Low GI Diabetic-Friendly Food Market Size

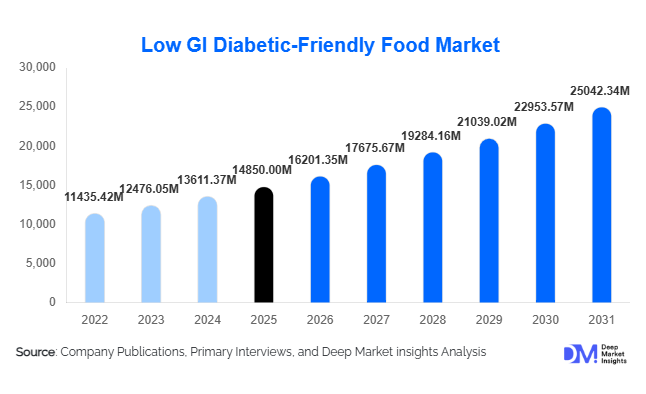

According to Deep Market Insights, the global low GI diabetic-friendly food market size was valued at USD 14,850 million in 2025 and is projected to grow from USD 16,201.35 million in 2026 to reach USD 25,042.34 million by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). The low GI diabetic-friendly food market growth is primarily driven by the rising global prevalence of diabetes, increasing consumer awareness of glycemic management, and expanding demand for preventive nutrition products across both developed and emerging economies.

Key Market Insights

- Low GI staple foods such as rice, pasta, and flour blends dominate product demand, accounting for nearly 28% of total 2025 revenue due to their integration into daily diets.

- North America leads the global market, contributing approximately 36% of total revenue, supported by high diabetes diagnosis rates and strong retail penetration.

- Asia-Pacific is the fastest-growing region, projected to expand at over 11% CAGR through 2031, driven by rising diabetic populations in China and India.

- Premium-priced products represent nearly 45% of global revenue, reflecting strong consumer willingness to pay for clinically positioned and clean-label formulations.

- Whole grain and fiber-enriched ingredients account for over 34% of formulations, reinforcing demand for natural blood sugar management solutions.

- Online retail channels are expanding rapidly, growing at nearly 15% annually due to direct-to-consumer models and personalized nutrition subscriptions.

What are the latest trends in the low-GI diabetic-friendly food market?

Personalized Nutrition and CGM Integration

The integration of continuous glucose monitoring (CGM) devices with dietary planning is transforming consumer purchasing behavior. Individuals are increasingly using real-time glucose tracking to identify food responses, encouraging the adoption of certified low-GI products. Food brands are partnering with digital health platforms to offer tailored meal recommendations and subscription-based product bundles. This personalization trend is particularly strong in North America and Europe, where tech-enabled preventive healthcare ecosystems are mature. The ability to link product efficacy directly to measurable glucose outcomes enhances brand credibility and supports premium pricing strategies.

Expansion of Low GI Staples in Emerging Markets

Manufacturers are increasingly localizing low-GI staple offerings such as rice in Asia, flatbreads in the Middle East, and corn-based products in Latin America. This localization strategy significantly increases household penetration beyond niche diabetic consumers. In countries such as India and China, where rice consumption is central to diets, low GI rice variants are witnessing double-digit growth. Governments promoting sugar reduction and healthier carbohydrate intake further accelerate demand, positioning staple reformulation as a long-term structural growth opportunity.

What are the key drivers in the low-GI diabetic-friendly food market?

Rising Global Diabetes and Pre-Diabetes Population

The increasing number of individuals diagnosed with Type 2 diabetes is the primary structural driver of the market. With over 530 million adults living with diabetes globally and millions more classified as pre-diabetic, demand for blood sugar-regulating food alternatives continues to rise. Urbanization, sedentary lifestyles, and obesity prevalence in developing economies are accelerating product adoption, particularly in the Asia-Pacific and the Middle East.

Shift Toward Preventive and Functional Nutrition

Consumers are proactively managing metabolic health through diet rather than relying solely on pharmaceuticals. Low GI foods align with broader clean-label, plant-based, and high-fiber dietary trends. Retailers are expanding functional food aisles, and healthcare practitioners increasingly recommend low glycemic diets as part of diabetes management plans. Institutional adoption across hospitals and elderly care facilities further reinforces steady demand.

