Shoe Care Products Market Size

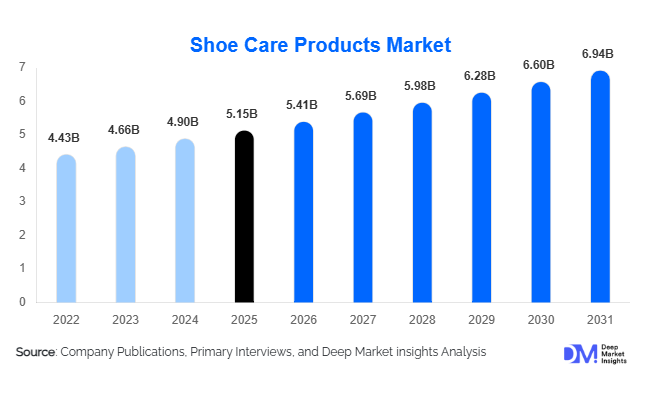

According to Deep Market Insights, the global shoe care products market size was valued at USD 5.15 billion in 2025 and is projected to grow from USD 5.41 billion in 2026 to reach USD 6.94 billion by 2031, expanding at a CAGR of 5.1% during the forecast period (2026–2031). The shoe care products market growth is primarily driven by increasing consumer awareness regarding footwear maintenance, the growing popularity of premium and luxury footwear, expansion of sneaker culture worldwide, and rising demand for specialized cleaning, conditioning, protection, and restoration solutions. As consumers increasingly view footwear as a long-term investment rather than a disposable product, demand for shoe care products continues to expand across both developed and emerging markets.

Key Market Insights

- Premium footwear ownership is increasing globally, driving higher spending on shoe maintenance products such as cleaners, conditioners, waterproofing sprays, and restoration kits.

- Sneaker culture continues to transform the market, with collectible and limited-edition footwear creating strong demand for specialized cleaning and protective products.

- North America dominates the global market, accounting for nearly 32% of total revenue in 2025 due to high consumer spending and established shoe care habits.

- Asia-Pacific is the fastest-growing regional market, supported by rising footwear consumption, urbanization, and expanding middle-class populations.

- E-commerce channels are rapidly gaining market share, enabling direct-to-consumer brands and niche premium manufacturers to expand their global reach.

- Sustainability is becoming a key purchasing criterion, with consumers increasingly preferring eco-friendly formulations, biodegradable ingredients, and recyclable packaging.

Shoe Care Products Market Trends

Rise of Premium Sneaker Care and Restoration Solutions

The growing global sneaker ecosystem is reshaping the shoe care products market. Consumers increasingly purchase limited-edition sneakers and luxury athletic footwear, many of which command significant resale value. As a result, specialized sneaker cleaning kits, stain-resistant coatings, sole whitening products, and restoration solutions are experiencing strong demand. Professional sneaker restoration services are also expanding globally, creating opportunities for manufacturers to develop premium-grade maintenance products. Social media platforms, sneaker influencers, and resale marketplaces continue to educate consumers on footwear preservation, further supporting product adoption. This trend is particularly prominent in North America, China, Japan, South Korea, and Western Europe, where sneaker collecting has evolved into a mainstream lifestyle category.

Sustainable Shoe Care Formulations Gaining Market Acceptance

Environmental sustainability is emerging as a major trend within the shoe care products industry. Manufacturers are increasingly replacing petroleum-derived ingredients with plant-based waxes, biodegradable surfactants, and low-VOC formulations. Consumers are showing a stronger preference for environmentally responsible products that minimize chemical exposure while delivering comparable performance. Companies are also investing in refillable packaging, recycled plastic containers, and carbon-neutral manufacturing practices. Regulatory pressures in Europe and North America regarding chemical content and packaging waste are accelerating innovation in sustainable product development. Eco-conscious brands are leveraging sustainability as a key differentiator, enabling premium pricing and stronger consumer loyalty.

Shoe Care Products Market Drivers

Growing Global Premium Footwear Industry

The continued expansion of premium, luxury, and branded footwear markets is a significant growth driver for shoe care products. Consumers purchasing higher-value footwear increasingly seek maintenance solutions that preserve appearance, durability, and resale value. Premium leather shoes, designer footwear, luxury sneakers, and handcrafted footwear require regular cleaning, conditioning, and protection, generating recurring demand for specialized shoe care products. Rising disposable incomes across Asia-Pacific and the Middle East are further contributing to premium footwear adoption and associated maintenance spending.

