Prebiotics Market Size

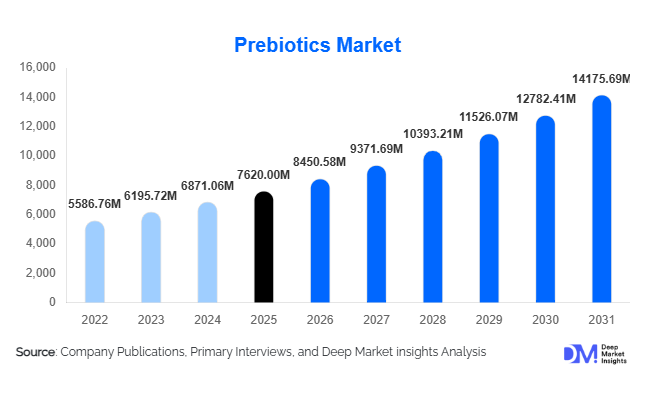

According to Deep Market Insights,the global prebiotics market size was valued at USD 7,620 million in 2025 and is projected to grow from USD 8,450.58 million in 2026 to reach USD 14,175.69 million by 2031, expanding at a CAGR of 10.9% during the forecast period (2026–2031). The prebiotics market growth is primarily driven by rising consumer awareness of gut health, increasing integration of dietary fibers in functional foods, and expanding applications across nutraceuticals, infant nutrition, and animal feed. Growing scientific validation of microbiome health benefits and regulatory recognition of key prebiotic ingredients as dietary fibers are further accelerating adoption globally.

Key Market Insights

- Inulin remains the dominant ingredient type, accounting for nearly 32% of the 2025 market, due to multifunctionality in food formulation and broad regulatory approvals.

- Functional food & beverages represent the largest application segment, contributing approximately 48% of total market demand.

- Powder form dominates globally, holding around 55% share, owing to ease of processing, longer shelf life, and formulation stability.

- North America leads the global market with nearly 30% share in 2025, supported by high supplement penetration and strong clean-label demand.

- Asia-Pacific is the fastest-growing region, expanding at over 12% CAGR, driven by infant nutrition demand and expanding middle-class populations.

- Direct B2B distribution channels account for nearly 60% of sales, reflecting long-term supply contracts between ingredient manufacturers and food producers.

What are the latest trends in the prebiotics market?

Synbiotic and Personalized Nutrition Expansion

The integration of prebiotics with probiotics into synbiotic formulations is accelerating innovation across supplements and fortified foods. Manufacturers are investing in microbiome research and AI-based personalization platforms to develop targeted gut-health solutions. Personalized fiber blends tailored to metabolic health, immunity, and digestive disorders are gaining traction in developed markets. Clinical research partnerships and biotechnology investments are expanding the pipeline of next-generation oligosaccharides derived through precision fermentation, enhancing efficacy and premium pricing potential.

Clean-Label and Plant-Based Ingredient Adoption

Consumer demand for natural, plant-derived, and non-GMO ingredients is reshaping sourcing strategies. Chicory-root-derived inulin and cereal-based resistant dextrin are witnessing strong uptake as sugar reduction and fat replacement solutions in bakery and dairy alternatives. Sustainability commitments are also influencing procurement decisions, with companies investing in traceable sourcing, regenerative agriculture, and carbon-neutral extraction technologies. This trend aligns closely with rising global dietary fiber consumption recommendations and regulatory clarity around labeling claims.

What are the key drivers in the prebiotics market?

Rising Gut Health Awareness

Growing recognition of the link between gut microbiota and immunity, metabolism, and mental health is a major growth driver. Consumers are actively seeking fiber-enriched foods and digestive supplements, particularly in North America, Europe, China, and Japan. Preventive healthcare spending and post-pandemic immunity focus have significantly accelerated demand.

Expansion of Functional Food Industry

The global functional food industry, valued at over USD 300 billion, is integrating prebiotic ingredients across yogurt, beverages, cereals, protein bars, and infant formula. Large-scale fortification initiatives by multinational food manufacturers are driving bulk ingredient procurement, strengthening long-term supply contracts.

What are the restraints for the global market?

