Global Vegetable Peeler Market Size

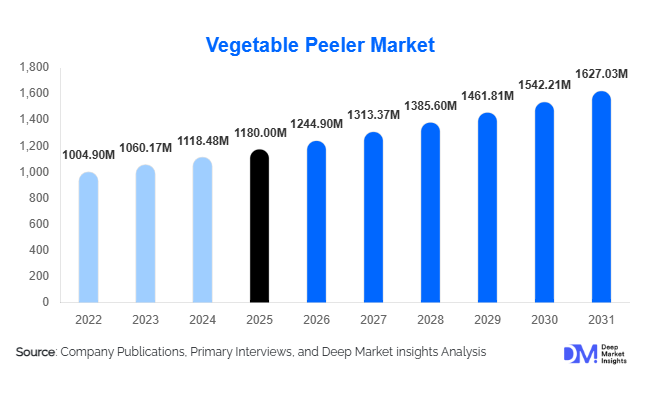

According to Deep Market Insights, the global vegetable peeler market size was valued at USD 1,180 million in 2026 and is projected to grow from USD 1,244.90 million in 2026 to reach USD 1,627.03 million by 2031, expanding at a CAGR of 5.5% during the forecast period (2026–2031). The vegetable peeler market growth is primarily driven by rising home cooking trends, increasing demand for ergonomic and electric peelers, and growing adoption in commercial kitchens and food processing industries worldwide.

Key Market Insights

- Manual peelers dominate globally, due to affordability, simplicity, and long-standing household usage.

- Electric and smart peelers are gaining traction, particularly in developed markets, for time-saving and efficiency benefits.

- North America and Europe account for the largest market share, driven by high disposable income, urbanized households, and strong e-commerce penetration.

- Asia-Pacific is the fastest-growing region, fueled by expanding middle-class incomes, urbanization, and growth of the foodservice sector in China and India.

- Sustainability trends are influencing consumer choices, with eco-friendly materials and recyclable components becoming key differentiators.

- Distribution channels are evolving, with online retail and direct-to-consumer sales increasing reach and providing broader product variety.

What are the latest trends in the vegetable peeler market?

Rise of Smart and Electric Peelers

Smart peelers with IoT connectivity, app integration, and predictive blade maintenance are emerging, targeting tech-savvy consumers and professional kitchens. Electric peelers are increasingly adopted in commercial kitchens and large households for time-efficient food preparation. These innovations offer precise, safe, and quick peeling, positioning them as high-value alternatives to traditional manual peelers.

Eco-Friendly and Sustainable Materials

Consumers are increasingly choosing peelers made from stainless steel, recycled plastics, and biodegradable composites. Manufacturers are offering products with replaceable blades and eco-conscious packaging to reduce waste. Sustainability has become a market differentiator, particularly in Europe and North America, aligning with regulatory pushes for environmentally friendly manufacturing.

What are the key drivers in the vegetable peeler market?

Growth of Home Cooking and Health-Conscious Lifestyles

The global trend toward fresh and healthy cooking at home has significantly boosted demand for efficient kitchen tools. Consumers across age groups are increasingly incorporating vegetable peelers as essential kitchen staples, motivated by convenience, time-saving, and health benefits.

Commercial Kitchen Efficiency and Food Processing Needs

Restaurants, hotels, and food processing industries are adopting high-quality peelers to optimize workflows. Consistent peeling quality, labor reduction, and ergonomic designs have strengthened demand in professional kitchens, supporting both manual and electric peeler segments.

Ergonomic and Multi-Functional Innovations

Ergonomic handles, multi-functional blades, and safety-focused designs are attracting a broader consumer base, including older populations and professional chefs. These innovations enhance user comfort, reduce injury risk, and differentiate products in a competitive market.

What are the restraints for the global market?

Competition from Multi-Functional Kitchen Appliances

Standalone peelers face competition from food processors and slicers that offer peeling alongside other functions. Integrated kitchen appliances can reduce the need for individual peelers, restraining growth, especially in price-sensitive markets.

Raw Material Price Volatility

Fluctuating prices of stainless steel and plastics can increase manufacturing costs, impacting margins and retail prices. Smaller manufacturers are particularly vulnerable to these changes, which may hinder market expansion.

What are the key opportunities in the vegetable peeler market?

Smart and IoT-Enabled Kitchen Solutions

Smart peelers equipped with IoT features offer usage analytics, maintenance alerts, and integration with other kitchen appliances. Early adoption in developed markets presents opportunities for premium pricing and enhanced consumer engagement, creating new revenue streams for manufacturers.

