Novel Dietary Fibers Market Size

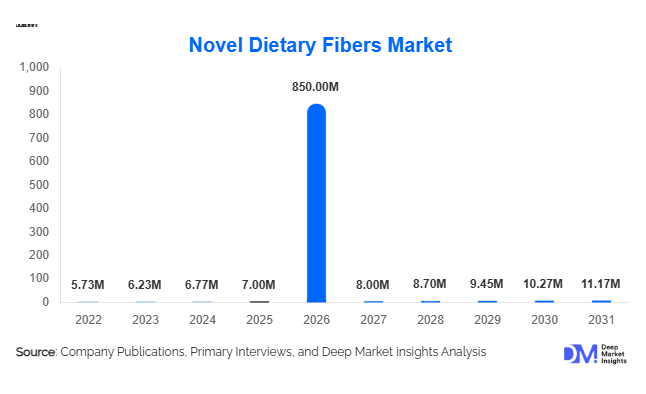

According to Deep Market Insights, the global novel dietary fibers market size was valued at USD 7,850 million in 2025 and is projected to grow from USD 8,532.95 million in 2026 to reach USD 12,949.32 million by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). Market growth is primarily driven by rising consumer awareness of gut health, increasing demand for sugar reduction in processed foods, and strong regulatory backing for fiber-enriched product claims across developed economies.

Novel dietary fibers, including inulin, resistant starch, polydextrose, beta-glucan, and galacto-oligosaccharides (GOS), are increasingly being incorporated into functional foods, beverages, dietary supplements, and clinical nutrition products. Unlike traditional fibers, these ingredients offer targeted physiological benefits such as microbiome modulation, glycemic control, cholesterol reduction, and improved digestive health. Growing incidences of obesity, diabetes, and lifestyle-related disorders are further encouraging manufacturers to reformulate products with added fiber content.

Key Market Insights

- Prebiotic fibers account for nearly 35% of the total market value, driven by strong demand for microbiome-focused nutrition solutions.

- Functional foods and beverages dominate applications, contributing approximately 44% of the 2025 global market revenue.

- North America leads the global market, holding around 34% share in 2025, supported by strong supplement consumption and regulatory clarity.

- Asia-Pacific is the fastest-growing region, expanding at over 10% CAGR due to rising urbanization and preventive healthcare adoption.

- Plant-based fibers represent nearly 68% of the total supply, reflecting clean-label and sustainability-driven consumer preferences.

- The top five companies control approximately 48% of the global market, indicating moderate consolidation with strong technological differentiation.

What are the latest trends in the novel dietary fibers market?

Microbiome-Centric Product Innovation

Consumer interest in gut microbiome health has accelerated the development of targeted prebiotic formulations. Ingredient manufacturers are investing in clinical validation of inulin, resistant dextrin, and GOS to support digestive and immune health claims. Functional beverages, protein bars, and dairy alternatives increasingly incorporate soluble fibers that enhance digestive tolerance while maintaining taste and texture. Partnerships between ingredient suppliers and nutraceutical brands are strengthening, with new product launches emphasizing synbiotic combinations (prebiotics + probiotics) for enhanced efficacy. This trend is especially pronounced in North America, Europe, and Japan, where personalized nutrition is gaining traction.

Sugar Reduction and Clean-Label Reformulation

Global sugar taxes and front-of-pack labeling regulations are encouraging manufacturers to replace sugar with fiber-based bulking agents such as polydextrose and soluble corn fiber. These ingredients enable calorie reduction without compromising product stability. Clean-label claims are becoming central to competitive positioning, prompting investment in non-GMO, plant-based, and minimally processed fiber sources. Food companies are reformulating bakery, cereal, dairy, and beverage products to achieve “high-fiber” and “reduced sugar” labels, significantly expanding commercial applications.

What are the key drivers in the novel dietary fibers market?

Rising Prevalence of Lifestyle Diseases

Increasing cases of obesity, cardiovascular diseases, and type-2 diabetes globally are encouraging dietary interventions. Clinical evidence supporting fiber’s role in glycemic control and cholesterol reduction is driving adoption in both functional foods and medical nutrition products. Healthcare professionals are recommending higher fiber intake, indirectly stimulating B2B demand from food manufacturers.

