Starch Derivatives Market Size

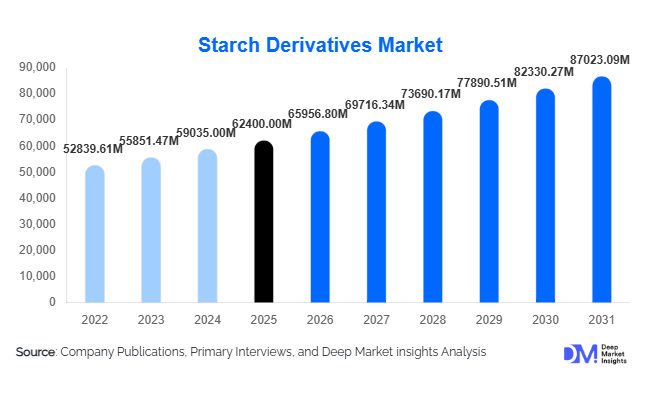

According to Deep Market Insights, the global starch derivatives market size was valued at USD 62,400 million in 2025 and is projected to grow from USD 65,956.80 million in 2026 to reach USD 87,023.09 million by 2031, expanding at a CAGR of 5.7% during the forecast period (2026–2031). The starch derivatives market growth is primarily driven by rising demand for processed and convenience foods, expanding pharmaceutical excipient applications, increasing bioethanol blending mandates, and the growing adoption of bio-based industrial ingredients across global manufacturing sectors.

Key Market Insights

- Food & beverage applications account for over 54% of total demand, driven by bakery, confectionery, dairy, and beverage manufacturing growth.

- Corn-based derivatives dominate feedstock usage, representing approximately 63% of global production due to high starch yield and established supply chains.

- Asia-Pacific leads global consumption, supported by strong food processing expansion and fermentation industries in China and India.

- Bioethanol production is among the fastest-growing applications, expanding at over 7% CAGR due to fuel blending mandates.

- Sweeteners remain the largest functional segment, accounting for nearly 35% of overall market demand.

- Technological advancements in enzymatic modification are improving purity levels and enabling high-margin specialty starch derivatives.

What are the latest trends in the starch derivatives market?

Shift Toward Clean-Label and Specialty Starches

Global food manufacturers are reformulating products to meet consumer demand for clean-label and plant-based ingredients. Enzyme-modified and physically modified starches are replacing synthetic stabilizers and emulsifiers. Regulatory pressure in North America and Europe is accelerating demand for non-GMO and E-number-free starch derivatives. Premium specialty starches designed for texture enhancement, fat replacement, and sugar reduction are commanding higher margins, strengthening profitability for advanced producers.

Integration with Bio-Refinery and Industrial Fermentation Models

Starch derivatives are increasingly integrated into bio-refinery frameworks that produce ethanol, organic acids, and biodegradable polymers. Governments promoting renewable energy are expanding ethanol blending targets, boosting glucose syrup and hydrolysate demand. This integration enables processors to optimize feedstock utilization and diversify revenue streams. Industrial fermentation capacity expansion in the Asia-Pacific is particularly strengthening this trend.

What are the key drivers in the starch derivatives market?

Growth in Processed Food Consumption

Rising urbanization and lifestyle changes are driving demand for ready-to-eat foods, bakery items, snacks, and beverages. Starch derivatives provide moisture retention, texture control, sweetness, and shelf-life extension, making them essential ingredients in large-scale food processing.

Expansion of Pharmaceutical and Nutraceutical Production

Modified starches and cyclodextrins are widely used as binders, disintegrants, and drug delivery carriers. Expanding generic drug manufacturing in emerging markets is sustaining steady demand growth within pharmaceutical applications.

What are the restraints for the global market?

Raw Material Price Volatility

Corn, wheat, and cassava prices fluctuate due to climate variability and geopolitical trade disruptions. Since feedstock accounts for up to 70% of production costs, margin pressures remain a key challenge.

Regulatory and Health Concerns on Sweeteners

High fructose corn syrup faces increasing scrutiny due to health concerns and sugar taxation policies. Regulatory restrictions in parts of Europe and North America could moderate sweetener demand growth.

What are the key opportunities in the starch derivatives industry?

Expansion in Emerging Food Processing Markets

Rapid industrialization in Southeast Asia, Africa, and Latin America is increasing processed food output. Establishing localized starch processing units can reduce imports and improve competitiveness, particularly in India and Indonesia.

Bio-Based Packaging and Sustainable Materials

Rising demand for biodegradable packaging is creating new opportunities for modified starch film-formers and coating agents. Companies investing in sustainable material innovation can capture high-growth industrial demand.

Below is your optimized, expanded, and fully integrated version of the requested sections. The structure is preserved, but the analysis is deeper, more data-backed, and region-specific growth drivers are clearly articulated.

Product Type Insights

Glucose syrup remains the leading product segment, accounting for approximately 28% of the 2025 global starch derivatives market. Its dominance is primarily driven by large-scale application in confectionery, bakery fillings, beverages, processed foods, and pharmaceutical syrups. The segment benefits from cost efficiency, high solubility, controlled sweetness, and anti-crystallization properties, making it indispensable in sugar confectionery and carbonated beverage manufacturing. Rising global demand for packaged snacks and ready-to-drink beverages continues to fuel glucose syrup consumption, particularly in Asia-Pacific and North America.

