Food Authenticity Market Size

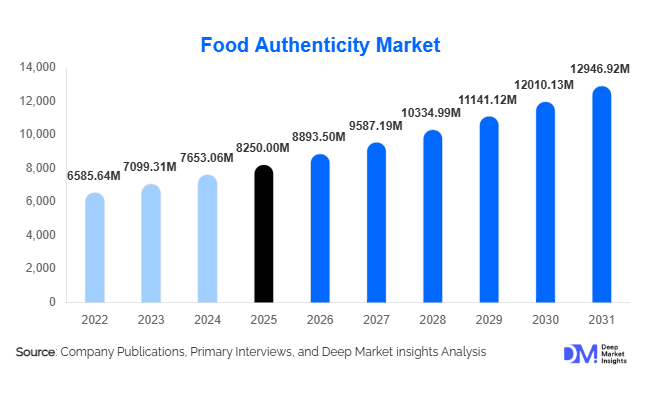

According to Deep Market Insights, the global food authenticity market size was valued at USD 8,250 million in 2025 and is projected to grow from USD 8,893.50 million in 2026 to reach USD 12,946.92 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The food authenticity market growth is primarily driven by increasing food fraud incidents, stricter global labeling regulations, and rising consumer demand for transparency in ingredient sourcing and product origin verification.

As global food supply chains become increasingly complex and cross-border trade intensifies, manufacturers, regulators, and retailers are investing heavily in advanced testing technologies such as PCR, mass spectrometry, isotope ratio analysis, and next-generation sequencing. Food authenticity testing has evolved from a reactive compliance measure to a proactive brand protection strategy. With premium, organic, and geographically indicated products gaining traction, scientific verification is becoming central to maintaining consumer trust and safeguarding export competitiveness across developed and emerging markets.

Key Market Insights

- Species identification testing accounts for nearly 32% of the global market, driven by frequent meat and seafood mislabeling cases.

- Europe leads with approximately 34% market share in 2025, supported by stringent regulatory enforcement and strong premium food consumption.

- Asia-Pacific is the fastest-growing region, expanding at close to 9% CAGR due to export-driven compliance requirements.

- PCR-based technologies dominate with around 28% share, owing to affordability and high testing reliability.

- Food & beverage manufacturers contribute nearly 38% of total demand, as brand protection becomes a strategic priority.

- The top five players control approximately 48% of the global market, indicating moderate consolidation.

What are the latest trends in the food authenticity market?

Blockchain-Integrated Traceability Systems

Food authenticity testing is increasingly being integrated with blockchain-enabled traceability platforms. Manufacturers and retailers are combining laboratory-verified results with digital tracking systems to create tamper-proof supply chain records. This trend is particularly strong in premium categories such as olive oil, seafood, wine, and organic dairy. Retailers are leveraging QR codes that link consumers to verified origin and testing data, enhancing brand transparency and consumer trust. Governments are also piloting national traceability frameworks to strengthen food fraud prevention.

Adoption of Advanced Molecular and Spectroscopy Technologies

Technological advancements such as next-generation sequencing (NGS), isotope ratio mass spectrometry (IRMS), and AI-powered spectral analysis are transforming food authentication accuracy. Rapid, on-site testing kits are gaining traction for preliminary screening, while centralized laboratories continue investing in high-end LC-MS/MS systems for confirmatory analysis. Automation and digital laboratory information management systems (LIMS) are improving turnaround times and reducing per-test costs, further expanding market penetration.

What are the key drivers in the food authenticity market?

Rising Food Fraud Incidents

Increasing global cases of adulteration, species substitution, and false origin claims have heightened awareness among regulators and consumers. High-value products such as seafood, spices, dairy, and olive oil are particularly vulnerable. The financial impact of food fraud, estimated in billions annually, has compelled manufacturers to adopt proactive authentication protocols to protect revenue and brand equity.

Stringent Regulatory Frameworks

Regulatory bodies across North America and Europe have strengthened labeling and traceability standards. Mandatory compliance with food safety certifications and export documentation has driven recurring demand for authentication services. Export-oriented economies in the Asia-Pacific and Latin America are expanding testing capabilities to meet international market requirements.

What are the restraints for the global market?

High Capital Investment Requirements

Advanced analytical technologies such as LC-MS/MS and NGS platforms require substantial capital expenditure and skilled personnel. Small-scale manufacturers and laboratories in developing regions may face barriers to adoption due to cost constraints.