Expansion of Functional and Plant-Based Foods

The global plant-based food industry, valued at over USD 45 billion, relies heavily on functional fibers for texture, stability, and nutritional enhancement. Novel fibers improve mouthfeel in dairy alternatives and plant-based meat products, making them indispensable in reformulation strategies. This structural role in food technology is a long-term growth driver.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in corn, chicory root, cassava, and cereal prices directly affect production costs. Energy-intensive fermentation processes also expose manufacturers to rising operational expenses, impacting profit margins.

Digestive Tolerance and Dosage Limitations

Excessive fiber consumption can lead to bloating or gastrointestinal discomfort, limiting formulation thresholds. Manufacturers must balance functionality and consumer tolerance, requiring extensive R&D investment.

What are the key opportunities in the novel dietary fibers industry?

Emerging Market Expansion

India, China, Brazil, and Southeast Asia are witnessing rapid growth in fortified packaged foods. Rising disposable incomes and government health initiatives promoting dietary fiber intake create significant market entry opportunities. Localized manufacturing under initiatives such as “Make in India” further enhances growth prospects.

Personalized Nutrition Platforms

Integration of microbiome testing with customized supplement subscriptions presents a high-margin niche. Digital health platforms are increasingly incorporating prebiotic fibers into tailored dietary solutions, offering recurring revenue opportunities for manufacturers.

Fiber Type Insights

Inulin remains the leading fiber type, accounting for approximately 22% of total 2025 revenue, primarily driven by its strong prebiotic functionality and broad regulatory acceptance across North America and Europe. Its ability to selectively stimulate beneficial gut bacteria, combined with neutral taste and high solubility, makes it highly suitable for dairy alternatives, yogurt, protein beverages, meal replacements, and dietary supplements. The leading growth driver for inulin is the accelerating consumer focus on microbiome health and digestive wellness, particularly in functional food reformulations and synbiotic product launches.

Resistant starch and polydextrose collectively represent a significant secondary share of the market, supported by rising demand for sugar reduction and calorie control. Their bulking properties and low glycemic impact make them critical in bakery, cereals, and snack reformulation initiatives responding to global sugar taxes. Beta-glucan continues steady expansion due to clinically supported cholesterol-lowering claims, especially in heart-health-positioned cereals and oat-based beverages. Meanwhile, galacto-oligosaccharides (GOS) and other specialty oligosaccharides command premium pricing in infant nutrition and medical formulations, where clinical validation and regulatory compliance create higher entry barriers and stronger margins.

Application Insights

Functional foods and beverages dominate the market, contributing nearly 44% of total global value in 2025. The primary driver for this segment is large-scale reformulation of packaged foods to achieve “high fiber” and “reduced sugar” labeling. Bakery, dairy alternatives, cereals, nutrition bars, and ready-to-drink beverages are the major consumption categories. Rising demand for plant-based and clean-label foods further strengthens fiber incorporation across product portfolios.

Dietary supplements are the fastest-growing application segment, expanding at nearly 10% CAGR, fueled by personalized nutrition trends and rising online sales. Capsule, powder, and sachet-based fiber supplements are gaining popularity among consumers seeking digestive and metabolic health support. Infant nutrition remains a high-value niche, particularly in China and Western Europe, where prebiotic fortification has become standard practice in formula products. Additionally, clinical and medical nutrition is emerging as a strategic growth area due to aging populations, increased hospitalization rates, and greater focus on disease-specific dietary management.

Distribution Channel Insights

B2B ingredient suppliers dominate distribution, accounting for nearly 70% of global revenues, as novel dietary fibers are primarily incorporated at the manufacturing stage. Long-term procurement contracts between ingredient producers and multinational food companies ensure stable volumes and predictable revenue streams. The key driver for this dominance is large-scale food reformulation and private-label expansion across developed markets.

