Food Safety Testing Market Size

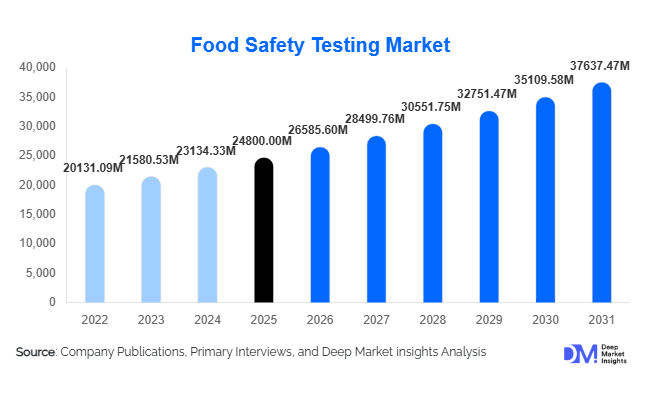

According to Deep Market Insights, the global food safety testing market size was valued at USD 24,800 million in 2025 and is projected to grow from USD 26,585.60 million in 2026 to reach USD 37,637.47 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). Market growth is primarily driven by rising global food trade, increasing foodborne illness outbreaks, stringent regulatory enforcement, and growing consumer demand for transparency in food quality and labeling. As supply chains become more globalized and complex, food manufacturers and regulators are intensifying testing protocols to mitigate contamination risks and ensure compliance with international standards.

Key Market Insights

- Pathogen testing dominates the market, accounting for approximately 34% of total revenue in 2025, driven by zero-tolerance regulations for Salmonella and Listeria in meat and dairy exports.

- Third-party testing laboratories lead service delivery, holding nearly 57% market share due to increasing outsourcing by food manufacturers for accredited compliance testing.

- North America holds the largest regional share (32%), supported by strict regulatory frameworks and advanced laboratory infrastructure.

- Asia-Pacific is the fastest-growing region, expanding at nearly 9% CAGR due to export-driven demand from China and India.

- Molecular diagnostic technologies are rapidly replacing traditional culture methods, accounting for nearly 29% of technology adoption in 2025.

- Processed and ready-to-eat food growth is significantly increasing multi-layer contaminant testing requirements worldwide.

What are the latest trends in the food safety testing market?

Shift Toward Rapid & Molecular Diagnostics

Food safety laboratories are increasingly transitioning from traditional culture-based techniques to PCR-based and molecular diagnostic solutions. These technologies significantly reduce turnaround time from several days to less than 24 hours, allowing faster product release cycles and minimizing recall risks. Automation in DNA extraction, multiplex pathogen detection, and AI-based data interpretation is improving accuracy while lowering labor dependency. Rapid testing kits and portable biosensors are also gaining adoption in high-risk categories such as meat, poultry, and dairy, where contamination control is critical. This trend is particularly strong in North America and Europe, where regulatory agencies emphasize preventive controls under food safety modernization frameworks.

Rising Allergen & Clean-Label Verification Testing

Growing consumer awareness regarding allergen-free and non-GMO food products is driving expansion beyond traditional microbial testing. Manufacturers are increasingly investing in allergen validation, gluten-free certification, pesticide residue detection, and authenticity testing. Clean-label trends are pushing food processors to conduct frequent nutritional and contaminant verification tests to maintain brand credibility. This shift has opened niche, high-margin opportunities for specialized testing labs focusing on infant nutrition, plant-based products, and nutraceutical categories. The increasing popularity of plant-based proteins is further driving cross-contamination testing requirements in mixed manufacturing facilities.

What are the key drivers in the food safety testing market?

Strengthening Regulatory Frameworks Globally

Governments worldwide are tightening food safety regulations, increasing mandatory inspection frequencies, and lowering permissible residue limits. Policies such as the U.S. Food Safety Modernization Act (FSMA) and enhanced European Food Safety Authority (EFSA) standards have institutionalized risk-based preventive controls. Exporting countries must comply with multiple international standards, significantly increasing recurring testing volumes.

Expansion of Global Food Trade

Global food exports continue to grow, particularly from emerging economies such as India, Brazil, Vietnam, and Thailand. Cross-border trade requires certification and residue analysis before shipment, boosting demand for accredited third-party testing services. Meat, seafood, and processed food exporters are increasingly reliant on laboratory networks for compliance validation.

