Sucrose Esters Market Size

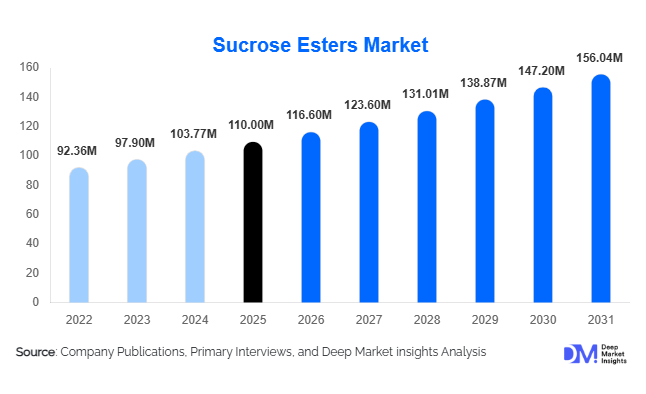

According to Deep Market Insights, the global sucrose esters market size was valued at USD 110 million in 2025 and is projected to grow from USD 116.60 million in 2026 to reach USD 156.04 million by 2031, expanding at a CAGR of 6% during the forecast period (2026–2031). The market growth is primarily driven by rising demand for natural emulsifiers in food & beverage, cosmetics, and pharmaceutical applications, increasing consumer preference for clean-label ingredients, and the expansion of industrial uses such as biodegradable surfactants and specialty coatings.

Key Market Insights

- Food & beverage applications are the largest end-use segment, with sucrose esters widely used as emulsifiers, foaming agents, and texture modifiers in bakery, dairy, and confectionery products.

- Personal care and cosmetic products are increasingly incorporating sucrose esters as plant-based surfactants, driven by the global shift toward natural, clean-label formulations.

- Asia Pacific dominates global consumption due to rapid industrialization, expanding processed food and cosmetic manufacturing, and growing awareness of functional food ingredients.

- North America and Europe remain key markets with established regulatory frameworks promoting natural emulsifiers in food and cosmetic formulations.

- Technological innovation and functional customization are reshaping product applications, allowing high-performance emulsifiers tailored to beverage, bakery, and pharmaceutical formulations.

- Export-driven demand is rising as emerging economies increase imports of high-grade sucrose esters from leading producers in Europe and North America.

What are the latest trends in the sucrose esters market?

Clean-Label and Natural Ingredient Demand

Consumer preference for clean-label and naturally derived ingredients is driving significant adoption of sucrose esters across food and personal care products. Manufacturers are increasingly replacing synthetic emulsifiers with sucrose esters to meet regulatory compliance and appeal to health-conscious consumers. This trend is especially strong in Europe and North America, where labeling regulations and consumer awareness reinforce demand for plant-based additives.

Technological and Functional Innovation

Advanced production techniques, such as enzyme-assisted esterification and high-purity fractionation, are enabling the creation of specialized sucrose ester grades with tailored hydrophilic-lipophilic balance (HLB) values. This allows precise formulation for beverages, bakery, confectionery, and pharmaceutical applications. Innovations also include nano-emulsion systems and functional blends to improve solubility, stability, and bioavailability, expanding the potential application scope.

What are the key drivers in the sucrose esters market?

Rising Demand in the Food & Beverage Industry

Processed and packaged food globally is boosting the demand for functional emulsifiers like sucrose esters. Products such as low-fat spreads, bakery items, confectionery, and dairy require stable emulsification, texture improvement, and shelf-life extension, making sucrose esters a preferred ingredient due to their natural origin and multifunctionality.

Growth in Personal Care and Pharmaceuticals

The rising adoption of plant-based and sustainable ingredients in personal care, cosmetics, and pharmaceuticals is driving market growth. Sucrose esters act as gentle surfactants, stabilizers, and solubilizers in creams, lotions, and drug delivery systems, supporting the expansion of premium natural product formulations.

What are the restraints for the global market?

High Production and Raw Material Costs

The cost of raw sugar and high-purity fatty acids directly impacts the production cost of sucrose esters. Price fluctuations in raw materials and specialized processing requirements can limit adoption, particularly in price-sensitive regions such as Latin America and parts of Asia.

