Protein Energy Drink Market Size

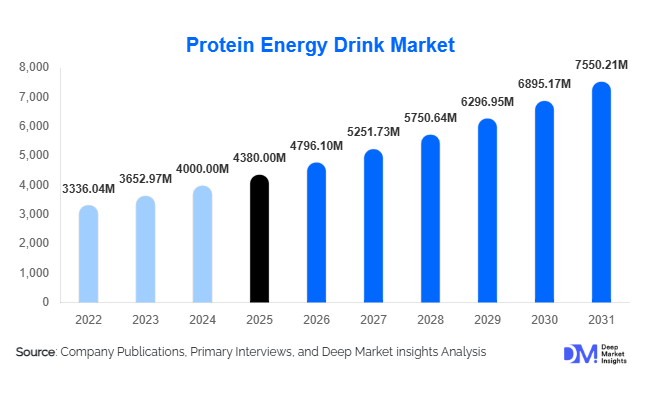

According to Deep Market Insights,the global protein energy drink market size was valued at USD 4,380 million in 2025 and is projected to grow from USD 4,796.10 million in 2026 to reach USD 7,550.21 million by 2031, expanding at a CAGR of 9.5% during the forecast period (2026–2031). The protein energy drink market growth is primarily driven by the rising adoption of high-protein diets, expanding fitness culture worldwide, and increasing demand for convenient, ready-to-drink (RTD) functional beverages that combine muscle recovery with sustained energy. The category has evolved beyond traditional sports nutrition to appeal to working professionals, students, and lifestyle consumers seeking healthier alternatives to sugar-laden energy drinks.

Key Market Insights

- RTD protein energy drinks dominate the category, accounting for over 70% of total market revenue due to portability and convenience.

- Whey protein-based formulations lead, representing nearly 48% of 2025 market share owing to superior bioavailability and strong consumer familiarity.

- North America holds approximately 38% of global demand, led by the United States with a 31% share of total market revenue.

- Asia-Pacific is the fastest-growing region, expanding at over 11% CAGR through 2031 driven by rising gym penetration and urbanization.

- Moderate-caffeine variants (80–150 mg per serving) account for around 46% of global sales, balancing performance with regulatory compliance.

- Online retail and DTC channels are expanding rapidly, supported by subscription models and influencer-driven marketing.

What are the latest trends in the protein energy drink market?

Plant-Based and Clean-Label Innovation

Manufacturers are increasingly investing in plant-based protein energy drinks using pea, rice, and soy protein blends. Consumers are demanding dairy-free, lactose-free, and non-GMO formulations, pushing brands to reformulate products with natural caffeine sources and zero added sugar. Clean-label positioning, including shorter ingredient lists and natural sweeteners, is enhancing premiumization and expanding the category beyond athletes to mainstream health-conscious consumers.

Functional Fortification and Hybridization

The market is witnessing rapid integration of additional functional ingredients such as electrolytes, collagen peptides, BCAAs, adaptogens, and nootropics. This hybridization is transforming protein energy drinks into multi-benefit beverages targeting cognitive focus, hydration, joint health, and metabolic support. Brands are positioning these products as all-day functional beverages rather than post-workout supplements, widening usage occasions and boosting repeat consumption.

What are the key drivers in the protein energy drink market?

Expansion of Global Fitness Culture

The rapid growth of gyms, boutique fitness studios, and amateur sports participation has significantly increased protein beverage consumption. Rising gym memberships in the U.S., Europe, China, and India have strengthened demand for convenient protein recovery solutions that also deliver energy. Social media fitness influencers and digital health platforms further accelerate product awareness and trial.

Shift Toward High-Protein Diets

Consumers increasingly associate protein intake with weight management, satiety, and metabolic health. Protein energy drinks provide an accessible alternative to protein powders, particularly for on-the-go lifestyles. Growing adoption of ketogenic, low-carb, and high-protein dietary patterns globally continues to stimulate category growth.

What are the restraints for the global market?

Premium Pricing and Cost Sensitivity

Protein energy drinks are priced significantly higher than conventional energy beverages due to expensive protein isolates and formulation costs. In emerging markets, price sensitivity restricts broader penetration, limiting adoption beyond affluent urban consumers.

Regulatory and Labeling Constraints

Stringent regulations regarding caffeine limits, protein claims, and nutritional labeling create compliance challenges across regions. Variations between U.S., European, and Asian regulatory frameworks increase operational complexity for global brands.