Growth in Processed & Ready-to-Eat Foods

The processed food industry, valued at over USD 3 trillion globally, is expanding at nearly 6% annually. Higher consumption of packaged and convenience foods increases contamination risk points, necessitating frequent pathogen, allergen, and chemical testing.

What are the restraints for the global market?

High Capital & Operational Costs

Advanced analytical instruments such as LC-MS/MS, GC-MS, and PCR systems require significant upfront investment. Smaller food processors may limit testing frequency due to cost pressures, particularly in developing markets.

Infrastructure & Skilled Workforce Limitations

Developing economies often face shortages of accredited laboratories and trained microbiologists, leading to longer turnaround times and inconsistent testing standards.

What are the key opportunities in the food safety testing industry?

Export-Oriented Laboratory Expansion

Emerging markets investing in agricultural exports are expanding laboratory infrastructure to meet EU and U.S. compliance standards. Joint ventures between global testing firms and regional players present high-growth opportunities.

Digitalization & AI Integration

Automation, blockchain-based traceability, and AI-driven predictive contamination analytics are enabling proactive risk management. Companies investing in integrated digital lab systems are expected to improve efficiency and reduce recall incidents.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 24800 Million |

| Market Size in 2026 | USD 26585.60 Million |

| Market Size in 2031 | USD 37637.47 Million |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Test Type Insights

Pathogen testing remains the leading segment, accounting for approximately 34% of the 2025 global food safety testing market. Its dominance is primarily driven by zero-tolerance regulatory frameworks for pathogens such as Salmonella, Listeria monocytogenes, and E. coli in meat, poultry, seafood, and dairy products. The increasing frequency of food recalls and global foodborne illness outbreaks has compelled both regulators and manufacturers to implement routine batch-level microbiological testing. Additionally, the rapid growth of ready-to-eat and minimally processed foods has elevated contamination risks, reinforcing sustained demand for pathogen detection across production and distribution stages. Export-driven meat industries in countries such as Brazil, the United States, and Australia further amplify pathogen testing volumes due to stringent import requirements in North America and Europe.

Chemical and toxin testing represents the second-largest segment, supported by tightening global maximum residue limits (MRLs) for pesticides, veterinary drugs, mycotoxins, and heavy metals. Increasing cross-border trade in fruits, vegetables, grains, and seafood is driving chromatography- and spectrometry-based residue testing. Meanwhile, allergen and GMO testing are the fastest-growing sub-segments, fueled by clean-label trends, plant-based product expansion, and mandatory allergen labeling regulations in developed markets.

Technology Insights

Molecular diagnostics hold nearly 29% share of the technology segment in 2025, making it the leading technological approach in food safety testing. The key growth driver is the need for rapid turnaround times, as PCR- and qPCR-based methods significantly reduce detection cycles from several days to under 24 hours. This speed advantage enables manufacturers to shorten product release timelines, reduce inventory holding costs, and mitigate recall risks. Automation in nucleic acid extraction and multiplex testing capabilities further enhances scalability and cost efficiency, particularly in high-throughput laboratories.

Traditional chromatography and spectrometry technologies, including LC-MS/MS and GC-MS systems, remain indispensable for chemical residue and contaminant analysis. These techniques are critical in meeting increasingly strict pesticide and heavy metal regulations worldwide. Emerging biosensor-based rapid detection kits are gaining traction for on-site screening in meat processing plants and fresh produce facilities, helping reduce logistics delays and enabling real-time contamination control.

Service Type Insights

Third-party testing laboratories dominate the service landscape with approximately 57% market share in 2025. The leading driver for this segment is the growing preference among food manufacturers to outsource testing to accredited laboratories certified under ISO 17025 and global compliance frameworks. Outsourcing ensures regulatory credibility, reduces capital expenditure on advanced equipment, and provides access to specialized expertise in multi-contaminant testing. Increasing global food trade further necessitates independent certification to meet import/export requirements.

In-house laboratories remain relevant among multinational food corporations that conduct routine quality control and preliminary screening. However, advanced confirmatory testing is often outsourced to third-party labs, reinforcing the latter’s dominance.

