Soy Protein Market Size

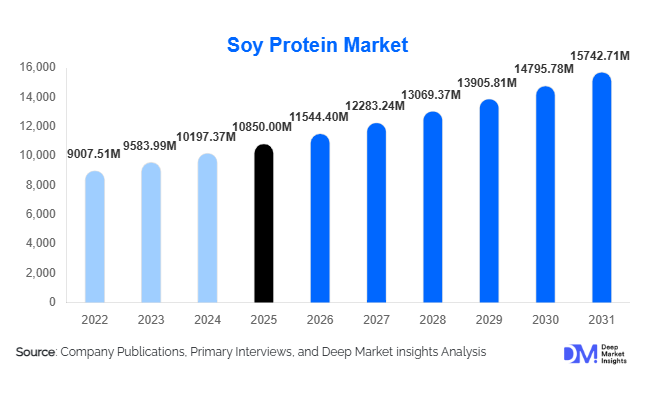

According to Deep Market Insights, the global soy protein market size was valued at USD 10,850 million in 2025 and is projected to grow from USD 11,544.40 million in 2026 to reach USD 15,742.71 million by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The soy protein market growth is primarily driven by the accelerating shift toward plant-based diets, increasing demand for high-protein functional foods, and expanding utilization in animal feed and industrial applications.

Soy protein remains one of the most commercially scalable plant proteins due to its complete amino acid profile, cost competitiveness, and established global soybean supply chains. Rapid expansion of meat alternatives, dairy substitutes, sports nutrition, and aquaculture feed formulations continues to strengthen global demand. Additionally, improvements in processing technologies have enhanced taste neutrality, solubility, and texturization, enabling broader application across mainstream food categories. With strong adoption across North America and Asia-Pacific and growing premium demand for non-GMO and organic variants in Europe, the market outlook remains structurally positive.

Key Market Insights

- Soy protein isolates account for approximately 38% of total market revenue, driven by high-protein content and strong demand in meat alternatives and beverages.

- Food & beverages represent nearly 52% of total consumption, led by plant-based meat and dairy substitute applications.

- Asia-Pacific dominates with around 36% market share, supported by large-scale feed demand and growing plant-based food adoption.

- North America holds approximately 32% share, driven by innovation in alternative proteins and sports nutrition.

- Conventional soy protein accounts for nearly 70% of the supply, reflecting industrial-scale procurement and cost efficiency.

- The top five players control roughly 42–45% of the global market, indicating moderate consolidation.

What are the latest trends in the soy protein market?

Premiumization Through Non-GMO and Organic Certification

Demand for identity-preserved, non-GMO, and organic soy protein is expanding, particularly across Europe and premium North American food segments. Consumers increasingly prioritize clean-label and traceable ingredient sourcing, prompting manufacturers to invest in segregated supply chains and certification compliance. Non-GMO soy protein variants typically command price premiums of 10–20%, strengthening margins for specialized producers. Retailers and food brands are also promoting sustainability-linked labeling, reinforcing consumer trust and boosting higher-value segment growth.

Technological Advancements in Texturization and Flavor Optimization

Modern extrusion and enzymatic processing technologies are improving the texture and taste profile of soy protein, especially in meat analog applications. High-moisture extrusion enables fibrous structures closely resembling animal meat, expanding adoption among mainstream consumers. Additionally, innovations in deodorization and hydrolysis are reducing beany flavors, making soy protein more suitable for beverages and clinical nutrition products. These technological upgrades are enhancing product versatility and accelerating penetration across high-growth food categories.

What are the key drivers in the soy protein market?

Expansion of Plant-Based Food Ecosystems

The rapid rise of flexitarian and vegan dietary patterns globally is significantly boosting soy protein demand. Soy protein isolates and textured soy protein are widely used in burgers, sausages, nuggets, and dairy-free beverages. Growing retail shelf space and foodservice adoption are expanding consumer access, strengthening long-term growth prospects.

Strong Demand from the Animal Feed Industry

The global poultry, swine, and aquaculture industries continue to expand, particularly in China, India, and Southeast Asia. Soy protein concentrates provide high digestibility and balanced amino acids, making them essential components of feed formulations. Feed demand provides a stable baseline consumption even during economic fluctuations.

What are the restraints for the global market?

GMO Perception and Regulatory Scrutiny

Consumer skepticism toward genetically modified crops remains a key challenge, particularly in Europe. Strict labeling regulations and compliance costs can restrict the adoption of conventional soy protein in premium food applications.

Raw Material Price Volatility

Soy protein pricing is closely linked to soybean commodity markets, which experience 8–12% annual volatility due to weather conditions, geopolitical trade shifts, and export policies. This impacts production margins and procurement planning for manufacturers.

What are the key opportunities in the soy protein industry?

Clinical and Sports Nutrition Expansion

The growing elderly population and rising health awareness are increasing demand for high-protein dietary supplements and ready-to-drink beverages. Hydrolyzed soy protein peptides offer improved absorption, creating opportunities in medical nutrition and performance sports segments.

Industrial and Biodegradable Applications

Soy protein is gaining traction in bio-based adhesives, paper coatings, and biodegradable plastics. As governments promote sustainable materials, soy-derived industrial ingredients present a diversification opportunity beyond food and feed markets.

Product Type Insights

Soy protein isolates (SPI) dominate the global market with approximately 38% revenue share in 2025, maintaining leadership due to their high protein concentration (>90%), neutral taste profile, and superior functional properties such as emulsification, gelation, and water-binding capacity. The primary growth driver for isolates is their extensive adoption in plant-based meat and dairy alternatives, where manufacturers require high-purity protein with strong texturization capability. Technological advancements in high-moisture extrusion and enzyme-assisted processing have further enhanced SPI’s structural performance in meat analog applications, reinforcing its premium positioning. Additionally, isolates are widely used in ready-to-drink beverages and clinical nutrition, where solubility and digestibility are critical.