What are the key opportunities in the protein energy drink industry?

Emerging Market Expansion

Asia-Pacific and Latin America present significant untapped potential. Countries such as China, India, Brazil, and Indonesia are witnessing rising disposable incomes and increasing sports participation. Establishing localized production facilities and region-specific flavor profiles can accelerate market penetration.

Corporate Wellness and Subscription Models

Growing adoption of workplace wellness programs provides opportunities for bulk procurement and vending partnerships. Subscription-based direct-to-consumer models enable predictable revenue streams and improved brand loyalty.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4380 Million |

| Market Size in 2026 | USD 4796.10 Million |

| Market Size in 2031 | USD 7550.21 Million |

| CAGR | 9.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Formulation Insights

Ready-to-drink (RTD) protein energy beverages continue to dominate the global market, accounting for approximately 72% of total revenue in 2025. The leadership of RTD formulations is primarily driven by increasing consumer preference for convenience-oriented nutrition solutions that align with fast-paced urban lifestyles. Their extended shelf life, portability, and compatibility with established energy drink packaging formats such as cans and PET bottles enhance mass-market penetration across supermarkets, gyms, convenience stores, and vending machines. In addition, manufacturers benefit from scalable production technologies and strong brand positioning within the broader functional beverage category. While concentrated powder and liquid formats hold a comparatively smaller share, they maintain relevance among fitness enthusiasts and performance-driven consumers who prefer customizable protein intake levels and flexible serving sizes. The leading RTD segment continues to gain traction due to impulse purchasing behavior, expanding retail shelf space, and growing demand for on-the-go protein supplementation.

Protein Source Insights

Whey protein-based beverages lead the global protein energy drink market, accounting for nearly 48% of total market share in 2025. The segment’s dominance is supported by whey protein’s superior amino acid profile, high branched-chain amino acid (BCAA) concentration, rapid absorption rate, and strong clinical backing for muscle recovery and performance enhancement. Its long-standing acceptance among athletes and bodybuilders further reinforces consumer trust and brand familiarity. However, plant-based protein energy drinks represent the fastest-growing segment, fueled by rising veganism, lactose intolerance concerns, and broader consumer interest in sustainable and allergen-free nutrition. Pea, soy, and blended plant proteins are increasingly incorporated into formulations to improve texture and amino acid completeness. Meanwhile, collagen-based protein variants are gaining momentum within beauty-from-within and holistic wellness sub-segments, appealing particularly to consumers focused on skin health, joint support, and anti-aging benefits.

Caffeine Content Insights

Moderate-caffeine formulations containing 80–150 mg per serving account for approximately 46% of global market share in 2025, making them the leading segment. Growth in this category is driven by mainstream consumers seeking balanced energy enhancement without excessive stimulation or adverse side effects. These products effectively bridge the gap between traditional energy drinks and coffee alternatives, making them suitable for daily consumption across professional and student populations. High-caffeine variants continue to perform strongly among athletes, gamers, and high-intensity lifestyle consumers who demand heightened alertness and endurance support. Conversely, low- or zero-caffeine formulations are gaining traction among caffeine-sensitive individuals and evening consumers, reflecting broader market diversification and product personalization trends.

Distribution Channel Insights

Supermarkets and hypermarkets represent approximately 38% of global sales in 2025, maintaining leadership due to strong shelf visibility, high foot traffic, and impulse-driven purchasing behavior. The leading position of this channel is supported by established supply chain networks, promotional discounting strategies, and integrated placement within functional beverage aisles. Convenience stores and specialty nutrition outlets also contribute significantly, particularly in urban markets. Online retail is the fastest-growing distribution channel, driven by subscription-based delivery models, direct-to-consumer brand strategies, influencer marketing campaigns, and expanding e-commerce penetration across emerging economies. Digital platforms enable detailed product comparisons, targeted advertising, and personalized recommendations, strengthening long-term customer retention.

Consumer Demographic Insights

Fitness enthusiasts and bodybuilding consumers contribute nearly 41% of total market demand, maintaining segment leadership due to strong alignment with protein-centric positioning and performance-oriented marketing strategies. This segment benefits from gym partnerships, sports sponsorships, and scientifically backed product claims emphasizing muscle recovery and endurance. However, working professionals and students represent the fastest-growing demographic group, increasingly adopting protein energy beverages as convenient meal supplements and productivity enhancers. Rising work pressure, extended study hours, and growing awareness of balanced macronutrient intake are supporting this shift. Additionally, female consumers are emerging as an important sub-segment, particularly for plant-based and collagen-infused formulations targeting wellness and aesthetic benefits.

