Probiotics Market Size

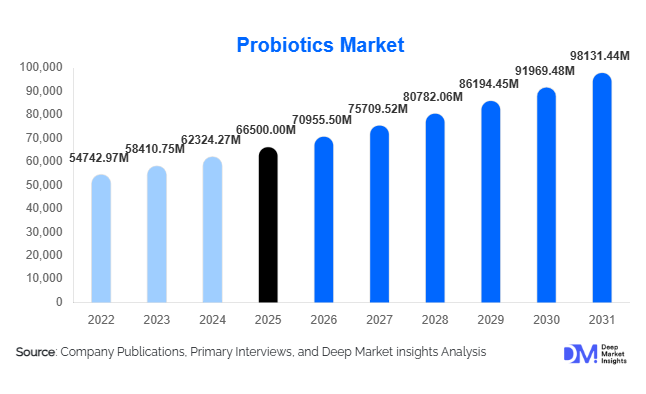

According to Deep Market Insights, the global probiotics market size was valued at USD 66,500 million in 2025 and is projected to grow from USD 70,955.50 million in 2026 to reach USD 98,131.44 million by 2031, expanding at a CAGR of 6.7% during the forecast period (2026–2031). The probiotics market growth is primarily driven by rising consumer awareness of gut health, increasing adoption of preventive healthcare, expanding applications in functional foods and dietary supplements, and regulatory restrictions on antibiotic growth promoters in animal feed.

Key Market Insights

- Functional foods and beverages account for nearly 48% of global revenue, led by yogurt and fermented dairy consumption in Asia-Pacific and Europe.

- Lactobacillus strains dominate with approximately 41% market share, supported by strong clinical validation and formulation stability.

- Dietary supplements are the fastest-growing product category, benefiting from e-commerce expansion and personalized nutrition trends.

- Asia-Pacific leads with 38% of global demand, driven by China, Japan, and India’s growing consumer base.

- Animal probiotics are expanding steadily, particularly in poultry and aquaculture, as antibiotic substitutes gain regulatory backing.

- Microencapsulation and shelf-stable technologies are reshaping product innovation and global distribution efficiency.

What are the latest trends in the probiotics market?

Personalized and Microbiome-Based Nutrition

The probiotics industry is witnessing strong growth in personalized nutrition models. Microbiome testing kits, combined with AI-driven supplement recommendations, are enabling personalized probiotic regimens. Consumers increasingly prefer strain-specific formulations targeting digestive balance, mental wellness (psychobiotics), women’s health, and metabolic function. Subscription-based delivery models are expanding in North America and Europe, enhancing recurring revenue streams. Companies investing in proprietary strain libraries and clinical research are differentiating themselves in a competitive marketplace.

Expansion into Non-Dairy and Plant-Based Formats

Growing vegan and lactose-intolerant populations are accelerating innovation in non-dairy probiotic beverages and plant-based yogurts. Probiotic-infused juices, kombucha, oat-based drinks, and plant-based supplements are expanding shelf presence. This trend is particularly strong in the U.S., Germany, and Australia, where plant-based food penetration is high. The shift reduces dependence on dairy supply chains while broadening the consumer base.

What are the key drivers in the probiotics market?

Growing Focus on Preventive Healthcare

Consumers are increasingly adopting preventive wellness solutions to manage digestive disorders, immunity concerns, and metabolic health. The global dietary supplement industry, valued at over USD 180 billion, is expanding at a nearly 8% CAGR, directly fueling probiotic demand. Rising healthcare costs are further encouraging consumers to adopt cost-effective preventive solutions.

Regulatory Push Against Antibiotic Growth Promoters

Stringent regulations in Europe and gradual restrictions across the Asia-Pacific on antibiotic growth promoters in animal feed are structurally boosting demand for animal probiotics. Poultry and aquaculture industries are increasingly integrating probiotics to improve feed conversion ratios and animal immunity, driving consistent B2B demand.

What are the restraints for the global market?

Strain-Specific Regulatory Complexities

Health claims require robust clinical validation, which increases R&D expenditure and prolongs product approval cycles. Regulatory frameworks vary significantly across regions, limiting cross-border scalability.

Stability and Storage Challenges

Maintaining bacterial viability during transportation and storage remains a challenge, particularly in emerging markets with high temperatures and limited cold-chain infrastructure. This increases production and logistics costs.

What are the key opportunities in the probiotics industry?

Animal Nutrition Expansion in Emerging Markets

India, Brazil, Vietnam, and Indonesia present high-growth opportunities in poultry and aquaculture probiotics. As feed producers shift away from antibiotics, demand for cost-effective microbial feed additives is expected to accelerate at an 8–9% CAGR in these regions.

Psychobiotics and Mental Wellness Applications

Emerging research on the gut-brain axis is opening new revenue streams in stress management, sleep enhancement, and cognitive health. Psychobiotics command premium pricing due to clinical backing and limited competition, making them a high-margin segment.

Product Type Insights

Probiotic foods and beverages continue to dominate the global market, accounting for approximately 48% of total revenue in 2025. This leadership is primarily driven by strong consumer acceptance of yogurt, fermented milk drinks, kefir, and functional beverages fortified with live cultures. The segment benefits from habitual consumption patterns, especially in Asia-Pacific and Europe, where fermented dairy is deeply embedded in traditional diets. In addition, continuous product innovation, such as low-sugar, lactose-free, and plant-based probiotic beverages, has expanded the consumer base beyond conventional dairy consumers. Large food manufacturers are leveraging established cold-chain networks and retail penetration to maintain scale advantages, further reinforcing the segment’s dominance.

