Plant-Based Organic Acids Market Size

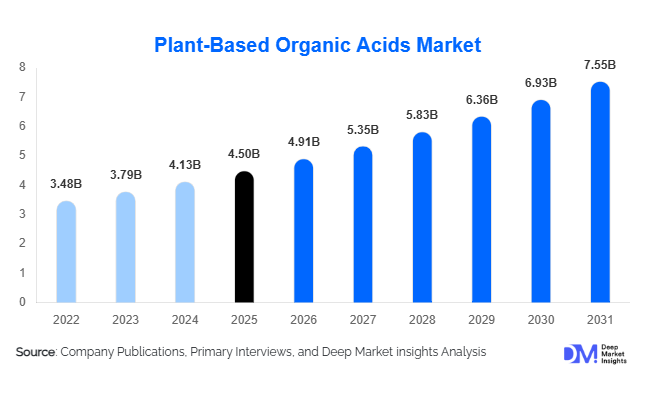

According to Deep Market Insights, the global plant-based organic acids market size was valued at USD 4.5 billion in 2025 and is projected to grow from USD 4.91 billion in 2025 to reach USD 7.55 billion by 2030, expanding at a CAGR of 9.0% during the forecast period (2025–2031). The market growth is primarily driven by increasing consumer preference for clean-label and natural ingredients, rising adoption of sustainable bio-based chemicals across food, pharmaceutical, cosmetics, and industrial applications, and expanding demand for eco-friendly materials such as bioplastics.

Key Market Insights

- Citric acid remains the leading plant-based organic acid globally, widely used in food preservation, flavoring, and pharmaceutical intermediates.

- Food & beverages dominate the end-use segment, driven by clean-label trends and natural preservatives replacing synthetic alternatives.

- North America holds significant market share, supported by advanced food processing and pharmaceutical industries alongside regulatory incentives for bio-based products.

- Asia-Pacific is the fastest-growing region, led by China and India due to industrial expansion, low-cost manufacturing, and rising consumer awareness.

- Technological advancements in fermentation and enzymatic production, coupled with integrated biorefineries, are improving yields, cost-efficiency, and product quality.

- Emerging applications in bioplastics and agriculture, such as biodegradable polymers and soil health enhancers, are expanding the market beyond traditional sectors.

What are the latest trends in the plant-based organic acids market?

Clean-Label and Natural Ingredient Adoption

Manufacturers are increasingly reformulating products using plant-based organic acids like citric, lactic, and acetic acids to meet consumer demand for natural, non-synthetic ingredients. This trend spans processed foods, beverages, and functional nutrition products. Clean-label positioning enhances brand value and compliance with stricter regulations on synthetic preservatives. Companies are also emphasizing traceability, sourcing acids from renewable feedstocks such as corn, sugarcane, and molasses, highlighting sustainability credentials.

Expansion into Bioplastics and Sustainable Materials

Plant-based organic acids, particularly lactic acid, serve as monomers for biodegradable polymers like PLA. The growing global focus on circular economy and plastic reduction policies is creating demand for bio-based acids in packaging, textiles, and engineering plastics. Companies are integrating fermentation technologies and downstream separation processes to scale production efficiently, enabling plant-based acids to compete with petrochemical-derived alternatives in industrial applications.

What are the key drivers in the plant-based organic acids market?

Rising Clean-Label and Natural Ingredient Demand

Consumers are actively seeking products free from synthetic additives. Food & beverage companies, pharmaceutical firms, and personal care manufacturers are increasingly incorporating plant-based organic acids as natural preservatives, pH regulators, and functional ingredients. This shift is driving consistent growth across multiple end-use industries globally.

Technological Advancements in Fermentation

Improvements in microbial fermentation, enzymatic processes, and biorefinery technologies have enhanced yields and lowered production costs. These advances enable manufacturers to produce plant-based organic acids at scale while maintaining quality and sustainability, increasing competitiveness with synthetic counterparts.