Explore more data points, trends and opportunities Download Free Sample Report

Protein Energy Drink Market Segmentations

By Product Formulation

- Ready-to-Drink (RTD) Protein Energy Drinks

- Powdered Protein Energy Mixes

- Liquid Concentrates & Shots

By Protein Source

- Whey Protein-Based

- Casein Protein-Based

- Plant-Based Protein (Soy, Pea, Rice, Blends)

- Collagen Protein-Based

By Caffeine Content

- High-Caffeine (Above 150 mg)

- Moderate-Caffeine (80–150 mg)

- Low/No-Caffeine

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & Direct-to-Consumer

- Specialty Nutrition Stores

- Foodservice & Gyms

By Consumer Demographic

- Fitness & Bodybuilding Consumers

- Lifestyle & Functional Beverage Consumers

- Working Professionals & Students

- Professional & Amateur Athletes

Regional Insights

North America

North America accounts for approximately 38% of the global protein energy drink market in 2025, maintaining its leadership position due to advanced sports nutrition infrastructure, high per capita health expenditure, and strong brand penetration. The United States alone contributes nearly 31% of global revenue, supported by a well-established fitness culture, widespread gym memberships, and early adoption of functional beverages. Innovation in clean-label, sugar-free, and performance-enhancing formulations further drives regional growth. Canada demonstrates steady expansion, fueled by increasing health awareness, rising disposable incomes, and growing demand for plant-based protein alternatives. Strong retail distribution networks and aggressive marketing by established brands continue to reinforce North America's dominant position.

Europe

Europe contributes close to 27% of global demand, led by the United Kingdom and Germany. Regional growth is driven by rising consumer focus on clean-label products, sugar reduction initiatives, and regulatory clarity surrounding functional ingredient claims. Western Europe represents a mature market characterized by premiumization trends, sustainable packaging innovations, and growing adoption of plant-based proteins. Meanwhile, Eastern Europe offers moderate growth potential due to improving retail infrastructure, rising disposable incomes, and expanding fitness participation rates. Increasing consumer awareness regarding protein supplementation for general wellness, rather than solely athletic performance, further supports steady regional expansion.

Asia-Pacific

Asia-Pacific holds approximately 22% of global revenue in 2025 and is projected to expand at a CAGR exceeding 11%, making it the fastest-growing regional market. Rapid urbanization, expanding middle-class populations, and increasing gym penetration in China and India serve as primary growth drivers. Rising youth demographics and social media-driven fitness trends significantly influence consumption patterns across metropolitan areas. Japan and Australia represent stable premium markets characterized by demand for high-quality, scientifically formulated products. Additionally, growing e-commerce adoption and cross-border brand availability are accelerating market accessibility throughout Southeast Asia.

Latin America

Latin America accounts for roughly 7% of the global market, with Brazil and Mexico leading regional consumption. Growth is primarily driven by expanding youth populations, increasing sports participation, and gradual improvement in health awareness levels. Urban retail expansion and rising penetration of international beverage brands contribute to market development. Although economic volatility presents short-term challenges, increasing demand for affordable RTD formulations and growing interest in fitness culture are expected to sustain moderate long-term growth across the region.

Middle East & Africa

The Middle East & Africa collectively represent approximately 6% of global revenue in 2025. The United Arab Emirates and South Africa serve as key regional hubs, supported by high-income consumer bases, expanding retail infrastructure, and strong demand for premium imported beverages. Growth in the Middle East is further stimulated by rising gym memberships, government-led health awareness initiatives, and increasing expatriate populations. In Africa, urbanization and improving modern trade penetration are gradually enhancing product accessibility. While the market remains in a developing stage, rising awareness of protein supplementation and energy beverages is expected to create incremental growth opportunities over the forecast period.

Key Players in the Protein Energy Drink Market

- PepsiCo, Inc.

- The Coca-Cola Company

- Monster Beverage Corporation

- Red Bull GmbH

- Abbott Laboratories

- Glanbia plc

- Nestlé S.A.

- Celsius Holdings, Inc.

- Vital Pharmaceuticals, Inc.

- Alani Nutrition LLC

- Otsuka Pharmaceutical Co., Ltd.

- BioSteel Sports Nutrition Inc.

- MusclePharm Corporation

- KeHE Distributors (private label brands)

- Amway Corp.