Raw Material Price Volatility

Dependence on chicory root and cereal feedstocks exposes manufacturers to agricultural fluctuations, climate variability, and energy-intensive extraction costs. Price instability can compress margins, particularly for mid-sized producers.

Consumer Education Gaps

Despite market growth, confusion between probiotics and prebiotics persists in emerging economies. Limited understanding of functional differences may slow penetration in price-sensitive regions, requiring greater marketing and educational investment.

What are the key opportunities in the prebiotics industry?

Clinical and Medical Nutrition Applications

Growing cases of IBS, metabolic syndrome, and antibiotic-associated gut imbalance create opportunities for medical-grade prebiotics in pharmaceutical and hospital nutrition programs. Clinical validation enhances premium pricing and strengthens regulatory claims.

Emerging Market Penetration

Countries such as China, India, Brazil, and Indonesia offer substantial untapped potential due to urbanization, rising disposable incomes, and preventive healthcare awareness. Localization of manufacturing facilities in Asia is improving cost competitiveness and export potential.

Ingredient Type Insights

Inulin dominates the global prebiotics market with approximately 32% share in 2025, primarily driven by its multifunctional performance as a soluble dietary fiber, fat replacer, and sugar substitute across food and beverage formulations. Its neutral taste profile, proven digestive health benefits, and compatibility with dairy, bakery, and functional beverage applications position it as the leading ingredient segment. The growing regulatory acceptance of fiber health claims in major markets further reinforces inulin’s commercial leadership. Fructooligosaccharides (FOS) and Galactooligosaccharides (GOS) continue to gain widespread adoption in infant nutrition and fortified beverages due to their clinically supported role in gut microbiota modulation and immune health. Rising global birth rates in developing economies and premiumization in infant formula formulations are accelerating FOS and GOS demand. Resistant dextrin is witnessing increasing penetration in sports nutrition, meal replacements, and low-calorie beverages, supported by rising consumer preference for digestive-friendly carbohydrate alternatives. Mannan oligosaccharides (MOS) maintain steady demand in animal feed applications, particularly in Europe and Asia, where antibiotic reduction policies are encouraging the adoption of gut-health-enhancing feed additives.

Source Insights

Chicory root accounts for nearly 40% of total raw material sourcing, supported by its high inulin concentration, cost efficiency, and well-established cultivation networks across Europe. The region’s strong agricultural infrastructure and export-oriented production capacity make chicory-derived inulin a globally traded commodity. Cereal-based sources such as wheat and corn are gaining prominence in North America and Asia due to large-scale agricultural output, integrated supply chains, and cost advantages. These sources are increasingly utilized for resistant dextrin production and industrial-scale fiber enrichment. Bio-fermentation-based production is emerging as a sustainable and technologically advanced alternative, offering improved yield consistency, purity, and scalability. Advances in enzymatic processing and microbial fermentation technologies are enhancing production efficiency while aligning with sustainability goals and clean-label positioning.

Form Insights

Powdered prebiotics hold around 55% of the global market share, driven by their extended shelf life, ease of storage and transportation, and seamless compatibility with large-scale food and beverage manufacturing systems. The stability of powdered formulations under varying processing conditions makes them ideal for dairy fortification, bakery integration, and powdered supplement blends, reinforcing their leadership in the segment. Liquid and syrup forms are primarily used in beverage manufacturing where rapid solubility and uniform dispersion are critical for product consistency. Capsules and tablets are expanding rapidly within nutraceutical applications, supported by rising consumer preference for convenient digestive health supplements and personalized nutrition formats.

Application Insights

Functional food and beverages represent approximately 48% of total demand, making them the leading application segment. Growth is primarily driven by dairy fortification, bakery reformulation to enhance fiber content, and the proliferation of fiber-enriched drinks targeting digestive wellness. Increasing consumer awareness of gut microbiome health and clean-label formulation trends are accelerating product innovation in this category. Dietary supplements are the fastest-growing segment, expanding at double-digit rates due to heightened digestive health awareness, aging populations, and preventive healthcare adoption. The animal feed segment is also expanding steadily as regulatory restrictions on antibiotic growth promoters in Europe and parts of Asia are encouraging the use of prebiotic alternatives to enhance livestock gut health and productivity.