Fragmented Global Standards

Variation in regulatory frameworks across countries complicates the harmonization of testing protocols. Differences in permissible limits and validation methods create operational complexity for multinational food producers.

What are the key opportunities in the food authenticity industry?

Premium and Clean-Label Product Verification

The rapid growth of organic, non-GMO, grass-fed, and geographically indicated products presents a strong opportunity for authentication service providers. Verification of premium claims commands higher margins and long-term contracts with major brands.

Expansion in Emerging Export Economies

Countries such as India, China, Brazil, and Vietnam are strengthening testing infrastructure to enhance export credibility. Investment in regional laboratories and localized partnerships offers significant growth potential for global testing firms.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8250 Million |

| Market Size in 2026 | USD 8893.50 Million |

| Market Size in 2031 | USD 12946.92 Million |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Testing Target Insights

Species identification remains the leading testing target, accounting for approximately 32% of the global food authenticity market in 2025. The segment’s leadership is primarily driven by recurring incidents of meat and seafood substitution, religious and dietary compliance requirements (Halal, Kosher), and stricter traceability mandates in export markets. High-profile fraud cases in beef, horse meat, and premium fish varieties have pushed regulators and retailers to adopt routine DNA-based verification protocols. The growing globalization of meat supply chains and rising demand for processed protein products further strengthen recurring testing volumes in this category.

Adulterant detection represents the second-largest segment, particularly prominent in spices, dairy products, oils, and sweeteners. Economically motivated adulteration, such as dilution of milk, addition of synthetic dyes in spices, and blending of lower-grade oils, continues to drive laboratory demand. Meanwhile, origin and geographical verification is expanding rapidly, supported by geographical indication (GI) protection laws, premium wine and olive oil exports, and country-of-origin labeling regulations. Isotope ratio and trace element profiling are increasingly deployed to validate regional authenticity claims. GMO and allergen testing maintain steady demand, particularly in North America and Europe, where labeling compliance is stringent. The rise of plant-based foods and clean-label products is also expanding the authentication scope into novel ingredients, supporting multi-target testing approaches.

Technology Insights

PCR-based testing dominates the technology landscape with approximately 28% market share in 2025, owing to its high sensitivity, reliability, scalability, and cost efficiency. PCR platforms are widely adopted for species identification and GMO verification, making them essential tools for routine compliance testing across laboratories globally. The availability of multiplex PCR kits and automated systems has further reduced turnaround times and operational costs, reinforcing segment leadership.

Mass spectrometry and chromatography collectively account for a significant portion of high-value confirmatory testing. LC-MS/MS and GC-MS technologies are extensively used for adulterant detection and chemical fingerprinting in oils, beverages, and dairy. These methods command premium pricing due to their analytical precision and regulatory acceptance. Spectroscopy technologies, including NMR and infrared spectroscopy, are gaining momentum due to rapid, non-destructive testing capabilities. They are increasingly used for olive oil, wine, and honey authentication. Additionally, next-generation sequencing (NGS) is emerging as a powerful solution for multi-species detection, particularly in processed and composite foods.

Food Type Insights

Meat & poultry account for approximately 26% of the total market, making it the largest food-type segment. This dominance is driven by high fraud vulnerability, stringent export inspection requirements, and religious certification standards. The processed meat sector, in particular, requires continuous verification due to complex ingredient sourcing and cross-border trade. Dairy and seafood follow closely, supported by strong global trade exposure and premium product pricing. Dairy authentication addresses concerns related to milk powder adulteration, protein substitution, and origin claims. Seafood remains highly susceptible to species mislabeling, particularly in frozen and processed formats, sustaining demand for DNA barcoding technologies.

Spices and herbs represent one of the fastest-growing categories due to high economic adulteration risk and significant export activity from the Asia-Pacific. Premium oils and beverages such as wine and fruit juices also contribute substantially to authentication demand.