Government Support and Sustainability Policies

Regulatory frameworks in North America, Europe, and parts of Asia-Pacific incentivize renewable chemical production, offering tax credits, subsidies, and green certifications. Such policies encourage adoption of plant-based organic acids and foster investment in production infrastructure, thereby accelerating market growth.

What are the restraints for the global market?

Raw Material Cost Volatility

Feedstocks such as corn, sugarcane, and molasses are subject to agricultural and commodity price fluctuations. Volatility in raw material costs can negatively impact profit margins and production stability for plant-based organic acid manufacturers.

Infrastructure Limitations in Developing Regions

Limited industrial fermentation capacity and logistical challenges in emerging economies restrict large-scale production and distribution. Overcoming these infrastructure barriers is critical for expanding market reach in developing regions.

What are the key opportunities in the plant-based organic acids market?

Bioplastics and Sustainable Materials Integration

Expanding applications of lactic acid in biodegradable polymers create a high-growth opportunity. Rising awareness of environmental issues and government mandates to reduce single-use plastics increase adoption of bio-based materials, driving demand for plant-based acids in industrial applications.

Growth in Clean-Label Food and Beverage Products

The global trend toward natural and minimally processed foods presents opportunities for citric, lactic, and malic acids as natural preservatives and flavor enhancers. Manufacturers can leverage clean-label positioning to differentiate products, improve brand loyalty, and expand market penetration.

Sustainable Agriculture Applications

Plant-based organic acids are increasingly used in agriculture as bio-stimulants, soil conditioners, and nutrient enhancers. Rising focus on eco-friendly farming practices and soil health management is expected to drive adoption of bio-based acids in agriculte-ingredients-market-research-reporural inputs.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.5 Billion |

| Market Size in 2026 | USD 4.91 Billion |

| Market Size in 2031 | USD 7.55 Billion |

| CAGR | 9.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Citric acid dominates the global plant-based organic acids market, accounting for approximately 32% of total revenue in 2025. Its leadership is primarily driven by its extensive use in the food and beverage industry as a natural preservative, acidulant, and flavor enhancer, as well as its critical role in pharmaceutical formulations and nutraceutical products. The acid’s proven safety profile, regulatory acceptance across major economies, and cost-efficient fermentation-based production further strengthen its market position.

Lactic acid is emerging as the fastest-growing product segment, driven by its expanding application in biodegradable plastics, medical devices, and personal care formulations. Growing investments in biopolymer manufacturing and rising demand for polylactic acid (PLA) are significantly accelerating lactic acid adoption. Acetic acid and malic acid continue to serve important niche and specialty applications, particularly in food processing, beverages, and industrial cleaning, supporting steady demand growth.

Application Insights

Food preservation remains the leading application segment, contributing nearly 30% of the total market revenue in 2025. The segment’s dominance is driven by increasing global demand for clean-label foods, heightened consumer awareness of synthetic additive risks, and stringent food safety regulations encouraging the replacement of artificial food preservatives with natural alternatives.

Bioplastics and agricultural applications are emerging as high-growth segments, offering manufacturers opportunities to diversify beyond traditional food and beverage uses. In bioplastics, plant-based organic acids are critical intermediates in biodegradable polymer production, while in agriculture, they are increasingly used as soil conditioners, feed additives, and crop protection agents, driven by sustainability mandates and organic farming expansion.

Distribution Channel Insights

B2B direct sales dominate the distribution landscape, accounting for approximately 48% of total market share. This channel benefits from long-term supply contracts with large food processors, pharmaceutical manufacturers, and agricultural input companies, ensuring consistent quality, traceability, and supply reliability.

Distributor networks and online sales platforms play a complementary role, particularly in serving small- and medium-scale manufacturers, specialty chemical buyers, and emerging market participants. The increasing digitization of procurement processes and cross-border e-commerce is further enhancing accessibility to plant-based organic acids across global markets.

End-Use Insights

The food and beverage industry remains the largest end-use sector, accounting for approximately 37% of total demand in 2025, supported by rising consumption of processed foods, beverages, and functional food products. Pharmaceuticals follow with nearly 20% share, driven by increasing use of organic acids in drug formulations, excipients, and controlled-release systems.