Distribution Channel Insights

Direct B2B sales account for nearly 60% of total market transactions, reflecting long-term procurement agreements between ingredient manufacturers and multinational food and beverage companies. Strategic supplier partnerships, volume-based contracts, and integrated supply chain models continue to support the dominance of this channel. Specialty ingredient distributors play a critical role in serving mid-sized processors and regional manufacturers by offering customized ingredient blends and technical support. Digital B2B procurement platforms are gradually emerging as secondary channels, enhancing price transparency, improving logistics efficiency, and enabling smaller manufacturers to access global suppliers.

End-Use Industry Insights

The food and beverage manufacturing industry remains the largest end-use sector, contributing roughly 50% of global demand, driven by continuous product reformulation toward high-fiber and gut-health-enhancing offerings. The nutraceutical industry represents the fastest-growing end-use segment, expanding at over 11% annually, supported by rising demand for digestive health supplements and personalized nutrition solutions. Pharmaceutical companies are increasingly integrating prebiotics into gastrointestinal health formulations and synbiotic therapies, reflecting growing clinical validation of microbiome-targeted interventions. Cosmetic applications are emerging within microbiome-based skincare formulations, particularly in premium beauty segments. Export-driven demand remains strong from Europe and China, while North America serves as a major importer of chicory-derived inulin to support its large functional food and supplement industries.

| By Ingredient Type | By Application | By Form | By Source |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 30% of the global market in 2025, with the United States leading regional consumption due to strong dietary supplement penetration, advanced functional food manufacturing capabilities, and increasing consumer focus on digestive health. Growth is further supported by favorable regulatory recognition of dietary fiber claims, high disposable incomes, and expanding clean-label product portfolios. Canada demonstrates steady growth driven by health-conscious consumer behavior, government-backed nutrition labeling initiatives, and rising demand for plant-based fortified foods. Robust retail infrastructure and e-commerce penetration also contribute to sustained regional expansion.

Europe

Europe holds nearly 28% market share, led by Germany, France, and the Netherlands. The region benefits from established chicory cultivation, vertically integrated processing facilities, and strong export infrastructure, making it a global production hub for inulin. Regulatory clarity within the European Union regarding fiber health claims and microbiome research funding continues to strengthen innovation and product development. Additionally, stringent antibiotic reduction policies in livestock farming are accelerating prebiotic inclusion in animal feed, further supporting regional demand growth.

Asia-Pacific

Asia-Pacific is the fastest-growing region with a CAGR exceeding 12%, driven by expanding middle-class populations, rising preventive healthcare awareness, and rapid urbanization. China dominates regional demand, particularly in infant formula, dairy fortification, and functional beverages, supported by strong domestic manufacturing capacity and growing health consciousness among parents. India is witnessing rapid growth fueled by increasing digestive health awareness, expanding nutraceutical production, and rising demand for fiber-enriched packaged foods. Japan maintains mature but stable demand, particularly for FOS-integrated functional beverages and scientifically validated gut-health products, supported by its aging population and established functional food culture.

Latin America

Brazil leads Latin American demand, supported by expanding nutraceutical manufacturing, rising functional beverage consumption, and growing awareness of digestive wellness. Increasing urbanization and improvements in retail distribution networks are enhancing product accessibility across major cities. Mexico and Argentina are gradually increasing imports of prebiotic ingredients to support domestic food reformulation efforts, while regional trade agreements are facilitating ingredient availability and cross-border supply chains.

Middle East & Africa

The United Arab Emirates and Saudi Arabia represent key import-driven markets within the Middle East, supported by high disposable incomes, growing health awareness, and expanding premium food retail sectors. Government initiatives promoting food security and local food processing investments are further supporting ingredient demand. South Africa leads African consumption, driven by the expansion of processed food industries, rising middle-class populations, and increasing consumer interest in digestive health solutions. Gradual modernization of retail infrastructure and increasing foreign investment in food manufacturing are expected to support steady regional growth.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Prebiotics Market

- BENEO

- Ingredion Incorporated

- Tate & Lyle

- DuPont

- FrieslandCampina

- Cargill

- Roquette Frères

- Cosucra

- Sensus

- Kerry Group

- ADM

- BASF

- Givaudan

- Fonterra

- Yakult Honsha Co., Ltd.