However, retail and e-commerce channels are expanding rapidly for finished fiber supplements, particularly in North America and Asia-Pacific. Digital health awareness, influencer-driven marketing, and subscription-based supplement models are accelerating direct-to-consumer sales. Online platforms provide transparency in ingredient sourcing and clinical validation, increasing consumer confidence and repeat purchase behavior.

End-Use Industry Insights

The functional food industry, valued at over USD 320 billion globally, remains the largest end-use sector for novel dietary fibers. Continuous innovation in fortified cereals, dairy alternatives, snack bars, and beverages is sustaining ingredient demand. The sector’s consistent 6–8% annual growth rate directly translates into stable fiber consumption expansion. The dietary supplements industry, exceeding USD 180 billion worldwide, is growing at more than 8% annually, creating a high-margin demand pool for specialty fibers. Export-driven demand is particularly notable from the United States and Germany, which supply high-value prebiotic fibers to Asia-Pacific markets where domestic production of specialty oligosaccharides remains limited. Additionally, rising clinical nutrition expenditure in hospitals and elderly care facilities is generating incremental demand for resistant starch and soluble fiber formulations.

| By Fiber Type | By Application | By Distribution Channel | By Source |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America holds approximately 34% of the 2025 global market share, with the United States contributing nearly 80% of regional revenue. The primary growth driver is strong consumer awareness of digestive health, supported by a well-established supplement consumption culture and regulatory clarity around fiber health claims. The presence of major ingredient manufacturers and advanced food processing infrastructure further strengthens regional dominance. Canada is witnessing rising demand for plant-based and clean-label fortified foods, while Mexico is gradually adopting fiber-based reformulations driven by sugar tax policies.

Europe

Europe accounts for around 29% of global revenue, led by Germany, France, and the United Kingdom. A key regional growth driver is regulatory endorsement of beta-glucan and fiber-related health claims under EFSA guidelines, which encourages product innovation. Strong consumer preference for clean-label and organic ingredients supports demand for plant-based fibers. Additionally, the region’s advanced infant nutrition industry, particularly in Germany and the Netherlands, fuels demand for specialty oligosaccharides. Sustainability initiatives and non-GMO labeling requirements further enhance regional fiber consumption.

Asia-Pacific

Asia-Pacific represents nearly 27% of global market share and is the fastest-growing region, expanding at over 10% CAGR. Rapid urbanization, rising disposable incomes, and increasing awareness of preventive healthcare are primary growth drivers. China leads regional demand due to strong infant nutrition and functional beverage industries, while India is experiencing accelerated growth supported by expanding packaged food consumption and government-led nutrition awareness campaigns. Japan remains a mature market with consistent demand for functional beverages enriched with soluble fibers. Expanding local manufacturing capacities and foreign direct investment in food processing are further boosting regional growth.

Latin America

Latin America holds approximately 6% of the global market share, with Brazil and Mexico as leading contributors. Regional growth is driven by sugar reformulation mandates, increasing packaged food penetration, and rising middle-class consumption. Domestic food manufacturers are integrating fiber ingredients to meet evolving labeling regulations and address obesity-related health concerns. Import reliance for specialty fibers remains high, creating opportunities for international suppliers.

Middle East & Africa

The Middle East & Africa region contributes nearly 4% of global revenue. Growth is primarily supported by rising urbanization, increasing demand for fortified packaged foods, and expanding modern retail networks in the UAE and Saudi Arabia. South Africa leads Sub-Saharan Africa in fiber-enriched cereal and bakery consumption. The region remains import-dependent for most specialty fibers, but growing investments in food processing infrastructure and premium supplement demand are gradually strengthening market expansion.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Novel Dietary Fibers Market

- Cargill Inc.

- Archer Daniels Midland (ADM)

- Ingredion Incorporated

- Tate & Lyle PLC

- Roquette Frères

- BENEO GmbH

- Kerry Group

- FrieslandCampina Ingredients

- Südzucker AG

- Cosucra Groupe Warcoing

- Nexira

- CP Kelco

- Tereos Group

- SunOpta Inc.

- Samyang Corporation