Expansion of E-Commerce and Direct-to-Consumer Sales

Digital commerce has transformed product accessibility within the shoe care products market. Consumers can now access specialized products that were previously available only through niche retailers. Direct-to-consumer brands are utilizing social media marketing, influencer partnerships, and educational content to increase awareness and product adoption. Subscription-based shoe care kits and bundled maintenance products are also gaining popularity among repeat customers. E-commerce channels provide manufacturers with higher margins while enabling broader geographic penetration across emerging markets.

Shoe Care Products Market Restraints

Low Consumer Awareness in Developing Markets

Despite growing footwear consumption globally, many consumers in developing economies remain unfamiliar with specialized shoe care products. In several regions, footwear replacement remains more common than footwear maintenance, reducing product penetration. Limited awareness regarding long-term cost savings and footwear preservation benefits continues to restrict market growth, particularly in lower-income consumer segments.

Availability of Low-Cost Cleaning Alternatives

Consumers frequently substitute dedicated shoe care products with household cleaning agents, detergents, and improvised maintenance methods. These alternatives often provide short-term cost advantages, particularly in price-sensitive markets. The widespread availability of substitute products creates pricing pressure and limits premium product adoption, particularly in emerging economies where brand loyalty remains relatively low.

Shoe Care Products Market Opportunities

Growth of Sneaker Care Ecosystems

The global sneaker resale economy presents significant opportunities for shoe care product manufacturers. Collectible sneakers often command premium resale values, creating strong incentives for consumers to invest in maintenance and preservation products. Companies can capitalize on this trend through specialized sneaker cleaning systems, protective coatings, restoration products, and membership-based care programs. Collaborations with sneaker retailers, collectors, and online resale platforms are expected to create new revenue streams for market participants.

Expansion Across Emerging Economies

Countries such as India, Indonesia, Vietnam, Brazil, Saudi Arabia, and Mexico are experiencing rapid growth in footwear ownership and disposable income levels. As consumers increasingly purchase branded and premium footwear, demand for maintenance products is expected to rise significantly. Localized manufacturing, affordable product formats, and expanded retail distribution networks offer attractive growth opportunities for both established brands and new entrants. Government initiatives supporting domestic manufacturing also create favorable investment conditions across emerging regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.15 Billion |

| Market Size in 2026 | USD 5.41 Billion |

| Market Size in 2031 | USD 6.94 Billion |

| CAGR | 5.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Shoe polishes dominated the global shoe care products market, accounting for approximately 31% of total revenue in 2025. The segment maintains its leadership due to the large installed base of leather formal footwear worldwide and the recurring need for polishing to preserve appearance, extend product lifespan, and maintain material quality. Wax-based and cream-based polishes remain the preferred solutions among corporate professionals, hospitality workers, military personnel, educational institutions, and luxury footwear owners due to their ability to restore shine, enhance water resistance, and protect leather surfaces from premature deterioration. Demand is particularly strong across Europe, North America, and parts of Asia where leather footwear ownership remains high.

The segment also benefits from the premiumization of footwear, as consumers increasingly view high-quality shoes as long-term investments that require regular maintenance. While traditional polish products continue to generate the largest share of industry revenue, shoe cleaners represent the fastest-growing product category, driven by the rapid expansion of sneaker culture and athletic footwear ownership globally. Specialized sneaker cleaners, foam-based cleaning products, and multi-material cleaning solutions are witnessing strong adoption among younger consumers and collectors seeking to maintain the resale value of premium footwear. Additionally, waterproofing sprays, protective coatings, and conditioning products are gaining traction due to rising participation in outdoor activities and increasing consumer awareness regarding preventive footwear care.

Footwear Type Insights

Formal footwear accounted for approximately 38% of global shoe care product demand in 2025, making it the largest footwear segment. The dominance of this category is primarily driven by the ongoing requirement for maintenance of leather-based formal shoes across corporate workplaces, hospitality establishments, government institutions, educational organizations, and defense sectors. Formal footwear typically requires regular polishing, conditioning, and restoration to maintain professional appearance standards, resulting in higher recurring purchases of shoe care products compared to other footwear categories.

Growth in premium business footwear and luxury leather shoe ownership further reinforces demand within this segment. In developed economies, consumers often own multiple pairs of formal shoes, creating recurring maintenance requirements throughout the product lifecycle. Meanwhile, athletic and sports footwear is emerging as the fastest-growing footwear category, supported by growing participation in fitness activities, increasing sneaker ownership, and the expansion of the global sportswear industry. The rising popularity of collectible sneakers and premium athletic footwear is generating substantial demand for specialized cleaning kits, sole restoration products, and protective treatments. Luxury footwear also remains a high-value segment due to above-average spending on conditioning, restoration, and preservation products.

