Pet Digestive Health Supplements Market Size

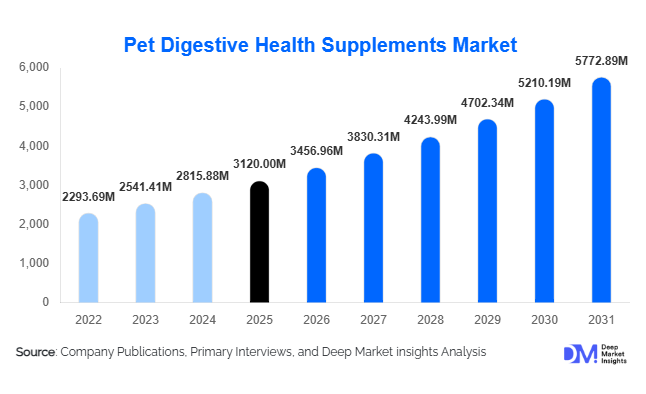

According to Deep Market Insights,the global pet digestive health supplements market size was valued at USD 3,120 million in 2025 and is projected to grow from USD 3,456.96 million in 2026 to reach USD 5,772.89 million by 2031, expanding at a CAGR of 10.8% during the forecast period (2026–2031). Market growth is primarily driven by rising pet humanization trends, increasing awareness of gut microbiome health, and growing demand for preventive veterinary care solutions. The shift toward premium pet nutrition and clinically validated probiotic formulations is further accelerating global adoption.

Key Market Insights

- Probiotics dominate product demand, accounting for nearly 42% of total market share in 2025, supported by strong veterinary endorsements and microbiome research advancements.

- Dogs represent the largest pet segment, contributing approximately 58% of global revenue due to higher healthcare spending per animal.

- North America leads the global market, holding around 38% share in 2025, driven by high pet ownership and premiumization trends.

- Asia-Pacific is the fastest-growing region, projected to expand at over 13% CAGR through 2031 due to urbanization and rising disposable income.

- Online retail channels account for nearly 34% of global sales, supported by subscription-based supplement models and DTC brand strategies.

- Chewable formats remain the most preferred formulation, representing approximately 46% of 2025 market revenue due to improved compliance and palatability.

What are the latest trends in the pet digestive health supplements market?

Microbiome-Centric and Personalized Nutrition Solutions

Advances in microbiome research are reshaping product development strategies. Manufacturers are increasingly investing in strain-specific probiotics supported by clinical validation. Personalized digestive health solutions based on microbiome testing kits and subscription-based custom blends are gaining traction, particularly in North America and Europe. This shift toward precision nutrition mirrors developments in human nutraceuticals, positioning digestive health supplements as a long-term preventive healthcare solution rather than a reactive treatment.

Integration with Functional Pet Foods

Digestive health supplements are increasingly being incorporated into functional treats and fortified pet foods. Pet food manufacturers are collaborating with supplement companies to develop synbiotic-enriched kibbles and soft chews. This convergence of nutrition and supplementation is expanding consumer convenience while strengthening brand loyalty. Functional treat formats are especially popular among younger pet owners who prefer simplified administration without capsules or powders.

What are the key drivers in the pet digestive health supplements market?

Rising Pet Humanization and Premium Spending

Pet owners increasingly consider animals as family members, resulting in higher per capita healthcare spending. Premium digestive health supplements formulated with high-quality strains, natural fibers, and clean-label ingredients are witnessing strong demand. Growing disposable income in emerging economies is further amplifying this driver.

Increasing Prevalence of Gastrointestinal Disorders

Rising cases of food intolerance, antibiotic-associated diarrhea, and inflammatory bowel conditions in pets are contributing to sustained demand. Veterinary clinics frequently recommend probiotic and enzyme supplements to restore gut flora after antibiotic treatment, supporting recurring sales and long-term usage patterns.

What are the restraints for the global market?

Regulatory Variability Across Regions

Regulatory classifications for nutraceuticals differ across the U.S., EU, China, and other regions, increasing compliance costs. Labeling standards, health claims approval, and ingredient registrations present challenges for global expansion.

Limited Standardization and Clinical Validation

Inconsistent clinical evidence across brands can affect consumer trust. Companies must invest in R&D and third-party trials to ensure product differentiation and credibility, particularly in mature markets.