End-Use Industry Insights

Food manufacturers and processors account for nearly 46% of total demand in 2025, making them the largest end-use segment. The primary growth driver is the expansion of processed and packaged food production globally, which increases mandatory testing at multiple stages, raw material intake, in-process monitoring, and final product validation. Growth in plant-based foods, infant nutrition, dairy alternatives, and nutraceutical products is intensifying allergen, contaminant, and authenticity testing requirements. Additionally, export-oriented food producers require recurring compliance testing to access regulated markets in North America and Europe.

Government and regulatory agencies represent a stable demand base, conducting surveillance testing and import inspections to ensure public health safety. Retail chains and food service operators are also strengthening supplier audit programs, indirectly boosting laboratory testing volumes.

Explore more data points, trends and opportunities Download Free Sample Report

Food Safety Testing Market Segmentations

By Test Type

- Pathogen Testing

- Chemical & Toxin Testing

- Allergen Testing

- GMO Testing

- Nutritional Label Verification

- Shelf-Life & Stability Testing

By Technology

- Traditional Culture-Based Methods

- Molecular Diagnostics (PCR, qPCR, NGS)

- Immunoassay-Based

- Chromatography & Spectrometry

- Biosensors & Rapid Detection Kits

By Service Type

- In-House Laboratories

- Third-Party Contract Testing Laboratories

By End-Use Industry

- Food Manufacturers & Processors

- Food Retailers & Supermarket Chains

- Food Service & Hospitality

- Government & Regulatory Agencies

- Exporters & Import Inspection Agencies

By Food Category

- Meat, Poultry & Seafood

- Dairy Products

- Processed & Packaged Foods

- Fruits & Vegetables

- Beverages

- Cereals, Grains & Pulses

- Infant Food & Nutraceuticals

Regional Insights

North America

North America holds approximately 32% of the global market share in 2025, with the United States contributing nearly 26%. Regional growth is primarily driven by stringent enforcement of preventive food safety regulations, high processed food consumption, and advanced laboratory infrastructure. The U.S. benefits from strong regulatory oversight, mandatory hazard analysis protocols, and frequent recall monitoring systems. Additionally, the region’s large-scale meat, dairy, and packaged food industries require continuous microbiological and chemical testing. Canada also contributes significantly, particularly through export-driven seafood and grain testing.

Europe

Europe accounts for approximately 28% of global revenue, led by Germany, France, the United Kingdom, Italy, and the Netherlands. Growth in the region is driven by strict food safety directives, harmonized residue standards, and strong demand for organic and allergen-free products. European consumers exhibit high awareness of food authenticity and clean labeling, encouraging routine allergen and GMO testing. Additionally, the region’s extensive intra-EU food trade and export activities necessitate multi-contaminant compliance verification.

Asia-Pacific

Asia-Pacific represents around 25% of the global market and is the fastest-growing region, expanding at approximately 9% CAGR. China contributes nearly 8% of global demand, supported by regulatory modernization, food safety reforms, and large-scale processed food production. India is experiencing double-digit growth due to rising agricultural exports, government-led laboratory infrastructure expansion, and increasing domestic packaged food consumption. Japan and Australia maintain steady demand through strict import controls and high seafood and dairy testing requirements. Rapid urbanization and rising middle-class consumption across Southeast Asia further support long-term growth.

Latin America

Latin America holds roughly 8% of the global market share, with Brazil being the primary contributor. The region’s growth is driven by strong meat and poultry exports to North America, Europe, and Asia, requiring rigorous pathogen and residue testing. Argentina, Chile, and Mexico are also expanding food export activities, increasing reliance on accredited third-party laboratories to meet international compliance standards.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of global revenue. Growth drivers include high dependence on food imports in countries such as the UAE and Saudi Arabia, where mandatory import inspection and residue testing are strictly enforced. In Africa, South Africa leads regional demand due to its developed food processing industry and export-oriented fruit and wine sectors. Increasing investments in food laboratory modernization and regional trade agreements are gradually strengthening testing infrastructure across the continent.

Key Players in the Food Safety Testing Market

- Eurofins Scientific

- SGS SA

- Bureau Veritas

- Intertek Group plc

- ALS Limited

- Mérieux NutriSciences

- TÜV SÜD

- TÜV Rheinland

- AsureQuality

- Microbac Laboratories

- Neogen Corporation

- Thermo Fisher Scientific

- bioMérieux

- PerkinElmer

- Romer Labs