Sustainable and Eco-Friendly Products

Eco-conscious consumers are driving demand for peelers made with recyclable or biodegradable materials. Manufacturers focusing on sustainability can differentiate themselves and gain loyalty from environmentally aware customers, particularly in Europe and APAC.

Emerging Market Growth

Rapid urbanization, rising disposable incomes, and expanding foodservice industries in APAC countries like China and India present a significant growth opportunity. Localized production and government support for food processing equipment further enhance market accessibility and adoption.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1180 Million |

| Market Size in 2026 | USD 1244.90 Million |

| Market Size in 2031 | USD 1627.03 Million |

| CAGR | 5.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Manual peelers continue to dominate the global market, capturing approximately 65% of the share, primarily due to their affordability, simplicity, and widespread household adoption. These peelers are highly favored for everyday culinary tasks as they require minimal maintenance and are easy to handle for diverse food preparation needs. The demand for manual peelers is particularly strong in regions where cost sensitivity and traditional cooking practices prevail. In contrast, electric peelers are rapidly gaining momentum, especially within professional kitchens, premium households, and urban areas where convenience and efficiency are prioritized. The increasing automation in commercial kitchens, coupled with a growing preference among consumers for time-saving appliances, underpins the expansion of this segment. Additionally, smart or connected peelers are emerging as a niche but high-potential segment, integrating digital technology to provide precise peeling, usage tracking, and connectivity with other smart kitchen devices. These innovations are attracting tech-savvy consumers and early adopters, positioning this segment for steady growth as smart kitchen solutions and the Internet of Things (IoT) continue to reshape household appliance trends globally.

Material Insights

Stainless steel peelers lead the market with a 40% share, driven by their durability, corrosion resistance, and hygienic properties, making them highly suitable for both household and commercial use. They are preferred by premium consumers and professional kitchens due to their long lifespan and ability to withstand frequent use without compromising performance. Plastic peelers, offering lightweight design, cost-effectiveness, and ease of handling, continue to be popular among mid-range households, particularly in regions where affordability is a key consideration. Rising awareness of sustainability is creating a new wave of demand for ceramic and eco-composite peelers, which appeal to environmentally conscious consumers seeking sharpness, durability, and design aesthetics while minimizing ecological impact. The choice of material is increasingly influenced by consumer segments, with stainless steel dominating professional and premium markets, plastic catering to mass-market households, and eco-friendly alternatives emerging as a growth driver in sustainability-focused regions.

End-Use Insights

The household segment dominates the market, capturing around 60% of global demand. This growth is fueled by rising health consciousness, increasing home cooking trends, and the convenience of preparing meals at home. Consumers are actively seeking tools that simplify daily culinary tasks, enhance efficiency, and improve food presentation. Commercial kitchens, encompassing restaurants, hotels, catering services, and institutional kitchens, are increasingly adopting electric and semi-automatic peelers to enhance operational efficiency, reduce labor costs, and maintain consistent product quality. The food processing sector is another key driver, where mechanized peeling solutions help optimize productivity, reduce waste, and standardize outputs for large-scale operations. Export-oriented food businesses are also contributing to incremental growth, as they demand high-quality, durable peelers that meet international standards. Overall, while household adoption remains the largest contributor, commercial and institutional use is emerging as a crucial factor in market expansion.

Distribution Channel Insights

Online retail commands a significant share of approximately 45%, fueled by its convenience, wide product selection, and competitive pricing. E-commerce platforms have become central to market penetration, particularly in regions with high urbanization and internet penetration. These platforms enable consumers to access a broader variety of peelers, compare features, and take advantage of home delivery, making them especially attractive for premium and innovative products. Physical retail channels, including supermarkets, specialty kitchenware stores, and direct-to-consumer outlets, continue to play an essential role, particularly for products where in-store experience, tactile assessment, and brand visibility influence purchase decisions. Omnichannel strategies, combining online convenience with offline experiential engagement, are increasingly adopted by brands to maximize market coverage and enhance consumer trust. The growth of online sales is particularly pronounced in North America and Asia-Pacific, reflecting the strong inclination of consumers in these regions towards digital shopping and access to international brands.