Material Compatibility Insights

Leather footwear care products represented approximately 46% of total market revenue in 2025 and continue to dominate the material compatibility segment. Leather remains one of the most maintenance-intensive footwear materials, requiring regular conditioning, polishing, waterproofing, and restoration to prevent cracking, discoloration, and material degradation. The large global installed base of leather formal shoes, luxury footwear, and premium boots creates consistent demand for leather-specific care solutions.

The segment benefits from growing consumer preference for premium and durable footwear, particularly in North America and Europe where leather footwear ownership remains significantly higher than the global average. Additionally, luxury footwear brands increasingly recommend dedicated maintenance products to preserve product quality and enhance longevity. While leather-specific products remain dominant, multi-material shoe care products are experiencing rapid growth due to increasing consumer demand for convenience-oriented solutions capable of cleaning and protecting leather, mesh, canvas, suede, synthetic, and rubber surfaces simultaneously. Rising casual footwear consumption is also supporting demand for textile and canvas-specific cleaning products, particularly among younger demographics.

Distribution Channel Insights

Offline retail channels accounted for approximately 75% of global shoe care product sales in 2025, maintaining their position as the leading distribution channel. Supermarkets, hypermarkets, department stores, and specialty footwear retailers continue to dominate sales due to their extensive geographic reach, strong consumer trust, and ability to facilitate impulse purchases alongside footwear sales. Consumers frequently purchase shoe care products while shopping for footwear, making physical retail stores an important point of sale for both premium and mass-market brands.

The segment is further supported by product demonstrations, personalized recommendations from store staff, and immediate product availability. However, e-commerce is the fastest-growing distribution channel, driven by increasing internet penetration, growing preference for online shopping, and the expansion of direct-to-consumer business models. Digital platforms provide access to specialized products, niche brands, customer reviews, and educational content that help consumers make informed purchasing decisions. Brand-owned websites are becoming increasingly important as manufacturers seek to improve profit margins, strengthen customer engagement, and offer customized product recommendations through data-driven marketing strategies.

End-User Insights

Residential consumers represented approximately 67% of total market demand in 2025, making them the largest end-user segment globally. The dominance of household consumers is driven by the widespread ownership of formal, casual, athletic, and luxury footwear requiring routine maintenance. Consumers regularly purchase shoe polishes, cleaners, conditioners, deodorizing sprays, waterproofing solutions, and maintenance accessories to preserve the appearance and durability of their footwear collections.

Growing awareness regarding footwear longevity, increasing ownership of premium shoes, and the rising influence of sneaker culture continue to strengthen residential demand. Additionally, social media platforms and footwear influencers have contributed significantly to consumer education regarding shoe maintenance practices. Although residential users account for the majority of market revenues, professional shoe care service providers represent the fastest-growing end-user segment. The rapid growth of sneaker restoration services, luxury shoe repair businesses, and specialty footwear maintenance providers is generating increased demand for professional-grade cleaning, conditioning, and restoration products. Commercial institutions, including hotels, corporate offices, defense organizations, and educational institutions, continue to provide stable demand due to workplace footwear maintenance requirements.

Explore more data points, trends and opportunities Download Free Sample Report

Shoe Care Products Market Segmentations

By Product Type

- Shoe Polishes

- Shoe Cleaners

- Conditioners & Restorers

- Protective Products

- Deodorizing Products

- Repair & Maintenance Products

- Shoe Care Accessories

By Footwear Type

- Formal Footwear

- Casual Footwear

- Athletic & Sports Footwear

- Luxury Footwear

- Work & Safety Footwear

- Outdoor & Hiking Footwear

- Children's Footwear

By Material Compatibility

- Leather Footwear Care Products

- Suede & Nubuck Care Products

- Synthetic Footwear Care Products

- Textile & Canvas Footwear Care Products

- Rubber & EVA Footwear Care Products

- Multi-Material Care Products

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Footwear Stores

- Department Stores

- Convenience Stores

- Brand-Owned Retail Stores

- E-Commerce Platforms

- Direct-to-Consumer (DTC) Websites

By End User

- Residential Consumers

- Professional Shoe Care Service Providers

- Commercial Institutions

- Footwear Manufacturers (B2B)

Regional Insights

North America

North America accounted for approximately 32% of global shoe care products market revenue in 2025, making it the largest regional market. The United States contributes nearly 26% of global demand, supported by high footwear ownership rates, strong consumer spending power, and one of the world's most developed sneaker cultures. The region has a well-established premium footwear market, with consumers demonstrating a strong willingness to invest in maintenance products that extend footwear lifespan and preserve resale value. Growing participation in sneaker collecting, expansion of premium athletic footwear sales, and increasing demand for specialized cleaning and restoration solutions continue to support market growth.