Limited Awareness in Emerging Markets

In several emerging markets, knowledge of the functional benefits of sucrose esters remains limited. Companies must invest in education, technical support, and product demonstrations to increase penetration, which can slow market growth in the short term.

What are the key opportunities in the sucrose esters market?

Expansion into Industrial and Non-Food Applications

Beyond traditional food and cosmetic uses, sucrose esters offer opportunities in industrial applications such as eco-friendly lubricants, coatings, and biodegradable surfactants. Companies can target emerging industrial applications where environmental regulations favor biodegradable and non-toxic ingredients.

Regulatory Support and Clean-Label Growth

Global regulatory trends promoting natural, safe, and transparent ingredients create a favorable environment for sucrose esters. Food, cosmetic, and pharmaceutical manufacturers seeking compliance and market differentiation can adopt sucrose esters as preferred emulsifiers, enhancing brand value and consumer trust.

Technological Integration for Functional Customization

Advances in manufacturing technology allow customization of sucrose ester grades with specific functional properties. Companies investing in R&D can develop high-value, application-specific emulsifiers, increasing margins and market share.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 110 Million |

| Market Size in 2026 | USD 116.60 Million |

| Market Size in 2031 | USD 156.04 Million |

| CAGR | 6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Monoesters dominate the global sucrose esters market, accounting for approximately 40% of the 2025 market share, primarily due to their superior emulsification efficiency, higher hydrophilic-lipophilic balance (HLB), and strong compatibility with aqueous systems. Their dominance is driven by rising demand in beverage emulsions, low-fat dairy formulations, whipped toppings, and aerated bakery products where stability, foam enhancement, and fat reduction are critical performance parameters. Monoesters are particularly preferred in clean-label beverage emulsions as they enable uniform dispersion of flavor oils and vitamins while maintaining transparency and shelf stability. Increasing consumer demand for reduced-fat and functional food products continues to accelerate monoester consumption globally.

Diesters and triesters collectively account for nearly 35% of the market and are gaining traction in bakery, confectionery, and specialty food applications where controlled crystallization, improved texture, and extended shelf life are required. These grades offer better fat structuring and stabilization in complex lipid systems. Mixed esters, representing roughly 25% of the market, are widely used in cosmetics and pharmaceuticals due to their multifunctional properties, including solubilization, dispersion, and mild surfactant behavior. Growth in premium skincare and advanced drug delivery systems is strengthening demand for these higher-value ester blends.

Application Insights

Food & beverage remains the largest application segment, representing approximately 50% of the global market in 2025. The leading driver for this segment is the rapid expansion of processed and convenience food industries worldwide, coupled with the global shift toward clean-label emulsifiers. Sucrose esters are extensively used in bakery, confectionery, dairy alternatives, beverages, and frozen desserts for emulsification, aeration, texture enhancement, and shelf-life extension. Growing demand for plant-based and low-fat formulations further strengthens their adoption.

Personal care and cosmetics account for nearly 25a % of the market and represent the fastest-growing segment, with CAGR exceeding 7%. The primary driver here is the increasing consumer preference for bio-based, non-irritating surfactants in skincare, haircare, and cosmetic emulsions. Sucrose esters provide mildness, biodegradability, and enhanced product stability, making them highly attractive for natural and organic cosmetic brands. Pharmaceuticals, animal feed, and industrial applications collectively contribute around 25% of global demand. In pharmaceuticals, sucrose esters improve solubility and bioavailability in oral and topical drug formulations. Industrial uses, including biodegradable lubricants and coatings, are emerging growth niches driven by tightening environmental regulations and sustainability goals.

Distribution Channel Insights

The sucrose esters market operates primarily through B2B direct supply agreements, with manufacturers supplying directly to multinational food processors, cosmetic formulators, and pharmaceutical companies. Long-term supply contracts and customized formulation support are critical competitive differentiators. Major buyers prefer technical collaboration and quality assurance partnerships, particularly in regulated industries such as food and pharmaceuticals.

