Marzipan Market Size

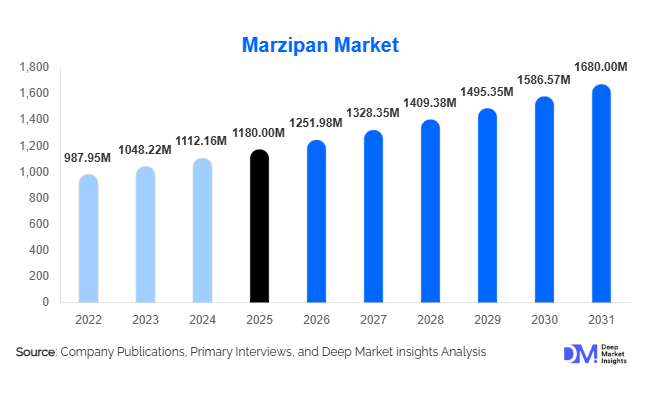

According to Deep Market Insights, the global marzipan market size was valued at USD 1,180 million in 2025 and is projected to grow from USD 1,251.98 million in 2026 to reach USD 1,680 million by 2031, expanding at a CAGR of 6.1% during the forecast period (2026–2031). The marzipan market growth is primarily driven by rising demand for premium confectionery, increasing use of marzipan in bakery and chocolate applications, and growing consumer preference for artisanal and clean-label desserts.

Key Market Insights

- Classic almond marzipan remains the dominant product type, supported by its extensive use in bakery and confectionery manufacturing.

- Europe leads global demand, accounting for nearly half of total consumption, driven by strong cultural and festive traditions.

- Bakery and confectionery manufacturing is the largest end-use segment, benefiting from the global expansion of premium baked goods.

- APAC is the fastest-growing region, supported by Western-style bakery adoption and rising disposable incomes.

- Premium and high-almond-content marzipan products are gaining traction, reflecting broader premiumization trends.

- E-commerce and direct-to-consumer channels are reshaping distribution, enabling specialty producers to reach global consumers.

What are the latest trends in the marzipan market?

Premium and High-Almond Formulations on the Rise

Premiumization is a defining trend in the marzipan market, with manufacturers increasing almond content and focusing on artisanal production methods. High-almond marzipan variants, often exceeding 65% almond content, are gaining popularity among gourmet consumers and professional bakers. These products offer superior texture and flavor, allowing manufacturers to command higher price points and margins. Premium marzipan is increasingly positioned as a luxury ingredient for fine chocolates, wedding cakes, and festive desserts, reinforcing its value perception.

Innovation in Sugar-Reduced and Functional Marzipan

Health-conscious consumer behavior is driving innovation in sugar-reduced, organic, and functional marzipan products. Manufacturers are experimenting with alternative sweeteners and natural formulations to comply with sugar-reduction regulations while maintaining taste quality. Organic-certified marzipan and clean-label offerings are particularly popular in Europe and North America, aligning with broader trends in responsible and mindful consumption.

What are the key drivers in the marzipan market?

Growth of the Global Bakery and Confectionery Industry

The expanding global bakery and confectionery industry is the primary driver of marzipan demand. Marzipan is widely used in cakes, pastries, filled chocolates, and decorative applications, making it a critical ingredient for both artisanal and industrial producers. The premium bakery segment, in particular, continues to grow at a robust pace, directly supporting marzipan consumption.

Strong Seasonal and Festive Consumption Patterns

Seasonal demand during Christmas, Easter, weddings, and regional festivals accounts for a significant portion of annual marzipan sales. Traditional marzipan products such as molded figures and gift assortments experience predictable demand spikes, providing revenue stability for manufacturers and retailers.

What are the restraints for the global market?

Volatility in Almond Prices

Almonds account for a substantial share of marzipan production costs, making the market highly sensitive to raw material price fluctuations. Climatic risks, water shortages, and supply concentration in key producing regions such as California and Spain contribute to price volatility, which can impact profitability.

Regulatory Pressure on Sugar Content

Increasing regulatory scrutiny on sugar consumption, particularly in Europe and North America, poses challenges for traditional marzipan formulations. Compliance often requires costly reformulation and labeling changes, potentially slowing product launches.

What are the key opportunities in the marzipan industry?

Expansion into Emerging Markets

Asia-Pacific and Latin America present strong growth opportunities as Western-style bakeries and premium dessert consumption expand. Localized flavors, smaller pack sizes, and partnerships with regional bakery chains can help manufacturers penetrate these high-growth markets.

Direct-to-Consumer and Customization Models

The rise of e-commerce enables marzipan producers to offer customized products such as personalized figurines and festive gift boxes. This model is particularly attractive for small and mid-sized manufacturers seeking global reach without heavy investment in traditional retail infrastructure.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1180 Million |

| Market Size in 2026 | USD 1251.98 Million |

| Market Size in 2031 | USD 1680 Million |

| CAGR | 6.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Classic almond marzipan dominates the global market, accounting for approximately 46% of total revenue in 2025. Its leadership is driven by deep-rooted cultural acceptance in Europe, extensive use in traditional confectionery, and its versatility across industrial bakery and chocolate manufacturing applications. Classic formulations offer stable texture, long shelf life, and cost efficiency, making them the preferred choice for large-scale producers and artisanal bakers alike.