End-Use Insights

Food & beverage manufacturers represent the largest end-use segment, contributing nearly 38% of total market demand in 2025. The expansion of in-house quality assurance programs, rising recall costs, and brand reputation risks have prompted manufacturers to integrate routine authenticity testing into procurement and production processes. Multinational brands increasingly adopt supplier verification audits and batch-level authentication testing to mitigate fraud exposure. Third-party testing laboratories are the fastest-growing segment, benefiting from outsourcing trends and regulatory inspections. Many small and mid-sized manufacturers lack the capital investment required for advanced instrumentation, leading to higher reliance on accredited external laboratories. Government and regulatory agencies continue investing in national food testing infrastructure, particularly across Asia-Pacific and the Middle East, where food import dependence necessitates stringent inspection protocols. Retailers and private label brands are also expanding authentication partnerships to safeguard consumer trust.

Explore more data points, trends and opportunities Download Free Sample Report

Food Authenticity Market Segmentations

By Testing Target

- Species Identification

- Adulterant Detection

- Origin & Geographical Verification

- GMO Verification

- Allergen & Contaminant Authentication

- Organic & Label Claim Verification

By Technology

- PCR-Based Testing (PCR & qPCR)

- Next-Generation Sequencing (NGS)

- Mass Spectrometry (LC-MS/MS, GC-MS)

- Chromatography (HPLC, GC)

- Spectroscopy (NMR, IR, Raman)

- Immunoassay-Based Testing (ELISA, Lateral Flow)

By Food Type

- Meat & Poultry

- Seafood

- Dairy Products

- Processed & Packaged Foods

- Beverages (Alcoholic & Non-Alcoholic)

- Oils & Fats

- Spices & Herbs

By End-Use

- Food & Beverage Manufacturers

- Third-Party Testing Laboratories

- Government & Regulatory Agencies

- Retailers & Private Label Brands

- Foodservice & Hospitality

Regional Insights

North America

North America accounts for approximately 29% of the global food authenticity market, with the United States contributing nearly 24% of global revenue. Growth in the region is primarily driven by strong enforcement of labeling regulations, high processed food consumption, and the presence of advanced analytical laboratories. The U.S. benefits from robust regulatory oversight, increasing retailer-led supplier verification programs, and strong consumer demand for non-GMO and clean-label products. Canada supports market expansion through seafood authentication linked to export-oriented fisheries and cross-border trade compliance requirements. High technological adoption and R&D investment further reinforce regional dominance.

Europe

Europe leads the global market with approximately 34% share in 2025. Germany, France, Italy, Spain, and the UK are major contributors. The region’s growth is underpinned by strict EU food safety regulations, geographical indication (GI) protection frameworks, and strong premium food markets, including wine, olive oil, dairy, and specialty meats. The European Union’s traceability mandates and harmonized laboratory accreditation standards (ISO 17025) ensure sustained testing volumes. Rising consumer awareness regarding origin claims and organic certification further supports regional expansion.

Asia-Pacific

Asia-Pacific holds roughly 23% of the global market share and is the fastest-growing region, expanding at nearly 9% CAGR. China and India are strengthening regulatory frameworks and investing in domestic laboratory infrastructure to enhance export credibility and meet international compliance standards. Rapid growth in processed food production, increasing export volumes of seafood and spices, and rising food safety awareness among urban consumers are major growth drivers. Japan and Australia represent technologically mature markets with steady demand for high-end analytical testing. Expansion of cross-border e-commerce in food products is also accelerating authentication needs.

Latin America

Latin America contributes approximately 6% of global revenue, led by Brazil, Mexico, and Argentina. Regional growth is driven by strong meat export industries and the need to comply with European and North American import regulations. Increasing modernization of food safety infrastructure and rising international trade agreements are gradually expanding authentication capabilities. However, adoption remains moderate compared to developed regions due to capital investment constraints.

Middle East & Africa

The Middle East & Africa region accounts for around 8% of the global market. Growth is largely import-driven, particularly in GCC countries such as the UAE and Saudi Arabia, where high dependence on imported food necessitates rigorous verification systems. Investments in centralized food testing laboratories and halal compliance verification are major regional drivers. South Africa serves as a key testing hub in Sub-Saharan Africa, supported by export-oriented agriculture and government-backed food safety initiatives. Rising urbanization and retail modernization are gradually strengthening demand across the broader region.

Key Players in the Food Authenticity Market

- Eurofins Scientific

- SGS SA

- Bureau Veritas

- Intertek Group

- Thermo Fisher Scientific

- Agilent Technologies

- Waters Corporation

- Merieux NutriSciences

- ALS Limited

- Neogen Corporation

- Bio-Rad Laboratories

- PerkinElmer

- Shimadzu Corporation

- Bruker Corporation

- AsureQuality