What are the key opportunities in the pet digestive health supplements industry?

Expansion in Emerging Markets

Rapid growth in pet ownership across Asia-Pacific and Latin America presents strong untapped demand. Localization of manufacturing and affordable product lines can help brands penetrate mid-income consumer segments in countries such as China, India, and Brazil.

Veterinary Partnerships and Therapeutic Positioning

Strategic partnerships with veterinary hospital chains can position digestive supplements as part of routine therapeutic protocols. With the global veterinary services industry exceeding USD 130 billion in 2025, integration into clinical practice represents a high-growth opportunity for manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3120 Million |

| Market Size in 2026 | USD 3456.96 Million |

| Market Size in 2031 | USD 5772.89 Million |

| CAGR | 10.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Pet Type Insights

The global pet digestive health supplements market is primarily driven by dogs, which account for approximately 58% of total revenue in 2025. This dominance is attributed to higher veterinary visitation frequency, greater preventive healthcare spending, and stronger supplement adoption among dog owners. Dogs are more frequently diagnosed with gastrointestinal disorders, food sensitivities, and age-related digestive concerns, encouraging consistent probiotic and enzyme supplementation. The humanization of pets and increasing expenditure on premium canine nutrition further reinforce segment leadership. Cats represent nearly 34% of the market, supported by rising awareness of digestive sensitivity, hairball-related gastrointestinal issues, and specialized feline microbiome care. Growing indoor cat ownership and targeted product formulations designed specifically for feline digestive systems are strengthening this segment’s growth trajectory. Other companion animals, including rabbits, birds, and small mammals, account for the remaining share; however, niche premiumization trends and specialty veterinary recommendations are enabling steady expansion within this category.

Product Type Insights

Probiotics lead the product segment with nearly 42% market share in 2025, primarily driven by strong clinical validation supporting gut microbiome balance, immunity enhancement, and improved nutrient absorption. Increasing scientific research into pet microbiota and growing consumer familiarity with probiotic benefits in human health have accelerated cross-adoption in companion animal care. Digestive enzymes and synbiotics follow, benefiting from rising diagnoses of pancreatic insufficiency and chronic digestive irregularities in aging pets. The leading segment driver remains expanding microbiome awareness and preventive supplementation trends, which continue to position probiotics at the forefront of innovation and new product launches. Fiber-based supplements are gaining significant traction, particularly among senior pets, due to their effectiveness in promoting bowel regularity and reducing constipation risks. Meanwhile, postbiotics represent an emerging innovation category, supported by advancements in microbial metabolite research and enhanced stability profiles compared to traditional live probiotic strains.

Formulation Insights

Chewable tablets and soft chews collectively account for approximately 46% of total revenue, driven by superior palatability, ease of administration, and higher compliance rates among pet owners. The leading growth driver in this segment is improved product acceptance, as flavored soft chews reduce resistance and eliminate the need for forced administration. Powders hold nearly 24% market share and are widely recommended by veterinarians due to their flexible dosing capabilities and suitability for therapeutic digestive interventions. Capsules, liquids, and functional treats contribute to the remaining market value, with functional treats gaining traction as pet owners increasingly prefer multi-benefit nutritional solutions that combine digestive support with overall wellness claims.

Distribution Channel Insights

Online retail dominates the distribution landscape with around 34% market share in 2025, supported by expanding e-commerce penetration, subscription-based purchasing models, and access to a wide range of premium and specialty brands. The primary growth driver within this segment is digital convenience combined with detailed product transparency, reviews, and competitive pricing. Pet specialty stores account for approximately 28% of sales, benefiting from knowledgeable staff recommendations and curated premium product assortments. Veterinary clinics contribute nearly 22% of total revenue, particularly for therapeutic-grade digestive supplements prescribed for clinical gastrointestinal conditions. Mass retail channels continue to expand in emerging economies, driven by improving retail infrastructure and growing consumer access to affordable supplement options.

