Textured Soy Protein Market Size

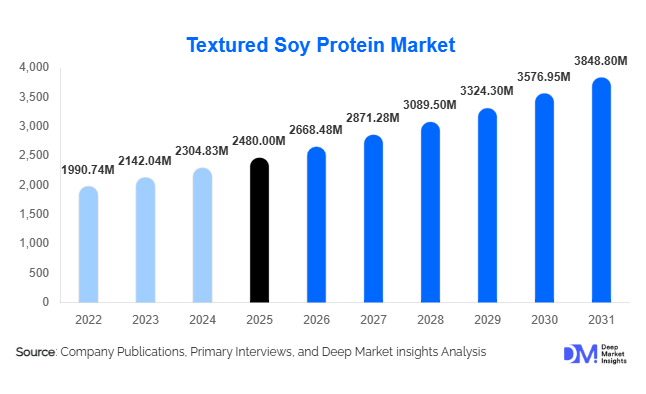

According to Deep Market Insights, the global textured soy protein market size was valued at USD 2,480 million in 2025 and is projected to grow from USD 2,668.48 million in 2026 to reach USD 3,848.80 million by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The textured soy protein market growth is primarily driven by rising global demand for plant-based meat alternatives, increasing protein fortification in processed foods, and cost-effective meat extension solutions adopted by large food processors.

Key Market Insights

- Meat alternatives represent the largest application segment, accounting for approximately 45% of the total market value in 2025.

- Textured soy concentrate dominates by product type, contributing nearly 42% of global revenue due to its cost-performance balance.

- Asia-Pacific leads the global market, holding around 37% share in 2025, driven by strong soy processing capacity and rising protein consumption.

- North America accounts for nearly 28% of global demand, led by the high penetration of plant-based diets in the United States.

- B2B direct sales channels dominate distribution, representing nearly 60% of global transactions.

- Non-GMO and organic variants are the fastest-growing nature segment, expanding at a higher-than-average CAGR due to clean-label demand.

What are the latest trends in the textured soy protein market?

Hybrid Meat and Reformulation Strategies

Food manufacturers are increasingly adopting hybrid meat formulations that combine animal protein with textured soy protein to reduce production costs and carbon footprints. This trend is particularly strong in North America and Europe, where sustainability commitments and ESG targets are influencing procurement decisions. TSP inclusion helps manufacturers maintain texture and protein content while lowering raw material volatility linked to meat pricing. Retailers are also introducing blended meat products positioned as transitional options for flexitarian consumers, expanding the addressable market base.

High-Moisture Extrusion and Texture Innovation

Advancements in extrusion technology are enabling improved fibrous structures that closely mimic whole-muscle meat textures. High-moisture extrusion lines are being deployed across new facilities in Asia and Europe, enhancing product quality and enabling premium positioning. Improved flavor-masking techniques and allergen-controlled production are further increasing product acceptance across mainstream food categories. These innovations are allowing manufacturers to target premium plant-based burgers, sausages, and ready meals.

What are the key drivers in the textured soy protein market?

Expansion of Plant-Based Diet Adoption

The global shift toward plant-based and flexitarian diets is a primary growth driver. Consumers are actively seeking protein alternatives with lower environmental impact. Foodservice chains and retail brands are responding by expanding plant-based portfolios, directly increasing demand for textured soy protein as a foundational ingredient.

Cost Efficiency Compared to Animal Protein

Volatility in beef and poultry markets, driven by feed price fluctuations and climate risks, has encouraged processors to integrate soy protein. TSP offers significant cost advantages, often 30–50% lower than certain meat formats, making it attractive for large-scale food manufacturers and institutional buyers.

What are the restraints for the global market?

Allergen and GMO Perception Challenges

Soy remains a recognized allergen in multiple regions, requiring mandatory labeling and limiting universal adoption. Additionally, consumer skepticism toward genetically modified soy in Europe and certain Asian markets increases demand for certified non-GMO variants, raising procurement complexity and cost.

Raw Material Price Volatility

Fluctuations in global soybean prices directly impact production costs. Weather disruptions in major producing countries such as the United States and Brazil can tighten supply and pressure margins for TSP manufacturers.

What are the key opportunities in the textured soy protein industry?

Emerging Market Protein Security Programs

Governments in Asia and Africa are investing in protein fortification programs to address nutritional gaps. Textured soy protein’s affordability and long shelf life make it suitable for public procurement in school feeding programs and food aid initiatives. Expansion of local processing facilities presents significant entry opportunities for global players.

Premium Non-GMO and Organic Product Lines

Rising clean-label demand in Europe and North America is opening premium pricing opportunities for certified organic and non-GMO TSP. Manufacturers investing in traceability systems and identity-preserved sourcing can secure higher margins and long-term supply contracts with multinational food brands.

Product Type Insights

Textured soy concentrate (TSC) holds the largest market share at approximately 42% in 2025, primarily driven by its balanced protein concentration (typically 65–70%) and strong cost-to-functionality ratio. TSC offers superior water-holding capacity and fibrous texture formation compared to textured soy flour, while remaining more economical than soy protein isolate. This makes it the preferred ingredient for large-scale plant-based meat manufacturers and processed meat extension applications. Additionally, TSC performs well in high-moisture extrusion systems, enabling improved meat analog textures, a key driver as global plant-based product launches accelerate.

Textured soy flour continues to serve price-sensitive applications, particularly in emerging markets across Asia and Africa, where affordability and nutritional fortification remain primary drivers. Its lower production cost and adaptability in blended protein systems make it suitable for institutional feeding programs and mass-market processed foods. Soy protein isolate variants, while smaller in overall share, are expanding rapidly in premium applications. Their higher protein purity (above 80%) and improved emulsification properties support clean-label formulations, high-protein retail products, and specialty plant-based SKUs. Growth in this segment is driven by rising consumer demand for high-protein diets and fortified convenience foods.

