Food Preservatives Market Size

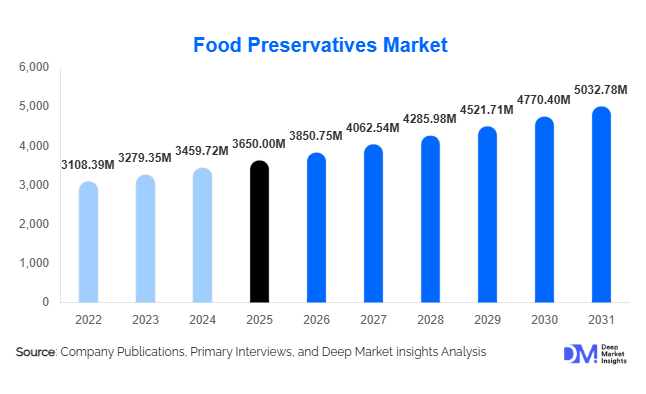

According to Deep Market Insights, the global food preservatives market size was valued at USD 3,650 million in 2025 and is projected to grow from USD 3,850.75 million in 2026 to reach USD 5,032.78 million by 2031, expanding at a CAGR of 5.5% during the forecast period (2026–2031). The food preservatives market growth is primarily driven by the rising consumption of packaged and processed foods, increasing global food trade, and the critical need to extend shelf life while maintaining food safety and quality across complex supply chains.

Key Market Insights

- Synthetic preservatives continue to dominate due to cost efficiency, broad-spectrum antimicrobial activity, and ease of formulation across high-volume food categories.

- Natural and clean-label preservatives are the fastest-growing segment, driven by consumer demand for transparency, minimally processed foods, and regulatory pressure on artificial additives.

- Antimicrobial preservatives represent the largest functional category, supported by strong demand from meat, dairy, and ready-to-eat food manufacturers.

- Asia-Pacific is the fastest-growing regional market, fueled by rapid urbanization, rising middle-class incomes, and the expansion of domestic food processing industries.

- Bakery, meat, and dairy applications account for the majority of demand, as these segments rely heavily on preservatives for shelf-life stability and food safety compliance.

- Technological innovation, including fermentation-derived preservatives and synergistic preservative blends, is reshaping product development strategies.

What are the latest trends in the food preservatives market?

Shift Toward Natural and Fermentation-Based Preservatives

The most prominent trend in the food preservatives market is the accelerating shift toward natural, clean-label, and fermentation-based solutions. Food manufacturers are increasingly replacing traditional synthetic preservatives with organic acids, cultured dextrose, vinegar powders, and plant extracts to meet consumer expectations and regulatory guidelines. Fermentation-derived antimicrobials such as nisin and natamycin are gaining widespread adoption, particularly in dairy and meat products, due to their effectiveness and regulatory acceptance. This trend is pushing suppliers to invest in biotechnology, strain development, and scalable fermentation capacity.

Development of Multifunctional Preservative Systems

Manufacturers are increasingly adopting multifunctional preservative systems that combine antimicrobial, antioxidant, and anti-browning properties into single formulations. These systems help reduce overall additive usage, optimize costs, and support clean-label positioning. Advanced technologies such as encapsulation, controlled-release systems, and hurdle technology are enabling lower dosage levels while maintaining shelf-life performance. This trend is particularly strong in ready-to-eat meals, beverages, and export-oriented food products.

What are the key drivers in the food preservatives market?

Growth of Processed and Convenience Foods

The global rise in consumption of processed, packaged, and ready-to-eat foods is a major driver of the food preservatives market. Urban lifestyles, increasing workforce participation, and demand for convenience have significantly expanded the use of preservatives across bakery, snacks, frozen foods, and beverages. Modern retail and e-commerce grocery platforms further increase the need for extended shelf life, directly supporting preservative demand.

Stringent Food Safety and Quality Regulations

Governments worldwide enforce strict microbial safety and shelf-life standards, particularly for meat, dairy, and beverages. Preservatives remain one of the most cost-effective and reliable solutions for regulatory compliance. Export-oriented food manufacturers rely heavily on preservatives to meet international food safety norms, further strengthening demand.