Dietary supplements represent nearly 37% of global revenue and are the fastest-growing product type, expanding at approximately 7.5% CAGR. Growth is driven by increasing consumer demand for targeted, strain-specific formulations addressing digestive health, immunity, women’s health, and mental wellness. Capsule, gummy, sachet, and stick-pack formats have improved convenience and compliance. The rapid rise of e-commerce, subscription-based models, and direct-to-consumer (D2C) brands is accelerating supplement penetration, particularly in North America and Europe. Animal probiotics account for roughly 15% of total market revenue. Growth in this segment is structurally supported by regulatory-driven feed reformulations that replace antibiotic growth promoters with microbial alternatives. Poultry and aquaculture applications are leading adoption due to measurable improvements in feed efficiency, animal immunity, and export compliance.

Application Insights

Digestive health applications dominate the probiotics market, contributing nearly 52% of total demand. The high prevalence of gastrointestinal disorders, including IBS, bloating, and antibiotic-associated diarrhea, remains the primary growth driver. Clinically validated strains targeting gut microbiota balance continue to strengthen consumer trust, making digestive health the foundational application across both food and supplement formats.

Immunity enhancement accounts for approximately 21% of market demand, supported by sustained post-pandemic awareness of immune resilience. Probiotic formulations combining vitamins, minerals, and prebiotics are gaining traction as multifunctional health solutions. Women’s health and infant nutrition are emerging high-growth sub-segments, benefiting from increasing research linking probiotics to vaginal health, prenatal wellness, and early-life microbiome development. Mental wellness applications, including psychobiotics targeting stress, anxiety, and sleep regulation, represent a smaller but rapidly expanding niche. Rising awareness of the gut-brain axis and increasing clinical studies are expected to drive above-average growth in this category over the next five years.

Distribution Channel Insights

Supermarkets and hypermarkets account for nearly 38% of global probiotic sales, particularly for foods and beverages. Their dominance is supported by high consumer footfall, established cold-chain infrastructure, and impulse purchase behavior in dairy aisles. Large retail chains also provide shelf visibility for multinational brands, sustaining volume leadership.

Pharmacies and drug stores represent approximately 27% of total sales, serving as trusted channels for dietary supplements. Pharmacist recommendations and proximity to healthcare ecosystems strengthen credibility, particularly for clinically validated formulations. Online retail contributes close to 20% of global sales and is growing at double-digit rates. The expansion of subscription-based supplement models, personalized microbiome kits, and influencer-driven marketing has accelerated digital channel growth. Specialty health stores maintain a niche presence, focusing on premium, organic, and high-potency formulations.

End-Use Industry Insights

The food and beverage industry accounts for approximately 45% of total probiotic demand, supported by the steady expansion of the global functional foods sector. Fermented dairy, plant-based probiotic beverages, and fortified snacks are key growth contributors. The dietary supplement industry, expanding at nearly 8% CAGR, represents a high-margin end-use sector characterized by premium pricing and recurring consumer purchases.

The global animal feed industry, valued at over USD 500 billion, is steadily increasing probiotic inclusion rates, particularly in poultry and aquaculture feed formulations. Export-oriented meat producers are adopting probiotics to meet international antibiotic-free compliance standards. Denmark, the United States, and China serve as major probiotic ingredient exporters, reinforcing strong export-driven demand dynamics in both human and animal nutrition markets.

| By Product Type | By Application | By Distribution Channel |

|---|---|---|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global probiotics market with approximately 38% market share in 2025. China accounts for nearly 45% of regional demand, driven by rising middle-class incomes, strong consumption of infant nutrition, and expanding dietary supplement adoption. Government support for biotechnology manufacturing and increasing awareness of gut health are accelerating domestic production capacity. Japan remains a mature, innovation-driven market, supported by high penetration of fermented dairy and functional food consumption. India is the fastest-growing country in the region, registering around 9% CAGR, fueled by rapid urbanization, increasing disposable income, and strong growth in poultry feed probiotics driven by expanding meat exports.

North America

North America holds nearly 30% of the global market share, with the United States contributing approximately 85% of regional revenue. Growth drivers include high dietary supplement penetration, advanced microbiome research infrastructure, and strong consumer inclination toward personalized nutrition. Premium pricing models and subscription-based D2C platforms further enhance revenue growth. Increasing clinical validation and rising demand for psychobiotics are also supporting sustained regional expansion at approximately 6% CAGR.

Europe

Europe represents about 22% of global demand, led by Germany, France, the UK, and Italy. Strict regulatory bans on antibiotic growth promoters have structurally increased animal probiotic adoption. High consumer awareness of functional foods and sustainability preferences further supports demand. Germany leads regional consumption due to a strong dairy culture and supplement penetration, while Nordic countries drive innovation in strain development and exports.

Latin America

Latin America accounts for approximately 6% of global revenue, with Brazil and Mexico as primary markets. The region’s strong poultry and livestock export industries are key drivers for animal probiotic demand. Rising urbanization and growing middle-class populations are gradually increasing supplement adoption. Government initiatives promoting food safety and antibiotic reduction in livestock production further support regional growth.

Middle East & Africa

The Middle East & Africa region holds nearly 4% of the global market share. The UAE and Saudi Arabia are driving supplement demand through rising health awareness and premium retail expansion. South Africa leads sub-Saharan Africa due to livestock modernization and functional food adoption. Government-led food security initiatives and increasing imports of probiotic ingredients are supporting steady market expansion across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Probiotics Market

- Chr. Hansen

- Danone

- Yakult Honsha

- Nestlé

- BioGaia

- Probi AB

- Kerry Group

- Lallemand

- DSM-Firmenich

- ADM

- IFF Health

- Morinaga Milk Industry

- Arla Foods

- Synlogic

- Sabinsa