What are the restraints for the global market?

Premium Pricing and Affordability Constraints

Low GI products typically carry a 20–40% price premium due to specialty ingredients such as resistant starches and natural sweeteners. In price-sensitive markets, particularly parts of Africa and Latin America, affordability remains a barrier to mass adoption.

Inconsistent Glycemic Index Labeling Standards

Regulatory inconsistencies in GI certification across countries create consumer confusion and limit product differentiation. The absence of standardized global labeling frameworks restricts transparency and slows market penetration in certain regions.

What are the key opportunities in the low-GI diabetic-friendly food industry?

Institutional and Healthcare Channel Expansion

Hospitals, clinics, elderly care centers, and corporate wellness programs are increasingly incorporating low-GI meal options. Long-term supply contracts offer predictable revenue streams for manufacturers. Preventive healthcare reimbursement models in developed markets create further growth avenues.

Emerging Market Localization Strategies

Adapting formulations to regional dietary preferences, such as low GI rice in Asia or low GI flatbreads in the Middle East, offers substantial first-mover advantages. Rapid urbanization and rising middle-class income levels enhance purchasing power, particularly in India, China, and Southeast Asia.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14850 Million |

| Market Size in 2026 | USD 16201.35 Million |

| Market Size in 2031 | USD 25042.34 Million |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Low GI staple foods lead the global market, accounting for approximately 28% of 2025 revenue, primarily due to their high-frequency consumption patterns and integration into daily dietary routines. Staples such as low GI rice, pasta, flour blends, and tortillas are consumed multiple times per day in major markets including Asia-Pacific, Europe, and Latin America. The leading driver for this segment is the structural shift toward carbohydrate quality optimization rather than carbohydrate elimination. Consumers are not eliminating staples but replacing conventional refined variants with low glycemic alternatives. In Asia-Pacific, particularly India and China, rising diabetes prevalence combined with high rice consumption is accelerating adoption of low GI rice varieties. Additionally, foodservice and institutional procurement of low GI staples is strengthening volume growth.

Low GI snacks and confectionery are witnessing strong innovation, particularly in sugar-free chocolates, high-protein snack bars, and portion-controlled desserts. The driver here is impulse health purchasing and demand for guilt-free indulgence. Beverages, including diabetic-friendly nutritional shakes and meal replacements, are expanding rapidly within healthcare, sports nutrition, and weight management segments. Dairy and plant-based alternatives are gaining traction as lactose-free, clean-label, and plant-forward trends intersect with glycemic management needs.

Ingredient Insights

Whole grain-based formulations dominate the ingredient landscape, representing roughly 34% of total market share in 2025. The primary growth driver for this segment is strong clinical validation linking whole grain intake to improved glycemic control and reduced cardiovascular risk. Regulatory approvals for whole grain health claims in the U.S. and Europe further support adoption.

Sugar substitutes such as stevia, monk fruit, erythritol, and allulose are increasingly replacing refined sugars. The key driver here is regulatory pressure on sugar reduction and consumer demand for natural, zero-calorie sweeteners. Taste profile improvements in blended sweetener systems have significantly improved product palatability, accelerating mainstream penetration. Nut- and legume-based ingredients further enhance protein and fiber content, supporting satiety and metabolic control. These ingredients align with plant-based diet trends, creating cross-category growth opportunities beyond diabetic consumers.

Distribution Channel Insights

Supermarkets and hypermarkets account for approximately 42% of total global revenue, maintaining dominance due to extensive product visibility, private-label expansion, and strong supply chain infrastructure. Large retailers are increasingly introducing private-label low GI product lines at mid-range price points, expanding accessibility beyond premium buyers. The key driver for this channel is consumer preference for one-stop grocery shopping and trust in established retail brands.

Online retail is the fastest-growing channel, expanding at nearly 15% annually. Growth is driven by subscription-based diabetic meal plans, personalized nutrition bundles, and direct-to-consumer brand strategies. E-commerce platforms allow smaller specialty brands to scale without an extensive physical retail presence. Pharmacies and specialty health stores maintain a strong position in clinically positioned products, particularly in developed markets. Physician recommendations and pharmacist guidance reinforce product credibility in these channels.