Flavored marzipan continues to gain popularity, especially in confectionery fillings and seasonal assortments, as manufacturers innovate with chocolate, fruit, spice, and regional flavor profiles to appeal to younger consumers. Meanwhile, sugar-reduced and functional marzipan variants remain a niche segment but are expanding rapidly due to rising health awareness, sugar taxation policies, and demand for clean-label alternatives, particularly in Europe and North America.

Form Insights

Blocks and logs represent the leading form in the marzipan market, holding nearly 38% of the global market share. Their dominance is driven by ease of handling, extended shelf stability, and flexibility in portioning, making them ideal for industrial bakeries and confectionery manufacturers. This form enables efficient scaling of production while minimizing material waste.

Sheets and ready-to-roll marzipan are witnessing rising adoption, particularly among artisanal bakeries and cake decorators, as they reduce preparation time and ensure uniform thickness for premium cake coverings. Molded figures and decorative marzipan products are closely linked to seasonal and festive demand, especially during Christmas, Easter, and wedding seasons, where visual appeal and customization play a critical role.

End-Use Insights

Bakery and confectionery manufacturing is the largest end-use segment, accounting for approximately 52% of total global demand. The segment’s leadership is driven by the expanding premium bakery industry, increasing use of marzipan as a decorative and filling ingredient, and the growing popularity of artisanal and specialty baked goods.

Retail and household consumption follows as the second-largest segment, supported by festive gifting traditions, home baking trends, and the growing availability of marzipan through specialty stores and online platforms. Seasonal consumption peaks during holidays, contributing significantly to annual sales volumes. The foodservice and HORECA segment is expanding steadily as hotels, restaurants, and cafés increasingly incorporate premium desserts and confectionery items into their menus. Rising demand for plated desserts, luxury pastries, and customized confectionery offerings is supporting marzipan adoption in upscale hospitality establishments.

Distribution Channel Insights

B2B direct sales dominate the marzipan distribution landscape, particularly for industrial bakery and confectionery customers. Long-term supply contracts, bulk purchasing, and customized formulations drive this channel’s leadership, ensuring stable demand for manufacturers.

Modern trade and specialty gourmet stores play a vital role in retail distribution, especially in Europe and North America, where premium and artisanal marzipan products are positioned as high-value confectionery items. These outlets benefit from strong consumer trust and impulse-driven seasonal purchases. E-commerce and direct-to-consumer (DTC) channels are the fastest-growing distribution segment, driven by global shipping capabilities, personalization options, and increasing consumer preference for online specialty food purchases. Digital platforms enable small and mid-sized producers to access international markets while offering customized marzipan products for festive and gifting applications.

Explore more data points, trends and opportunities Download Free Sample Report

Marzipan Market Segmentations

By Product Type

- Classic Almond Marzipan

- Premium & High-Almond Marzipan

- Flavored Marzipan

- Sugar-Reduced & Functional Marzipan

By Form

- Blocks & Logs

- Sheets & Ready-to-Roll

- Molded Figures & Decorations

- Paste & Fillings (Industrial Use)

By End Use

- Bakery & Confectionery Manufacturing

- Retail & Household Consumption

- Foodservice & HORECA

- Seasonal & Festive Gifting

By Distribution Channel

- B2B Direct Sales

- Modern Trade & Specialty Gourmet Stores

- E-commerce & Direct-to-Consumer (DTC)

Regional Insights

Europe

Europe accounts for approximately 48% of the global marzipan market, led by Germany, Denmark, Spain, and Italy. Regional dominance is driven by strong cultural and festive traditions, high per-capita consumption, and a well-established bakery and confectionery industry. Germany remains the largest single market due to its historical association with marzipan production and consumption. Additional growth drivers include demand for premium and organic marzipan, strong export activity, and regulatory support for clean-label and high-quality food products.

North America

North America represents around 21% of global demand, driven by premium bakery growth, rising interest in artisanal confectionery, and expanding use of marzipan in industrial bakery applications. The United States leads regional consumption, supported by innovation in dessert formats, strong foodservice demand, and increasing consumer willingness to pay for premium ingredients. Growth is further supported by e-commerce expansion and demand for sugar-reduced formulations.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at over 8% CAGR. Key markets include China, Japan, India, and South Korea, where urbanization, Western bakery adoption, and premium gifting culture are driving demand. Growth is fueled by rising disposable incomes, the increasing presence of international bakery chains, and the growing demand for luxury confectionery during festivals and celebrations. Localization of flavors and smaller pack sizes is further accelerating adoption.

Latin America

Latin America holds nearly 7% of the global market, with Brazil and Mexico driving regional growth through expanding industrial bakery sectors and rising imports of premium bakery ingredients. Increasing urban middle-class populations, growing exposure to European-style desserts, and improving cold-chain logistics are supporting steady demand growth.

Middle East & Africa

The Middle East and Africa account for approximately 6% of global demand, supported by luxury gifting traditions, high disposable incomes in Gulf countries, and rapidly growing bakery infrastructure in the UAE and Saudi Arabia. Demand is further driven by premium hospitality projects, increasing tourism, and a strong preference for visually appealing confectionery products used in celebrations and corporate gifting.

Key Players in the Marzipan Market

- Zentis GmbH

- Niederegger Lübeck

- Lübecker Marzipan-Fabrik

- Odense Marcipan

- Lubeca GmbH

- Barry Callebaut

- Cargill

- Puratos Group

- Almond Products Company

- Natra S.A.

- Irca Group

- Valrhona

- Hosta Group

- AAK AB

- Gütermann Confiserie