Additional growth drivers include mature retail infrastructure, strong e-commerce penetration, widespread availability of premium shoe care brands, and increasing consumer awareness regarding footwear preservation. Canada contributes significant demand through luxury footwear ownership and outdoor footwear applications, while sustainability-focused consumers across the region are driving adoption of environmentally friendly shoe care formulations.

Europe

Europe represented approximately 29% of global market revenue in 2025 and remains one of the most mature shoe care products markets worldwide. Germany, the United Kingdom, France, Italy, and Spain collectively account for the majority of regional demand. The region's long-standing tradition of leather footwear ownership and strong luxury fashion industry continue to support demand for premium shoe care products. Italy and France, in particular, benefit from their positions as major luxury footwear manufacturing hubs, where consumers place significant emphasis on footwear maintenance and preservation.

Regional growth is driven by increasing consumer preference for high-quality footwear, expanding luxury footwear sales, and growing adoption of sustainable consumer products. Stringent environmental regulations and rising demand for biodegradable formulations are encouraging manufacturers to develop eco-friendly shoe care solutions. Additionally, Europe benefits from high disposable incomes, established retail networks, and strong consumer awareness regarding footwear care practices.

Asia-Pacific

Asia-Pacific accounted for approximately 25% of global demand in 2025 and is projected to register the fastest growth rate through 2031. China remains the largest regional market, contributing approximately 10% of global consumption, while India represents one of the fastest-growing countries due to rising disposable incomes, rapid urbanization, and increasing footwear ownership. Japan and South Korea continue to drive premium demand through luxury footwear purchases and strong sneaker culture adoption.

The region's growth is supported by expanding middle-class populations, increasing penetration of international footwear brands, growing e-commerce adoption, and rising consumer awareness regarding footwear maintenance. Rapid growth in organized retail, increasing participation in sports and fitness activities, and expansion of domestic footwear manufacturing industries are further contributing to demand. Government-led manufacturing initiatives in countries such as India and China are also supporting broader development of footwear-related value chains, indirectly benefiting shoe care product consumption.

Latin America

Latin America accounted for approximately 8% of global market revenue in 2025. Brazil remains the dominant market due to its large footwear manufacturing industry, extensive domestic consumer base, and increasing ownership of branded footwear. Mexico, Argentina, and Chile are also contributing to regional demand growth through rising urbanization and improving consumer purchasing power.

Key growth drivers include increasing awareness regarding footwear maintenance, expansion of modern retail channels, and growing demand for affordable premium footwear. The emergence of middle-income consumers across major economies is encouraging higher spending on personal care and lifestyle products, including footwear maintenance solutions. Additionally, increasing penetration of international footwear brands is creating new opportunities for premium shoe care product adoption throughout the region.

Middle East & Africa

The Middle East & Africa region represented approximately 6% of global market revenue in 2025 and is expected to witness above-average growth during the forecast period. Saudi Arabia, the United Arab Emirates, and South Africa remain the primary demand centers, supported by rising luxury consumption, premium retail expansion, and growing urban populations. The UAE has emerged as a particularly attractive market due to its strong luxury footwear sector and high concentration of affluent consumers.

Regional growth is being driven by increasing disposable incomes, expansion of premium shopping destinations, rising international tourism, and growing demand for luxury fashion products. In addition, footwear consumption is increasing across several African economies as urbanization and middle-class development continue to accelerate. The expansion of organized retail networks and greater availability of international footwear brands are expected to create significant opportunities for shoe care product manufacturers across both the Middle East and Africa over the coming years.

Key Players in the Shoe Care Products Market

- S.C. Johnson & Son

- Implus Corporation

- Tarrago Brands International

- Angelus Brand

- Grangers International

- Cherry Blossom

- Salamander

- Jason Markk

- Cadillac Shoe Products

- Walter's Shoe Care

- Lexol

- Moneysworth & Best

- Penguin Brands

- Shinola

- Dasco