Specialty chemical distributors and regional ingredient suppliers account for a significant secondary distribution share, particularly in emerging markets where local warehousing and technical sales support are essential. Meanwhile, digital B2B marketplaces and ingredient e-commerce platforms are gradually expanding access for SMEs and startup cosmetic brands. Although online sales represent a smaller share today, they are growing steadily as procurement digitization increases across industries.

Explore more data points, trends and opportunities Download Free Sample Report

Sucrose Esters Market Segmentations

By Product Type

- Monoesters

- Diesters

- Triesters

- Mixed Esters

By Application

- Food & Beverage

- Personal Care & Cosmetics

- Pharmaceuticals

- Animal Feed

- Industrial Applications

By Form

- Powder

- Liquid

- Pellet/Solid

By Distribution Channel

- Direct B2B Supply

- Specialty Chemical Distributors

- Ingredient Marketplaces & E-Commerce Platforms

- Regional Warehousing & Contract Supply Agreements

Regional Insights

North America

North America accounts for approximately 25% of global sucrose esters consumption, with the United States representing the largest share, followed by Canada. Regional growth (CAGR 5.5%) is driven by strong demand for clean-label food additives, the rising plant-based product innovation, and the advanced cosmetic manufacturing industries. Strict FDA labeling standards and consumer scrutiny of synthetic emulsifiers have accelerated the adoption of bio-based alternatives. Additionally, the presence of multinational food and personal care companies with high R&D expenditure supports continuous product innovation and premium-grade ester consumption. Pharmaceutical advancements in drug solubility enhancement further contribute to stable demand growth.

Europe

Europe represents the largest regional market with approximately 30% share, led by Germany, France, the United Kingdom, and Italy. Growth (CAGR 6%) is strongly supported by stringent EU regulations promoting natural, biodegradable additives and restricting certain synthetic surfactants. The region’s mature processed food sector and strong organic cosmetic industry create sustained demand. High consumer awareness of ingredient transparency, combined with sustainability-focused policies under EU Green Deal initiatives, further drives sucrose ester adoption. Europe is also a major exporter of specialty sucrose esters to emerging markets, reinforcing its leadership position.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, accounting for approximately 28% of global demand in 2025. China and India are key growth engines due to rapid urbanization, rising disposable income, and expanding processed food and personal care industries. Japan and Australia represent mature, high-value markets with strong adoption in premium cosmetics and functional foods. Growth drivers include increasing domestic manufacturing capacity, rising imports of specialty ingredients, and growing awareness of clean-label formulations. Government initiatives supporting food processing industries in India and industrial modernization in China further accelerate demand.

Latin America

Latin America accounts for roughly 7% of global demand, led by Brazil, Mexico, and Argentina. The region is witnessing moderate growth driven by the expansion of processed food manufacturing and rising domestic cosmetic production. Increasing foreign direct investment in food processing facilities and improving retail infrastructure are strengthening ingredient demand. However, price sensitivity and limited local production capacity result in higher reliance on imports from Europe and North America.

Middle East & Africa

The Middle East & Africa region holds approximately 10% of global demand, led by the UAE, Saudi Arabia, and South Africa. Growth (CAGR 6%) is driven by expanding food processing sectors, rising premium cosmetic consumption, and strong import dependency on high-grade specialty ingredients. In Gulf Cooperation Council (GCC) countries, high disposable income and growing demand for premium skincare products support cosmetic applications. Meanwhile, South Africa serves as a regional manufacturing and distribution hub. Increasing government initiatives aimed at food security and domestic food manufacturing are further stimulating regional demand.

Key Players in the Sucrose Esters Market

- DuPont de Nemours, Inc.

- ICI Chemicals (UK) Ltd.

- Danisco (part of DuPont)

- Jungbunzlauer Suisse AG

- Amerchol Corporation

- ADM (Archer Daniels Midland Company)

- Kerry Group

- CEPSA Química, S.A.

- Yingkou Baohua Chemical Co., Ltd.

- Shandong Huatai Sugar Industry Co., Ltd.

- Seppic (France)

- Wego Chemical Group

- Biesterfeld AG

- Oleon NV

- Solvay S.A.