What are the restraints for the global market?

Regulatory Restrictions on Synthetic Preservatives

Increasing regulatory scrutiny on synthetic preservatives such as nitrites, sulfites, and benzoates is a key restraint. Limits on permissible usage levels and mandatory labeling requirements increase reformulation costs and lengthen product approval timelines, particularly in Europe and North America.

Higher Cost of Natural Preservatives

Natural and clean-label preservatives are generally more expensive than synthetic alternatives, limiting adoption among small and mid-sized food processors. Price sensitivity in developing markets continues to slow the transition toward natural solutions.

What are the key opportunities in the food preservatives industry?

Expansion in Emerging Food Processing Markets

Asia-Pacific, Latin America, and parts of Africa present strong growth opportunities due to rising packaged food consumption and government investments in domestic food processing infrastructure. Localized preservative solutions tailored to regional diets and climatic conditions offer significant potential for both multinational and regional suppliers.

Innovation in Clean-Label and Low-Dosage Technologies

Opportunities exist in developing low-dosage, high-efficacy preservative systems that balance clean-label requirements with cost efficiency. Companies investing in fermentation technology, plant-based extracts, and synergistic blends can achieve premium pricing and long-term supply contracts.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3650 Million |

| Market Size in 2026 | USD 3850.75 Million |

| Market Size in 2031 | USD 5032.78 Million |

| CAGR | 5.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Chemical preservatives dominate the market, accounting for approximately 45% of the 2024 share, due to their cost-efficiency, stability, and widespread application across bakery, dairy, and beverage products. Their proven effectiveness in extending shelf-life and maintaining microbial safety makes them the preferred choice for large-scale industrial food processing. Meanwhile, natural preservatives are rapidly gaining traction, fueled by growing consumer preference for clean-label, organic, and minimally processed foods. The rising health consciousness and willingness to pay a premium for natural solutions are driving their adoption, particularly in North America and Europe. Antioxidants, both synthetic and natural, are increasingly used to prevent oxidation in beverages, snacks, and packaged foods, maintaining product quality over extended storage periods. Furthermore, multifunctional preservatives that combine antimicrobial and antioxidant properties are emerging as key innovations, enabling manufacturers to meet regulatory requirements, reduce additive load, and cater to evolving consumer preferences. The trend toward multifunctional and natural preservatives is expected to accelerate, particularly in premium and export-oriented food segments.

Application Insights

The dairy and frozen desserts segment leads the application market with a 28% share in 2024. Products such as milk, yogurt, cheese, and ice cream rely on preservatives like natamycin, sorbates, and organic acids to maintain microbial stability and prolong shelf-life. The bakery segment follows closely, with chemical preservatives such as benzoates and sorbates ensuring freshness in bread, cakes, and confectionery products. Beverages, including juices and carbonated drinks, predominantly use antioxidants to prevent oxidation and maintain flavor integrity. Meat and seafood products also increasingly depend on both chemical and natural preservatives to control microbial growth and meet export standards. Emerging applications include plant-based dairy alternatives, functional foods, and premium snacks, reflecting the rising demand for innovative products with extended shelf-life and clean-label formulations.

Distribution Channel Insights

Direct B2B sales remain the dominant distribution channel, as food processors source preservatives directly from manufacturers to ensure quality and consistency for large-scale production. Ingredient distributors and wholesalers support smaller regional food manufacturers and processors, providing flexibility in order size and delivery. The increasing adoption of online B2B platforms facilitates bulk ordering, enhances transparency, and simplifies international trade, particularly for export-oriented manufacturers. Export-focused distributors play a critical role in regions with stringent food safety regulations, helping manufacturers meet local compliance standards. Overall, the integration of digital platforms and efficient supply chains is strengthening market accessibility and global reach for preservative products.