Form Insights

Granules and crumbles dominate the global market with nearly 38% share, driven by their versatility in minced meat substitutes, hybrid meat blends, and ready-to-eat meal applications. Their uniform particle size, rapid hydration capability, and compatibility with industrial mixing systems make them highly suitable for large food processors. As plant-based burger patties, meatballs, and taco fillings continue to gain traction globally, granulated forms remain the preferred format.

Chunks maintain strong demand in Asian cuisines and institutional catering environments, where larger textured pieces are preferred for traditional dishes and bulk food service operations. The growth in urban foodservice chains across the Asia-Pacific is reinforcing this demand. Flakes and powder formats are increasingly used in bakery, snack fortification, and protein-enriched cereals. Their ease of blending and ability to enhance protein content without significantly altering texture make them valuable for health-oriented product lines.

Application Insights

Meat alternatives represent the largest application segment, accounting for around 45% of global revenue. This leadership is driven by rapid product innovation in plant-based burgers, sausages, nuggets, and ready meals. The flexitarian consumer trend and retail expansion of plant-based product lines across North America and Europe continue to fuel this segment’s dominance.

Processed meat extension applications hold a substantial share, particularly in cost-sensitive and emerging markets. Meat processors incorporate textured soy protein to manage raw material costs, improve yield, and stabilize margins amid volatile meat prices. Bakery and snack fortification is an emerging but steadily growing niche, supported by rising demand for protein-enriched packaged foods. Animal feed applications provide a consistent baseline demand, especially in Latin America and parts of Asia, where cost-effective protein supplementation is essential.

Distribution Channel Insights

B2B direct sales dominate the market with nearly 60% share, reflecting the ingredient-centric and industrial nature of textured soy protein. Large food processors and multinational manufacturers rely on long-term procurement contracts to ensure supply stability and price predictability. Bulk purchasing, customized formulations, and technical support services strengthen supplier relationships within this channel.

Ingredient distributors play a critical role in regional market penetration, especially in fragmented emerging markets where smaller processors require lower minimum order volumes.Branded consumer packs sold via modern retail and e-commerce platforms are expanding in developed markets, particularly in North America and Europe, where home cooking trends and vegetarian meal preparation are rising.

End-Use Industry Insights

The food processing industry accounts for approximately 55% of total demand, valued at over USD 1,360 million in 2025. This segment’s dominance is driven by large-scale production of plant-based meals, processed meat blends, frozen foods, and packaged convenience products. Continuous reformulation strategies to reduce costs and improve sustainability metrics further strengthen this segment. Plant-based protein manufacturers represent the fastest-growing end-use segment, expanding at nearly 9% CAGR. Rapid product innovation cycles, venture capital investments in alternative protein startups, and retail shelf expansion are accelerating procurement volumes. Quick-service restaurants (QSRs) are increasingly incorporating plant-based menu options to capture flexitarian consumers. Global fast-food chains introducing soy-based alternatives are driving incremental industrial demand.

| By Product Type | By Form | By Application | By Distribution Channel | By End-Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global market with 37% share in 2025, supported by extensive soybean processing infrastructure and rising protein consumption. China alone represents nearly 18% of global demand, driven by its large domestic soy crushing capacity and expanding plant-based product launches. Government-backed food security programs and investment in domestic protein production further stimulate growth. In India, strong vegetarian dietary patterns, rapid urbanization, and expansion of packaged food manufacturing are key demand drivers. Southeast Asian countries are also witnessing increased adoption of cost-effective meat extension solutions, reinforcing regional growth.

North America

North America accounts for around 28% of the global market, with the United States contributing approximately 23%. The region’s growth is driven by high plant-based diet penetration, strong retail innovation, and extensive R&D investments in extrusion technology. Major food manufacturers are integrating textured soy protein into reformulated products to meet ESG targets. Canada supports growth through non-GMO production and export capabilities, strengthening supply chain resilience.

Europe

Europe holds roughly 22% market share, led by Germany, the U.K., and France. Strict labeling regulations, sustainability mandates, and strong consumer preference for non-GMO ingredients are key regional drivers. The European Green Deal and climate policy frameworks are encouraging protein diversification away from livestock. Retailers actively promote plant-based private labels, supporting steady procurement growth for textured soy protein suppliers.

Latin America

Latin America represents about 8% of global demand. Brazil plays a dual role as a major producer and exporter of soy derivatives, strengthening vertical integration across the value chain. Domestic growth is supported by cost-conscious food manufacturers using soy protein as a meat extender. Argentina and Mexico are also expanding processed food production, contributing incremental demand.

Middle East & Africa

The Middle East & Africa account for nearly 5% share but remain the fastest-growing region, expanding at close to 9% CAGR. Growth is driven by food security initiatives, rising protein imports, and government-supported diversification away from import-dependent meat supplies. GCC countries are investing in food processing infrastructure to enhance domestic production. In Africa, institutional feeding programs and urban packaged food expansion are gradually increasing the adoption of affordable plant-based proteins.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Textured Soy Protein Market

- Archer Daniels Midland (ADM)

- Cargill Incorporated

- International Flavors & Fragrances (IFF)

- CHS Inc.

- Bunge Limited

- Wilmar International

- Fuji Oil Holdings

- Sonic Biochem

- Devansoy Inc.

- Victoria Group

- Crown Soya Protein Group

- Shandong Yuxin Bio-Tech

- Bremil Group

- Nutraferma

- Solae (legacy brand under IFF)