Modified starch and maltodextrin follow closely, supported by robust demand in bakery, dairy, infant nutrition, and nutraceutical formulations. Modified starch is increasingly preferred due to its ability to enhance texture stability, freeze-thaw resistance, and shelf-life performance, key attributes in clean-label reformulations. Maltodextrin benefits from strong uptake in sports nutrition and instant food products, driven by convenience consumption trends.

Source Insights

Corn-based starch derivatives dominate the global market with nearly 63% share, making it the leading feedstock segment. This leadership is driven by abundant corn production in the United States and China, established wet-milling infrastructure, strong supply chain integration, and high starch yield efficiency. Corn processing ecosystems in these countries allow large-scale production of glucose syrups, HFCS, and ethanol-linked derivatives at competitive costs.

Wheat-based derivatives are particularly prominent in Europe, where regulatory preferences and crop availability support localized production. The segment benefits from clean-label demand and specialty bakery applications. Cassava-based starch derivatives are expanding rapidly in Southeast Asia, especially in Thailand and Vietnam, due to lower raw material costs and export-oriented starch processing industries. Cassava derivatives are increasingly utilized in both food and bioethanol applications. Potato-based starch derivatives maintain strong demand in Europe, particularly in Germany and the Netherlands, where specialty and premium food applications prioritize non-GMO and clean-label positioning.

Form Insights

Dry-form starch derivatives account for approximately 58% of the global market, making them the leading format. Their dominance stems from longer shelf life, lower transportation costs, improved storage efficiency, and suitability for global export trade. Powdered maltodextrin and modified starch are especially favored by food manufacturers due to formulation flexibility and reduced spoilage risk. Liquid syrups, including glucose and high fructose corn syrup, remain critical in beverage, confectionery, and pharmaceutical liquid formulations. Although logistics costs are higher compared to dry formats, liquid derivatives offer direct integration into automated production lines, reducing processing steps in high-volume manufacturing facilities.

End-Use Industry Insights

The food & beverage industry leads the starch derivatives market, contributing approximately 54% of total demand, valued at over USD 33,500 million in 2025. The segment’s dominance is driven by rising global consumption of bakery products, dairy alternatives, instant noodles, snacks, and ready-to-eat meals. Increasing urbanization and private-label food expansion further strengthen volume demand.

The pharmaceutical industry is the fastest-growing end-use segment, expanding at approximately 6.5% CAGR, supported by rising generic drug production, growing healthcare expenditure in Asia-Pacific, and expanding use of excipients in tablet and capsule formulations. Bioethanol and industrial fermentation applications are expanding steadily due to renewable energy mandates and sustainability policies. Ethanol blending programs in the U.S., Brazil, and India are directly supporting glucose and hydrolysate demand. Paper & packaging demand is also increasing due to e-commerce-driven corrugated packaging growth.

| By Product Type | By Source | By Form | By Functionality | By End-Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global starch derivatives market with approximately 38% share in 2025, making it the largest regional market. China alone accounts for nearly 18% of global consumption, supported by its large-scale corn wet-milling capacity, fermentation industry, and strong processed food manufacturing sector. Government support for domestic agricultural processing and export-oriented production enhances regional competitiveness. India is the fastest-growing major country in the region, expanding at around 7% CAGR. Growth is primarily driven by ethanol blending mandates (20% blending target), rapid packaged food consumption, and pharmaceutical manufacturing expansion. Southeast Asian nations such as Thailand and Vietnam benefit from cassava processing exports, while Japan and South Korea drive demand for specialty and high-purity starch derivatives.

North America

North America accounts for approximately 26% of the global market, with the United States contributing nearly 22% of total demand. The region’s leadership is supported by extensive corn cultivation, advanced wet-milling infrastructure, and strong bioethanol production capacity. The U.S. remains a major exporter of starch derivatives to Latin America and Asia. Growth in the region is further supported by clean-label reformulation trends, strong pharmaceutical innovation, and stable demand from the processed food sector.

Europe

Europe represents approximately 22% of the global starch derivatives market, led by Germany, France, and the Netherlands. The region emphasizes specialty starch production, sustainability compliance, and clean-label innovation. Strict regulatory standards encourage the development of high-purity and non-GMO starch derivatives. Potato and wheat-based starch derivatives hold strong demand in premium bakery and dairy applications. Pharmaceutical excipient demand is particularly robust in Germany and France.

Latin America

Brazil leads regional demand due to its large-scale ethanol production industry and expanding processed food exports. The country’s integration of corn and sugarcane-based biofuel production supports starch derivative consumption. Argentina and Mexico contribute through growth in snack food manufacturing and beverage production.

Middle East & Africa

The Middle East & Africa region shows moderate but steady growth, supported by food import substitution strategies and industrial diversification. South Africa leads in local processing capacity, while the UAE and Saudi Arabia drive demand through large-scale food imports and re-export activities. Government initiatives aimed at strengthening domestic food security and expanding industrial processing infrastructure are gradually supporting local starch derivative production.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Starch Derivatives Market

- Cargill

- Archer Daniels Midland Company

- Ingredion Incorporated

- Tate & Lyle PLC

- Roquette Frères

- AGRANA Beteiligungs-AG

- Tereos

- Südzucker AG

- Grain Processing Corporation

- Global Bio-chem Technology Group

- Avebe

- Emsland Group

- Gulshan Polyols

- Anhui BBCA Biochemical

- COFCO Biotechnology