End-Use Insights

Household pet owners represent nearly 64% of global demand, driven by increasing preventive healthcare awareness and the ongoing trend of pet humanization. The leading driver for this segment is proactive digestive health management, as owners increasingly prioritize daily supplementation to avoid costly medical treatments. Veterinary therapeutic use is the fastest-growing segment, expanding at over 12% CAGR, supported by rising incidence of chronic digestive disorders and greater clinical endorsement of probiotic-based interventions. Breeders and shelters account for a smaller but stable share of demand, typically purchasing in bulk to maintain digestive stability in multi-animal environments where stress-related gastrointestinal issues are common.

Explore more data points, trends and opportunities Download Free Sample Report

Pet Digestive Health Supplements Market Segmentations

By Pet Type

- Dogs

- Cats

- Other

By Product Type

- Probiotics

- Prebiotics

- Postbiotics

- Digestive Enzymes

- Synbiotics

- Fiber-Based Supplements

By Formulation Form

- Chewable Tablets & Soft Chews

- Powders

- Capsules & Tablets

- Liquids & Pastes

- Functional Treats

By Distribution Channel

- Online Retail & E-commerce

- Pet Specialty Stores

- Veterinary Clinics & Hospitals

- Mass Retail

By End-Use

- Household Pet Owners

- Veterinary Therapeutic Use

- Pet Breeders & Kennels

- Animal Shelters & Rescue Organizations

Regional Insights

North America

North America holds approximately 38% of the global market share in 2025, with the United States contributing nearly 30% alone. Regional growth is driven by high pet ownership rates, advanced veterinary infrastructure, and strong consumer willingness to spend on premium and preventive pet healthcare solutions. A well-established e-commerce ecosystem, subscription-based supplement models, and extensive product availability further accelerate market penetration. In addition, increasing awareness of pet microbiome science and strong marketing investments by major brands continue to stimulate product innovation. Canada demonstrates steady growth, supported by nationwide veterinary awareness campaigns and expanding adoption of natural and clean-label digestive supplements.

Europe

Europe accounts for around 27% of global revenue, with Germany, the United Kingdom, and France serving as key revenue contributors. Regional growth is driven by strict regulatory frameworks that enhance product quality assurance and consumer trust, allowing premium pricing strategies. Rising adoption of preventive veterinary care and increasing consumer preference for natural, organic, and sustainably sourced ingredients are further supporting market expansion. Additionally, growing awareness of animal welfare standards and responsible pet ownership practices across Western Europe continues to strengthen demand for clinically validated digestive supplements.

Asia-Pacific

Asia-Pacific holds approximately 22% market share in 2025 and is the fastest-growing region, projected to expand at over 13% CAGR. Growth is primarily driven by rapid urbanization, rising disposable incomes, and expanding middle-class populations that are increasingly adopting companion animals. China and Japan lead regional consumption due to strong pet humanization trends and growing availability of premium imported brands. India is witnessing rapid acceleration, supported by increasing urban pet ownership, improving veterinary access, and expanding digital retail platforms. The region also benefits from growing awareness of preventive healthcare and rising demand for specialized digestive formulations tailored to breed-specific and age-specific needs.

Latin America

Latin America contributes nearly 8% of global demand, with Brazil and Mexico serving as primary markets. Regional growth is supported by rising pet adoption rates, expanding middle-income populations, and increasing availability of specialty pet retail chains. Growing educational initiatives around preventive pet healthcare and improving access to veterinary services are strengthening supplement adoption. E-commerce expansion and cross-border product availability are further enhancing market penetration across urban centers.

Middle East & Africa

The Middle East & Africa region accounts for approximately 5% of the global market, led by the United Arab Emirates and South Africa. Growth is driven by increasing pet adoption in urban metropolitan areas, rising disposable incomes, and expanding premium pet product imports. The gradual development of organized retail infrastructure and veterinary services is improving accessibility to digestive health supplements. Additionally, a growing expatriate population in Gulf countries and increasing awareness of companion animal wellness are contributing to steady long-term market expansion.

Key Players in the Pet Digestive Health Supplements Market

- Nestlé Purina PetCare

- Mars Petcare

- Hill’s Pet Nutrition

- Zoetis Inc.

- Elanco Animal Health

- Virbac

- Vetoquinol

- ADM (Animal Nutrition Division)

- Chr. Hansen Holding

- DSM-Firmenich

- Nutramax Laboratories Veterinary Sciences

- Zesty Paws

- PetHonesty

- NaturVet

- NOW Foods