Explore more data points, trends and opportunities Download Free Sample Report

Vegetable Peeler Market Segmentations

By Product Type

- Manual Peelers

- Electric Peelers

- Smart/Connected Peelers

By Material

- Stainless Steel

- Plastic

- Ceramic

- Aluminum

- Silicone/Composite Eco-materials

By End Use

- Household/Home Kitchen

- Commercial Kitchens

- Food Processing & Catering

- Institutional

By Distribution Channel

- Online Retail & Marketplaces

- Supermarkets & Hypermarkets

- Specialty Kitchenware Stores

- Department Stores & Wholesale

Regional Insights

North America

North America represents one of the most mature markets, holding approximately 32% of the 2025 global share. Growth is supported by high disposable incomes, advanced retail infrastructure, and widespread e-commerce adoption, which make both manual and electric peelers readily accessible to consumers. The increasing focus on health-conscious lifestyles, home cooking, and convenience has fueled interest in ergonomic and electric peelers that save time and improve kitchen efficiency. Commercial adoption is robust, particularly in restaurants, hotels, and catering services, where operational efficiency and consistent quality are critical. Regulatory standards emphasizing product safety, durability, and hygiene favor premium peelers, further driving market expansion. Additionally, innovation in connected kitchen appliances and smart peelers aligns with the region’s tech-savvy consumer base, creating opportunities for high-end product penetration.

Europe

Europe accounts for around 28% of the global market, driven by high demand for premium and eco-friendly peelers. Countries such as Germany, France, and the U.K. are key contributors, with consumer preferences shaped by established culinary traditions, higher disposable incomes, and growing sustainability awareness. Households in Europe favor durable, ergonomically designed, and aesthetically appealing peelers, while commercial kitchens prioritize efficiency and productivity-enhancing tools. Regulatory initiatives promoting eco-friendly products, combined with consumer interest in zero-waste cooking, are increasing the adoption of ceramic and sustainable composite peelers. Mature retail channels, including both online marketplaces and traditional kitchenware stores, provide extensive accessibility and visibility for brands. Innovation in design, sustainability, and ergonomics further supports market growth in this region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, with China and India leading the surge due to rapid urbanization, rising middle-class incomes, and expanding foodservice sectors. Increasing exposure to global culinary trends, coupled with rising standards of living, is boosting demand for both manual and electric peelers. The proliferation of e-commerce platforms and localized manufacturing capabilities reduces costs and increases accessibility, further accelerating adoption across urban and semi-urban populations. Institutional kitchens, restaurants, and processed food industries are contributing to commercial demand, while households are embracing premium and smart peelers to align with convenience and health-oriented cooking trends. Government initiatives supporting domestic production, quality standards, and innovation in kitchen appliances are additional growth drivers, making Asia-Pacific a high-potential region for market expansion.

Latin America

Latin America is witnessing steady growth in peeler demand, primarily led by Brazil, Argentina, and Mexico. Consumers typically prefer mid-range manual peelers due to price sensitivity and entrenched household cooking habits. The region’s market expansion is supported by the rise of modern retail chains, urban population growth, and increasing e-commerce penetration, which facilitate access to a broader range of products. Commercial kitchens, including restaurants, institutional cafeterias, and catering services, are emerging as significant buyers, seeking efficient peeling solutions for large-scale food preparation. Additionally, cross-border trade and export activities allow domestic manufacturers and international brands to target the growing consumer base, further enhancing market development. The interplay of affordability, convenience, and rising culinary awareness underpins continued regional growth.

Middle East & Africa

The Middle East and Africa (MEA) remain smaller but stable markets, driven primarily by urban centers, expatriate households, and tourism-related food services. Major cities and hospitality hubs support demand from commercial kitchens, hotels, and catering operations, while urban households increasingly adopt manual and electric peelers for convenience. Rising disposable incomes, evolving culinary practices, and awareness of high-quality kitchen tools are boosting demand for premium peelers. E-commerce expansion in the Middle East, coupled with retail network growth in African urban centers, is gradually enhancing accessibility and brand awareness. Key growth drivers include the increasing presence of modern kitchens, culinary tourism, and the gradual shift towards convenience-oriented, high-quality kitchen solutions across the region.

Key Players in the Vegetable Peeler Market

- Victorinox

- OXO

- Kuhn Rikon

- Zyliss

- Cuisinart

- KitchenAid

- Microplane

- Prepworks

- Norpro

- Fackelmann

- Alistar Europe

- Triangle (TRAMONTINA)

- Plazotta

- ADE Germany GmbH

- Tupperware (Premium Kitchen Range)