Textured soy protein (TSP) holds the second-largest share, supported directly by the rapid expansion of meat analog production globally. TSP’s fibrous structure and cost efficiency make it the preferred base material for burgers, sausages, nuggets, and plant-based ready meals. Its growth trajectory closely mirrors the expansion of flexitarian diets and foodservice adoption of alternative proteins. Soy protein concentrates (SPC) remain heavily utilized in animal feed, particularly poultry and aquaculture, where digestibility and amino acid balance drive procurement decisions. Meanwhile, soy flour and grits continue serving the bakery, confectionery, and processed food segments as cost-effective protein enrichment solutions. Ongoing R&D investments in extrusion and flavor optimization technologies are expected to further strengthen isolate and textured protein dominance over the forecast period.

Application Insights

Meat substitution and analog structuring represent the fastest-growing application, accounting for nearly 28% of total market revenue in 2025. The primary driver is rising global demand for plant-based meat alternatives, supported by environmental sustainability concerns, animal welfare awareness, and food innovation. High-moisture extrusion techniques have enabled soy protein to closely replicate muscle fiber textures, making it highly suitable for mainstream consumer products. Protein fortification in snacks, beverages, cereals, and bakery items is expanding steadily, driven by increasing health consciousness and demand for high-protein diets. Manufacturers are incorporating soy protein into everyday packaged foods to improve nutritional claims without significantly altering taste or texture.

Emulsification and fat replacement remain critical functional uses in processed foods, particularly in sausages, sauces, and ready-to-eat meals, where soy protein enhances stability and shelf life. Nutritional supplementation, including sports nutrition powders and elderly nutrition formulas, continues gaining traction as aging populations and fitness trends accelerate demand for high-quality plant proteins.

End-Use Industry Insights

The food & beverages segment leads the market with approximately 52% share in 2025, valued at over USD 5,600 million and growing at nearly 7% CAGR. The segment’s growth is primarily driven by plant-based meat alternatives, dairy substitutes, functional beverages, and fortified packaged foods. Rising consumer preference for clean-label and sustainable protein sources continues to accelerate soy protein penetration in this sector. Animal feed represents the second-largest end-use segment, underpinned by global poultry and aquaculture expansion. Rapid urbanization and rising protein consumption in the Asia-Pacific region are driving feed demand, ensuring stable baseline consumption of soy protein concentrates.

Personal care and cosmetics remain niche but are steadily expanding, as soy peptides are increasingly incorporated into anti-aging and hair-care formulations. Industrial applications, including adhesives, paper coatings, and biodegradable plastics, are emerging growth pockets. Additionally, new applications such as plant-based seafood analogs and fortified infant formulas are creating incremental and high-margin demand streams.

| By Product Type | By Application | By End-Use Industry | By Nature | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 32% of global revenue, led predominantly by the United States. Regional growth is driven by strong consumer adoption of plant-based diets, a highly developed sports nutrition industry, and robust innovation ecosystems. The presence of advanced soybean processing infrastructure and vertically integrated agribusiness firms ensures supply chain efficiency and competitive pricing. Regulatory clarity and strong retail distribution networks further support the rapid commercialization of soy protein-based food products.

Asia-Pacific

Asia-Pacific holds the largest share at around 36% of global revenue. China dominates regional demand due to large-scale soybean processing and extensive use of soy protein in animal feed. Rising meat consumption continues to boost feed-grade soy protein procurement. Japan and South Korea lead functional food and clinical nutrition adoption, supported by aging populations. India is the fastest-growing country in the region, expanding at nearly 8% CAGR, driven by vegetarian dietary traditions, growing middle-class incomes, and expansion of processed food manufacturing. Increasing investments in domestic protein processing facilities further accelerate regional growth.

Europe

Europe contributes roughly 22% of global revenue, with Germany, France, and the Netherlands serving as key markets. Growth is primarily driven by high consumer demand for non-GMO and sustainably sourced proteins. Strict labeling regulations and environmental policies promote plant-based protein alternatives, accelerating soy protein adoption in meat substitutes and dairy alternatives. The region also benefits from strong retail penetration of private-label plant-based products and government-backed sustainability initiatives.

Latin America

Latin America, led by Brazil and Argentina, plays a dual role as both a major producer and exporter of soy protein. Abundant soybean cultivation, favorable climate conditions, and export-oriented agribusiness infrastructure drive production capacity. Domestic demand is expanding alongside the livestock and processed food industries. Government incentives supporting agricultural exports and investments in crushing and processing facilities strengthen the region’s competitive position in global trade.

Middle East & Africa

The Middle East & Africa region represents an emerging market with growing import dependency for soy protein products. Rising poultry feed demand in Saudi Arabia, the UAE, and South Africa is a key growth driver. Urbanization, expanding food processing industries, and increasing consumer awareness of plant-based nutrition are gradually supporting food-grade soy protein adoption. Strategic trade partnerships and investments in feed manufacturing capacity are expected to enhance regional demand over the forecast period.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Soy Protein Market

- Archer Daniels Midland Company

- Cargill Incorporated

- International Flavors & Fragrances Inc.

- CHS Inc.

- Bunge Limited

- Wilmar International Ltd.

- Fuji Oil Holdings Inc.

- Shandong Yuwang Industrial Co., Ltd.

- Gushen Biological Technology Group Co., Ltd.

- DuPont de Nemours Inc.

- The Scoular Company

- Victoria Group

- Devansoy Inc.

- Shandong Sinoglory Health Food Co., Ltd.

- Solae LLC