The personal care and cosmetics sector contributes around 15% of demand, benefiting from consumer preference for natural, plant-derived ingredients in skincare, haircare, and hygiene products. Bioplastics and agriculture represent rapidly expanding end-use segments, driven by global sustainability regulations, bio-based material mandates, and growing adoption of eco-friendly farming practices. Additionally, export-driven demand is rising, with North America and Europe increasingly importing high-purity plant-based organic acids from Asia-Pacific manufacturing hubs.

Explore more data points, trends and opportunities Download Free Sample Report

Plant-Based Organic Acids Market Segmentations

By Product Type

- Citric Acid

- Lactic Acid

- Acetic Acid

- Fumaric Acid

- Malic Acid

- Tartaric Acid

- Formic Acid

- Other Organic Acids

By Application

- Food Preservation

- Pharmaceuticals

- Agriculture

- Cosmetics & Personal Care

- Bioplastics & Sustainable Materials

- Industrial Biotechnology & Chemicals

By End-Use Industry

- Food & Beverages

- Pharmaceutical & Healthcare

- Agricultural Inputs & Crop Protection

- Personal Care & Cosmetics

- Packaging & Bioplastics

- Chemical Processing

By Form / Physical State

- Liquid

- Powder

- Granular

By Distribution Channel

- B2B Direct Sales

- Distributors & Wholesale

- E-commerce / Online Platforms

- Retail Specialty Outlets

Regional Insights

North America

North America accounts for approximately 30% of the global market, supported by strong demand from food processing, pharmaceutical, and cosmetic industries. The United States leads regional growth due to widespread clean-label adoption, advanced food safety regulations, and government incentives promoting bio-based chemicals. Canada is witnessing steady growth driven by rising consumer awareness, investments in sustainable manufacturing, and increased adoption of plant-derived ingredients across end-use sectors.

Europe

Europe represents nearly 20% of global market share, with key contributions from Germany, France, and the United Kingdom. Growth in the region is driven by stringent environmental regulations, strong consumer preference for natural and organic ingredients, and government initiatives promoting renewable and bio-based chemicals. The presence of eco-certification programs and sustainability-focused procurement policies among food and cosmetic manufacturers further strengthens regional demand.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, led by China and India. Rapid industrialization, expanding food processing capacity, and low-cost fermentation-based production provide a competitive advantage to regional manufacturers. Growth is further supported by rising demand from pharmaceutical, bioplastics, and agricultural sectors, along with increasing adoption of plant-based organic acids in industrial and export-oriented applications.

Latin America

Latin America, led by Brazil and Mexico, is emerging as a promising growth region due to expanding processed food consumption and increasing use of organic acids in agricultural applications. Favorable climatic conditions for biomass availability support local production potential, although infrastructure limitations and regulatory variability continue to moderate adoption rates. Growth remains steady, particularly among mid-tier manufacturers.

Middle East & Africa

The Middle East & Africa region is witnessing gradual growth, supported by abundant natural resources and increasing industrial diversification. Countries such as the UAE and Saudi Arabia are experiencing rising adoption in pharmaceutical and cosmetic manufacturing, driven by healthcare investment and premium personal care demand. In Africa, expanding intra-regional trade, agricultural modernization, and growing awareness of sustainable inputs are supporting the gradual uptake of plant-based organic acids across multiple applications.

Key Players in the Plant-Based Organic Acids Market

- Cargill, Inc.

- ADM (Archer Daniels Midland)

- Corbion N.V.

- BASF SE

- Eastman Chemical Company

- Celanese Corporation

- Evonik Industries AG

- Jungbunzlauer Suisse AG

- Tate & Lyle PLC

- Royal DSM

- Weifang Ensign Industry Co., Ltd.

- Shandong Baoyuan Chemical Co., Ltd.

- Fuso Chemical Co., Ltd.

- Yara International ASA