End-Use Insights

The food processing industry is the largest end-user segment, accounting for approximately 55% of the market, driven by high demand for packaged and ready-to-eat products. Beverage manufacturers and snack producers follow closely, relying on preservatives to ensure product stability and extend shelf-life. Emerging end-use segments, such as plant-based dairy alternatives, premium confectionery, and functional foods, are creating additional growth avenues. Export-driven demand is particularly high in the U.S., Germany, India, and China, where preservatives enable compliance with international shelf-life standards. The rising consumer emphasis on natural ingredients and multifunctional preservatives is pushing end-users to adopt innovative preservative solutions that meet both regulatory requirements and market expectations.

Explore more data points, trends and opportunities Download Free Sample Report

Food Preservatives Market Segmentations

By Product Type

- Chemical Preservatives

- Natural/Organic Preservatives

- Antioxidants

- Multifunctional Preservatives

By Application

- Dairy & Frozen Desserts

- Bakery & Confectionery

- Beverages

- Meat, Poultry & Seafood

- Fruits & Vegetables

- Snacks & Ready-to-Eat Foods

By Distribution Channel

- Direct B2B Sales

- Ingredient Distributors & Wholesalers

- Online B2B Platforms

- Export-Oriented Distributors

By End-Use Industry

- Food Processing Industry

- Beverage Manufacturing

- Retail/Private Label Packaged Foods

- Foodservice & Catering

Regional Insights

North America

North America holds approximately 30% of the global market, led by the U.S. and Canada. Growth is driven by strong packaged food consumption, high adoption of natural and multifunctional preservatives, and stringent food safety regulations. Consumer demand for clean-label, organic, and premium products is encouraging manufacturers to innovate with plant-based and multifunctional preservatives. Additionally, the region’s mature retail infrastructure, presence of leading food processing companies, and advanced cold-chain logistics enable efficient distribution and support market expansion.

Europe

Europe accounts for around 28% of the market, with Germany, France, and the U.K. leading demand. Growth is primarily driven by rising consumer awareness for health-conscious and clean-label foods, coupled with regulatory alignment with EFSA standards. Export-oriented food industries in Europe are also adopting preservatives to ensure product stability in international markets. Innovation in natural antioxidants and multifunctional preservatives further strengthens market penetration, while premium product lines cater to affluent consumers seeking high-quality, safe, and minimally processed food options.

Asia-Pacific

Asia-Pacific is the fastest-growing region with a CAGR of approximately 7%, driven by China, India, and Japan. Urbanization, increasing disposable incomes, and the rising adoption of packaged and processed foods are primary growth drivers. Modern retail expansion, improved cold-chain infrastructure, and export-oriented food processing industries are fueling demand for both chemical and natural preservatives. Multifunctional preservatives are gaining prominence in APAC to meet international food safety standards and extend product shelf-life, supporting the growth of dairy, beverages, and meat processing segments.

Latin America

In Latin America, Brazil, Mexico, and Argentina are the primary contributors. Growth is driven by expanding urban populations, rising processed food consumption, and increasing industrial-scale food processing. Chemical preservatives dominate due to cost-efficiency, while the adoption of natural and multifunctional preservatives is gradually increasing in premium product segments. Export-oriented food manufacturers are also contributing to regional demand, leveraging preservatives to comply with international shelf-life and safety standards.

Middle East & Africa

Africa continues to serve as a key production and export hub for preservatives, while Middle Eastern countries such as the UAE, Saudi Arabia, and Qatar are experiencing rising demand due to high-income populations and growing packaged food consumption. Intra-African demand is increasing in South Africa and Nigeria, driven by urbanization and expanding food processing infrastructure. The adoption of multifunctional preservatives is supported by the need for longer shelf-life products to withstand hot climates, supply chain challenges, and increasing exports. Additionally, government initiatives promoting food safety and industrial growth in the region are creating a favorable environment for market expansion.

Key Players in the Food Preservatives Market

- BASF SE

- Archer Daniels Midland Company

- Corbion N.V.

- DuPont de Nemours, Inc.

- Kemin Industries, Inc.

- Chr. Hansen Holding A/S

- Associated British Foods PLC

- Koninklijke DSM N.V.

- Tate & Lyle PLC

- Kerry Group PLC

- Ajinomoto Co., Inc.

- Givaudan SA

- Jungbunzlauer Suisse AG

- Dohler Group

- Ingredion Incorporated