toothfish products from the comfort of their homes. Despite this growth, B2B channels are expected to remain dominant due to the scale and consistency of demand from the foodservice sector.

End-Use Insights

The foodservice industry represents the largest end-use segment in the toothfish market, accounting for nearly 62% of the overall market share. This segment’s leadership is closely tied to the premium positioning of toothfish, which aligns seamlessly with the requirements of fine dining establishments and luxury hospitality services. Restaurants and hotels leverage toothfish as a high-value menu item, often featuring it in signature dishes that command premium pricing.The primary driver for this segment is the growing global demand for luxury dining experiences, particularly in urban centers and tourist destinations. As consumers increasingly seek unique and high-quality culinary experiences, restaurants are incorporating premium seafood options such as toothfish to differentiate their offerings. The rise of international tourism and the expansion of high-end hospitality infrastructure further contribute to this trend, creating sustained demand from the foodservice sector.Retail consumption, while smaller in comparison, is steadily gaining momentum. The increasing availability of packaged and value-added toothfish products in premium retail outlets is encouraging consumers to experiment with gourmet cooking at home. Additionally, the influence of digital media, cooking shows, and celebrity chefs has heightened consumer awareness and interest in premium seafood. As disposable incomes rise and culinary preferences evolve, the retail segment is expected to grow, although it will continue to complement rather than surpass the dominance of the foodservice industry.

Preservation Method Insights

Frozen preservation methods dominate the toothfish market, accounting for approximately 65% of the total market share. This dominance is intrinsically linked to the geographical and logistical realities of toothfish harvesting, which occurs in remote and often inhospitable regions of the Southern Ocean. Freezing is essential to preserving the quality and safety of the product during long transit periods, enabling it to reach distant markets without significant degradation.The leading driver for this segment is the necessity of maintaining product integrity across extended global supply chains. Advanced freezing techniques, including blast freezing and individually quick frozen (IQF) processes, ensure that toothfish retains its texture, flavor, and nutritional value. These technologies have significantly enhanced the appeal of frozen products, making them nearly indistinguishable from fresh alternatives in terms of quality.Fresh and chilled products, while offering superior sensory attributes, are primarily limited to local or regional markets due to their shorter shelf life and higher transportation costs. However, innovations in packaging, such as modified atmosphere packaging (MAP) and vacuum sealing, are gradually extending the viability of fresh products in select premium markets. Despite these advancements, frozen preservation is expected to remain the dominant method, driven by its critical role in enabling global trade and ensuring consistent product availability.

Explore more data points, trends and opportunities Download Free Sample Report

Toothfish Market Segmentations

By Species Type

- Patagonian Toothfish

- Antarctic Toothfish

By Product Form

- Whole Fish

- Frozen Whole Fish

- Fillets

- Frozen Fillets

- Value-Added Products

By Distribution Channel

- Direct B2B

- Seafood Distributors & Wholesalers

- Retail

- Online Seafood Platforms

By End-Use Industry

- Foodservice Industry

- Retail Consumers

- Institutional Buyers

Regional Insights

North America

North America accounts for approximately 34% of the global toothfish market share, making it the largest consumption region. The United States, in particular, represents a significant demand center due to its well-established seafood culture and high consumer purchasing power. The region’s growth is driven by several key factors, including rising disposable incomes, a strong preference for premium and sustainable seafood, and the widespread presence of fine dining establishments that feature toothfish as a signature offering.Another critical growth driver in North America is the increasing emphasis on sustainability and traceability. Consumers are becoming more conscious of the environmental impact of their food choices, leading to a growing demand for certified seafood products. This trend aligns well with the toothfish market, where strict regulatory frameworks and sustainability certifications enhance consumer confidence. Additionally, the expansion of premium retail chains and online seafood platforms is improving accessibility, enabling a broader consumer base to purchase toothfish products. The region’s robust cold chain infrastructure further supports market growth by ensuring efficient distribution and product quality.

Europe

Europe holds around 28% of the global market share, with key markets including France, the United Kingdom, and Germany. The region is characterized by a strong emphasis on sustainability, quality, and regulatory compliance, which significantly influences consumer purchasing behavior. European consumers are highly discerning and prioritize ethically sourced seafood, making sustainability certifications a critical factor in market growth.Retail channels are also evolving, with an increasing number of specialty seafood stores and premium supermarkets offering high-quality toothfish products. The growing popularity of home cooking, particularly following shifts in consumer behavior, is further supporting retail demand. As sustainability continues to be a central theme in European markets, the region is expected to maintain steady growth in the coming years.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the toothfish market, with a projected CAGR exceeding 9%. Major markets such as China and Japan are driving this growth, supported by rising affluence, expanding middle-class populations, and increasing exposure to international cuisines. The region’s evolving culinary landscape is creating new opportunities for premium seafood products, including toothfish.E-commerce platforms and modern retail formats are also playing a crucial role in expanding market access. Consumers in urban centers are increasingly purchasing premium seafood online, supported by improvements in cold chain logistics and delivery infrastructure. As consumer awareness and demand for high-quality seafood continue to rise, Asia-Pacific is expected to remain a key growth engine for the global toothfish market.

Latin America

Latin America serves as a critical supply hub for the global toothfish market, with countries such as Chile and Argentina playing a dominant role in production and export activities. The region’s extensive coastline and proximity to key fishing grounds make it a strategic center for toothfish harvesting operations.The primary driver for regional growth is its strong export-oriented industry, which is supported by well-established fisheries management systems and international trade partnerships. Chile, in particular, has developed a robust reputation as a leading exporter of Patagonian toothfish, leveraging advanced fishing technologies and sustainable practices to meet global demand. While domestic consumption remains relatively limited compared to export volumes, there is a gradual increase in local demand driven by rising incomes and expanding tourism sectors.Infrastructure development, including improvements in port facilities and cold storage capabilities, is further enhancing the region’s competitiveness in the global market. As sustainability and traceability continue to gain importance, Latin American producers are increasingly adopting certification standards to strengthen their position in international markets.

Middle East & Africa

The Middle East and Africa region is emerging as a promising market for toothfish, driven by the rapid growth of luxury tourism and hospitality sectors. Countries such as the United Arab Emirates and Saudi Arabia are at the forefront of this growth, with significant investments in high-end hotels, resorts, and fine dining establishments.In Africa, the market plays a dual role as both a supply region and a growing consumption market. Coastal countries with access to fishing grounds contribute to the global supply of toothfish, while urbanization and economic development are gradually increasing local demand. As infrastructure and supply chain capabilities improve, the region is expected to witness steady growth, supported by both export opportunities and rising domestic consumption.

Key Players in the Toothfish Market

- Austral Fisheries

- Sanford Limited

- Pesca Chile

- Délifrance Seafood Group

- Glacier Fish Company

- Ervik Havfiske

- Argos Froyanes

- Consolidated Fisheries

- Fortune Fish & Gourmet

- Lee Fishing Company

- Iberconsa

- Antarctic Fishing Company

- Southern Ocean Fishing

- Maruha Nichiro Corporation

- Nippon Suisan Kaisha