End-Use Insights

The Type 2 diabetic population accounts for approximately 38% of total market demand in 2025, making it the largest end-use segment. The leading driver for this segment is medical dietary compliance and physician-recommended glycemic control strategies. As diabetes management increasingly integrates lifestyle modification, low GI foods are becoming standard dietary components.

Pre-diabetic and weight management consumers represent the fastest-expanding segments, supported by growing awareness of metabolic syndrome and obesity-related risks. Preventive nutrition adoption among younger demographics is expanding the addressable consumer base. Institutional buyers, including hospitals, elderly care centers, and corporate wellness programs, are contributing to steady volume growth, particularly in North America, Europe, and Japan. Export-driven demand remains strong for low GI rice and fiber-enriched ingredients shipped from Asia to Western markets, reinforcing global trade flows within this category.

Explore more data points, trends and opportunities Download Free Sample Report

Low GI Diabetic-Friendly Food Market Segmentations

By Product Type

- Low GI Staple Foods

- Low GI Bakery & Cereals

- Low GI Snacks & Confectionery

- Low GI Beverages

- Low GI Dairy & Plant-Based Alternatives

By Ingredient Type

- Whole Grain-Based

- Resistant Starch & Fiber-Enriched

- Sugar Substitute-Based

- Nut & Seed-Based

- Legume-Based

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail

- Pharmacies & Medical Stores

- Specialty Health Stores

- Convenience Stores

By End-Use

- Type 2 Diabetic Population

- Type 1 Diabetic Population

- Pre-Diabetic Consumers

- Weight Management Consumers

- Institutional Buyers

Regional Insights

North America

North America holds approximately 36% of the 2025 market share, making it the largest regional market. The United States accounts for nearly 82% of regional revenue, supported by high diabetes prevalence, advanced healthcare infrastructure, and strong consumer awareness regarding glycemic index labeling. Growth drivers in the region include rising obesity rates, insurance-backed preventive healthcare programs, and strong penetration of functional food brands. The presence of leading multinational manufacturers and aggressive private-label expansion further enhances availability. Canada demonstrates steady adoption, particularly in bakery and cereal categories, supported by regulatory clarity around nutritional labeling and high per capita health expenditure.

Europe

Europe represents around 27% of global revenue, with Germany, the United Kingdom, France, and Italy leading demand. Regional growth is driven by strong regulatory emphasis on sugar reduction, clean-label reformulation, and whole-grain consumption. The U.K. exhibits strong growth in low-GI bakery products due to consumer familiarity with glycemic index concepts. Germany’s aging population and well-established healthcare reimbursement structures support institutional demand. Additionally, EU-wide initiatives targeting obesity and metabolic disorders are encouraging reformulation across packaged food categories.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 11% CAGR. China and India dominate regional consumption due to rising diabetic populations, urbanization, and dietary westernization. The primary regional growth driver is the high baseline consumption of carbohydrate staples, creating strong substitution potential for low GI rice and flour products. Government health campaigns in China and India promoting sugar reduction and diabetes awareness further support market penetration. Japan and Australia contribute a steady demand in premium functional and nutraceutical food categories.

Latin America

Brazil and Mexico lead Latin American demand, supported by sugar taxation policies, increasing obesity prevalence, and rising middle-class health awareness. Growth drivers include regulatory initiatives aimed at reducing sugar consumption and expanding retail penetration of functional food categories. While overall market penetration remains moderate compared to North America and Europe, increasing urbanization and retail modernization are accelerating adoption.

Middle East & Africa

Saudi Arabia and the UAE drive growth in the Middle East due to some of the world’s highest obesity and diabetes prevalence rates. Government-led health diversification programs and rising disposable incomes are key growth drivers. In Africa, South Africa leads the regional market, supported by developed retail infrastructure and growing health consciousness among urban populations. However, affordability constraints and limited awareness in certain African economies continue to moderate broader regional penetration.

Key Players in the Low-GI Diabetic-Friendly Food Market

- Nestlé SA

- Abbott Laboratories

- Danone SA

- Kellogg Company

- General Mills Inc.

- Unilever PLC

- PepsiCo Inc.

- The Kraft Heinz Company

- Haleon plc

- Hain Celestial Group

- Hero Group

- Freedom Foods Group

- Bob’s Red Mill Natural Foods

- Beneo GmbH

- Arla Foods